Business

Trans Mountain pipeline’s soaring cost provides more proof of government failure

From the Fraser Institute

By Julio Mejía and Elmira Aliakbari

To recap, since the Trudeau government purchased the project from Kinder Morgan for $4.5 billion in 2018, the cost of the Trans Mountain expansion has ballooned (in nominal terms) to $34 billion.

According to the latest calculations, the Trans Mountain pipeline expansion project, which the Trudeau government purchased from Kinder Morgan in 2018, will cost $3.1 billion more than the $30.9 billion projected last May, bringing the total cost to about $34 billion—more than six times the original estimate.

This is yet another setback for a project facing rising costs and delays. To understand how we arrived at this point, let’s trace the project’s history.

In 2013, Kinder Morgan applied to the National Energy Board (NEB) to essentially twin the existing pipeline built in 1953, which runs for 1,150 kilometres between Strathcona County, Alberta and Burnaby, British Columbia, with the goal to have oil flow through the expansion by December 2019.

In 2016, after three years of deliberations, the NEB approved the pipeline, subject to 157 conditions. By that time, according to Kinder Morgan, costs had risen by $2 billion, bringing the total cost to $7.4 billion.

And yet, despite Kinder Morgan following the legal and regulatory process to get the necessary approvals, the B.C. NDP and Green Party vowed to “immediately employ every tool available” to stop the project. At the same time, the Trudeau government was planning regulations that would increase the cost and uncertainty of infrastructure projects across the country.

Faced with mounting uncertainty and potential setbacks, Kinder Morgan planned to withdraw from the project in 2018. In response, the Trudeau government intervened, nationalizing the project by purchasing it from Kinder Morgan with taxpayer dollars for $4.5 billion. Once under government control, costs skyrocketed to $12.6 billion by 2020 and $21.4 billion by 2022 reportedly due to project safety requirements, financing costs, permitting costs, and crucially, more agreements with Indigenous communities. One year later, in 2023, the Trudeau government said the cost has risen to $30.9 billion.

To recap, since the Trudeau government purchased the project from Kinder Morgan for $4.5 billion in 2018, the cost of the Trans Mountain expansion has ballooned (in nominal terms) to $34 billion.

Surprised? You shouldn’t be.

When government attempts to build infrastructure projects, it often incurs cost overruns and delays due to a lack of incentives to build in an efficient and resourceful way. According to a study by Bent Flyvbjerg, an expert in this field, a staggering 90 per cent of 258 public transportation projects (in 20 countries) exceeded their budgets. The reason behind this phenomenon is clear—unlike private enterprises, government officials can shift cost overruns onto the public without bearing any personal financial consequences.

And the Trudeau government continues to make a bad situation even worse by introducing uncertainty and erecting barriers to private-sector investment in vital infrastructure projects including pipelines. Federal Bill C-69, for instance, overhauled the entire environmental assessment process and imposed complex and subjective review requirements on major energy projects, casting doubt on the viability of future endeavours.

What’s the solution to this mess?

Clearly, if policymakers want to help develop Canada’s natural resource potential—and the jobs, economic opportunity and government revenue that comes with it—they must enact regulatory reform and incentivize private investment. Rather than assuming the role of construction companies, governments should create an environment conducive to private-sector participation, thereby mitigating risk to taxpayers.

By implementing reasonable and competitive regulations that enhance investment incentives, policymakers—including in the Trudeau government—can encourage the private sector to build large-scale infrastructure projects that benefit the Canadian economy.

Authors:

MxM News

MxM News

Quick Hit:

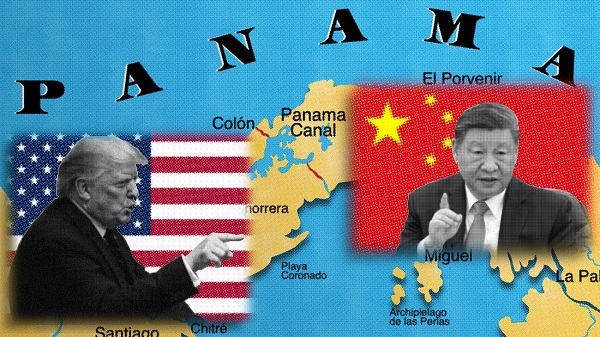

President Donald Trump is pushing for U.S. ships to transit the Panama and Suez canals without paying tolls, arguing the waterways would not exist without America.

Key Details:

-

In a Saturday Truth Social post, Trump said, “American Ships, both Military and Commercial, should be allowed to travel, free of charge, through the Panama and Suez Canals! Those Canals would not exist without the United States of America.”

-

Trump directed Secretary of State Marco Rubio to “immediately take care of, and memorialize” the issue, signaling a potential new diplomatic initiative with Panama and Egypt.

-

The Panama Canal generated about $3.3 billion in toll revenue in fiscal 2023, while the Suez Canal posted a record $9.4 billion. U.S. vessels account for roughly 70% of Panama Canal traffic, according to government figures.

Diving Deeper:

President Donald Trump is pressing for American ships to receive free passage through two of the world’s most critical shipping lanes—the Panama and Suez canals—a move he argues would recognize the United States’ historic role in making both waterways possible. In a post shared Saturday on Truth Social, Trump wrote, “American Ships, both Military and Commercial, should be allowed to travel, free of charge, through the Panama and Suez Canals! Those Canals would not exist without the United States of America.”

— Rapid Response 47 (@RapidResponse47) April 26, 2025

Trump added that he has instructed Secretary of State Marco Rubio to “immediately take care of, and memorialize” the situation. His comments, first reported by FactSet, come as U.S. companies face rising shipping costs, with tolls for major vessels ranging from $200,000 to over $500,000 per Panama Canal crossing, based on canal authority schedules.

The Suez Canal, operated by Egypt, reportedly saw record revenues of $9.4 billion in 2023, largely driven by American and European shipping amid ongoing Red Sea instability. After a surge in attacks by Houthi militants on commercial ships earlier this year, Trump authorized a sustained military campaign targeting missile and drone sites in northern Yemen. The Pentagon said the strikes were part of an effort to “permanently restore freedom of navigation” for global shipping near the Suez Canal.

Trump has framed the military operations as part of a broader strategy to counter Iranian-backed destabilization efforts across the Middle East.

Meanwhile, in Central America, Trump’s administration is working to counter Chinese influence near the Panama Canal. On April 9th, Defense Secretary Pete Hegseth announced an expanded partnership with Panama to bolster canal security, including a memorandum of understanding allowing U.S. warships and support vessels to move “first and free” through the canal. “The Panama Canal is key terrain that must be secured by Panama, with America, and not China,” Hegseth emphasized during a press conference in Panama City.

American commercial shipping has long depended on the canal, which reduces the shipping route between the U.S. East Coast and Asia by nearly 8,000 miles. About 40% of all U.S. container traffic uses the Panama Canal annually, according to the U.S. Maritime Administration.

The United States originally constructed and controlled the Panama Canal following a monumental effort championed by President Theodore Roosevelt in the early 20th century. After backing Panama’s independence from Colombia in 1903, the U.S. secured the rights to build and operate the canal, which opened in 1914. Although U.S. control ended in 1999 under the Torrijos-Carter Treaties, the canal remains vital to U.S. trade.

2025 Federal Election

Columnist warns Carney Liberals will consider a home equity tax on primary residences

From LifeSiteNews

The Liberals paid a group called Generation Squeeze, led by activist Paul Kershaw, to study how the government could tap into Canadians’ home equity — including their primary residences.

Winnipeg Sun Columnist Kevin Klein is sounding the alarm there is substantial evidence the Carney Liberal Party is considering implementing a home equity tax on Canadians’ primary residences as a potential huge source of funds to bring down the massive national debt their spending created.

Klein wrote in his April 23 column and stated in his accompanying video presentation:

The Canada Mortgage and Housing Corporation (CMHC) — a federal Crown corporation — has investigated the possibility of a home equity tax on more than one occasion, using taxpayer dollars to fund that research. This was not backroom speculation. It was real, documented work.

The Liberals paid a group called Generation Squeeze, led by activist Paul Kershaw, to study how the government could tap into Canadians’ home equity — including their primary residences.

Kershaw, by the way, believes homeowners are “lottery winners” who didn’t earn their wealth but lucked into it. That’s the ideology being advanced to the highest levels of government.

It didn’t stop there. These proposals were presented directly to federal cabinet ministers. That’s on record, and most of those same ministers are now part of Mark Carney’s team as he positions himself as the Liberals’ next leader.

Watch below Klein’s 7-minute, impassionate warning to Canadians about this looming major new tax should the Liberals win Monday’s election.

Klein further adds:

The total home equity held by Canadians is over $4.7 trillion. It’s the largest pool of private wealth in the country. For millions of Canadians — especially baby boomers — it’s the only retirement fund they have. They don’t have big pensions. They have a paid-off house and a hope that it will carry them through their later years. Yet, that’s what Ottawa has quietly been circling.

The Canadian Taxpayer’s Federation has researched this issue and published a report on the alarming amount of new taxation a homeowner equity tax could cost Canadians who sell their homes that have increased in value over the years they have lived in it. It is a shocker!

A Google search on the question, “what is a home equity tax?” returns the response:

A home equity tax, simply put, it’s a proposed levy on the increased value of your home, specifically, on your principal residence. The idea is for Government to raise money by taxing wealth accumulation from rising property values.

The Canadian Taxpayers Federation has provided a Home Equity Tax Calculator Backgrounder to help Canadians understand what the impact of three different types of Home Equity Tax Calculators would have on home owners. The required tax payment resulting from all three is a shocker.

Keep in mind that World Economic Forum policies intend to eventually eliminate all private home ownership and have the state own and control not only all residences, but also eliminate car ownership, and control when and where you may live and travel.

Carney, Trudeau and several other members of the Liberal government in key positions are heavily connected to the WEF.

The Federal Brief That Should Sink Carney

How Canada’s Mainstream Media Lost the Public Trust

Ottawa Confirms China interfering with 2025 federal election: Beijing Seeks to Block Joe Tay’s Election

CBC retracts false claims about residential schools after accusing Rebel News of ‘misinformation’

-

2025 Federal Election2 days ago

The Federal Brief That Should Sink Carney

-

2025 Federal Election2 days ago

How Canada’s Mainstream Media Lost the Public Trust

-

2025 Federal Election2 days ago

Ottawa Confirms China interfering with 2025 federal election: Beijing Seeks to Block Joe Tay’s Election

-

Media21 hours ago

CBC retracts false claims about residential schools after accusing Rebel News of ‘misinformation’

-

John Stossel2 days ago

John Stossel2 days agoClimate Change Myths Part 2: Wildfires, Drought, Rising Sea Level, and Coral Reefs

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoReal Homes vs. Modular Shoeboxes: The Housing Battle Between Poilievre and Carney

-

COVID-192 days ago

COVID-192 days agoNearly Half of “COVID-19 Deaths” Were Not Due to COVID-19 – Scientific Reports Journal

-

Bjorn Lomborg20 hours ago

Bjorn Lomborg20 hours agoNet zero’s cost-benefit ratio is CRAZY high