Business

TikTok on the Clock: US Appeals Court Hits the “Ban” Button

|

The winds of Washington are blowing icy cold for TikTok this December. A federal appeals court panel handed down a ruling today that could send the app packing— or at least force it into a kind of corporate divorce.

The US Court of Appeals for the District of Columbia Circuit has today declared the law threatening TikTok’s existence to be totally constitutional, leaving the platform to fight for its digital life. In short, TikTok has until mid-January to break ties with its Beijing-based parent, ByteDance, or risk an outright ban in the United States. TikTok responded with the following statement: “The Supreme Court has an established historical record of protecting Americans’ right to free speech, and we expect they will do just that on this important constitutional issue. Unfortunately, the TikTok ban was conceived and pushed through based upon inaccurate, flawed and hypothetical information, resulting in outright censorship of the American people. The TikTok ban, unless stopped, will silence the voices of over 170 million Americans here in the US and around the world on January 19th, 2025.” The Free Speech Shuffle TikTok played the First Amendment card, arguing that banning the platform would stomp on Americans’ free speech rights. But the court wasn’t having it, throwing in a little verbal aikido about protecting actual freedom. “The First Amendment exists to protect free speech in the United States,” the court wrote, presumably while straightening its tie in a metaphorical mirror. “Here the Government acted solely to protect that freedom from a foreign adversary nation and to limit that adversary’s ability to gather data on people in the United States.” Translation: TikTok, it’s not you — it’s China. |

|

|

TikTok has been accused of being influenced by the Chinese Communist Party.

|

|

ByteDance’s Legal Tango

TikTok and its parent company, ByteDance, is already planning to appeal to the Supreme Court because apparently, they’re gluttons for punishment. And hey, why not? When you’re staring down a deadline that could nuke your entire US business, you either fight or fold. But here’s where it gets interesting: the same President-elect Donald Trump who once tried to fire TikTok like it was a contestant on The Apprentice now says he’s against a ban. Trump has promised to swoop in and “save” the platform during his second term. The law itself was signed by President Joe Biden in April, marking a rare bipartisan moment in a town otherwise allergic to cooperation. For years, Washington has been gnashing its teeth over TikTok’s ties to the Chinese government, accusing the app of being a national security threat disguised as a dance challenge factory. Of course, critics argue this is about power. TikTok’s cultural dominance has made it an unpredictable disruptor, threatening not only Big Tech’s grip on social media but also giving the average American teen more clout than your local senator. Government officials argue that the app’s voracious appetite for user data could lead to sensitive information, from browsing histories to biometric identifiers, being vacuumed up by the Chinese communist government. But the main issue? The proprietary algorithm, that magical machine-learning potion that keeps you scrolling at 2 a.m., is painted as a weapon of influence — a subtle but powerful propaganda tool ready to tweak your feed for Beijing’s benefit. Except, there’s a catch: a good chunk of the government’s evidence for these claims is locked behind classified curtains. TikTok’s attorneys — and by extension the American public — are left in the dark. |

|

|

More than 170 million Americans use TikTok.

|

|

TikTok Fights Back

TikTok has steadfastly denied being a Chinese Trojan horse, insisting that no evidence exists to prove they’ve ever handed over data to Beijing. As for the algorithm? TikTok says any suggestion of manipulation is pure speculation. Their legal team hammered home that the government’s arguments rely on what might happen in the future — a slippery foundation for ripping apart a platform that’s glued to the cultural zeitgeist. But the Department of Justice isn’t just playing futurist. It has hinted — vaguely and ominously — at unspecified past actions by TikTok and ByteDance in response to Chinese government demands. The key word here is “unspecified,” because whatever receipts the DOJ might have, they’re conveniently out of reach for TikTok’s lawyers, the media, or anyone else. A Courtroom Tango: First Amendment vs. National Security The appeals court panel, a politically mixed trio of judges, seemed as torn as the rest of us about how far Uncle Sam can stretch its First Amendment arguments to justify banning an app with foreign ties. Over two hours of oral arguments in September, the judges volleyed tough questions at both sides. Can the government really shut down a platform just because it’s foreign-owned? the judges asked, channeling TikTok’s core argument. On the flip side: What happens if this platform turns into a covert disinformation campaign during wartime? they wondered, invoking wartime-era laws restricting foreign ownership of broadcast licenses. Both sides twisted themselves into legal yoga poses. TikTok’s lawyer, Andrew Pincus, argued that a private company — even one with foreign owners — deserves constitutional protections. The DOJ’s Daniel Tenny countered that the government has a duty to head off potential foreign interference, even if the threat isn’t fully realized yet. $2 Billion in Data Defenses TikTok itself hasn’t just been sitting back while lawyers spar. The company claims it’s invested over $2 billion to fortify its US data, including setting up Project Texas — a heavily marketed initiative to store American user data on servers managed by Oracle. ByteDance has also floated the idea of a comprehensive draft agreement that it says could have eased Washington’s fears years ago. But according to TikTok, the Biden administration ghosted them, walking away from the negotiating table without offering a viable path forward. The DOJ insists the draft didn’t go far enough, but skeptics wonder if the government’s hardline stance is less about national security and more about flexing control over Big Tech. Divestment Drama Washington’s solution to the TikTok dilemma sounds deceptively simple: ByteDance should sell the US arm of TikTok. However attorneys for the company argue that such a divestment would be a logistical and commercial nightmare. And without TikTok’s algorithm—intellectual property that Beijing is unlikely to let go of—the app would lose its magic. Imagine TikTok without its eerily intuitive feed: it’d be MySpace 2.0, a ghost town for millennials waxing nostalgic. Still, some sharks smell blood in the water. Billionaire Frank McCourt and former Treasury Secretary Steven Mnuchin have rallied a consortium with over $20 billion in informal commitments to snap up TikTok’s US operations. TikTok isn’t going down without a fight and it’s bringing allies to the battlefield. The company’s legal challenge has been bundled with lawsuits from several content creators, who argue that losing the platform would gut their livelihoods, and conservative influencers who claim a ban would silence their political speech. TikTok, ever the sugar daddy, is footing the legal bills for its creators — a savvy PR move if ever there was one. The Clock is Ticking If TikTok’s Hail Mary appeal to the Supreme Court fails, it’ll be up to President Trump’s Justice Department to enforce the ban. That means app stores would have to scrub TikTok from their offerings, and hosting services would be barred from supporting it. And what happens to the millions of creators, small businesses, and teenagers who’ve turned TikTok into a cultural juggernaut? Well, they’ll probably migrate to Instagram Reels or YouTube Shorts—platforms that coincidentally happen to be owned by US tech giants who’ve been salivating at the thought of TikTok’s demise. This is far from over. |

|

If you value free speech and privacy, subscribe to Reclaim The Net. Each issue we publish is a commitment to defend these critical rights, providing insights and actionable information to protect and promote liberty in the digital age.

Despite our wide readership, less than 0.2% of our readers contribute financially. With your support, we can do more than just continue; we can amplify voices that are often suppressed and spread the word about the urgent issues of censorship and surveillance. Consider making a modest donation — just $5, or whatever amount you can afford. Your contribution will empower us to reach more people, educate them about these pressing issues, and engage them in our collective cause. Thank you for considering a contribution. Each donation not only supports our operations but also strengthens our efforts to challenge injustices and advocate for those who cannot speak out.

Thank you

|

Sam Cooper

Sam Cooper

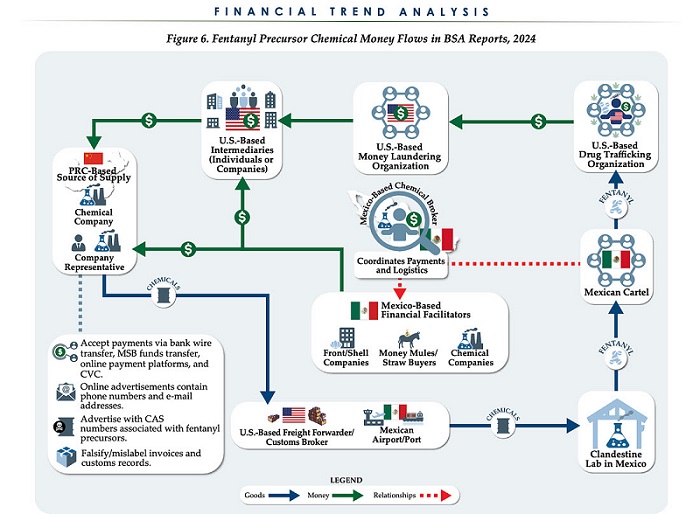

The U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN) has identified $1.4 billion in fentanyl-linked suspicious transactions, naming China, Mexico, Canada, and India as key foreign touchpoints in the global production and laundering network. The analysis, based on 1,246 Bank Secrecy Act filings submitted in 2024, tracks financial activity spanning chemical purchases, trafficking logistics, and international money laundering operations.

The data reveals that Mexico and the People’s Republic of China were the two most frequently named foreign jurisdictions in financial intelligence gathered by FinCEN. Most of the flagged transactions originated in U.S. cities, the report notes, due to the “domestic nature” of Bank Secrecy Act data collection. Among foreign jurisdictions, Mexico, China, Hong Kong, and Canada were cited most often in fentanyl-related financial activity.

The FinCEN report points to Mexico as the epicenter of illicit fentanyl production, with Mexican cartels importing precursor chemicals from China and laundering proceeds through complex financial routes involving U.S., Canadian, and Hong Kong-based actors.

The findings also align with testimony from U.S. and Canadian law enforcement veterans who have told The Bureau that Chinese state-linked actors sit atop a decentralized but industrialized global fentanyl economy—supplying precursors, pill presses, and financing tools that rely on trade-based money laundering and professional money brokers operating across North America.

“Filers also identified PRC-based subjects in reported money laundering activity, including suspected trade-based money laundering schemes that leveraged the Chinese export sector,” the report says.

A point emphasized by Canadian and U.S. experts—including former U.S. State Department investigator Dr. David Asher—that professional Chinese money laundering networks operating in North America are significantly commanded by Chinese Communist Party–linked Triad bosses based in Ontario and British Columbia—is not explored in detail in this particular FinCEN report.¹

Chinese chemical manufacturers—primarily based in Guangdong, Zhejiang, and Hebei provinces—were repeatedly cited for selling fentanyl precursors via wire transfers and money service businesses. These sales were often facilitated through e-commerce platforms, suggesting that China’s global retail footprint conceals a lethal underground market—one that ultimately fuels a North American public health crisis. In many cases, the logistics were sophisticated: some Chinese companies even offered delivery guarantees and customs clearance for precursor shipments, raising red flags for enforcement officials.

While China’s industrial base dominates the global fentanyl supply chain, Mexican cartels are the next most prominent state-like actors in the ecosystem—but the report emphasizes that Canada and India are rising contributors.

“Subjects in other foreign countries—including Canada, the Dominican Republic, and India—highlight the presence of alternative suppliers of precursor chemicals and fentanyl,” the report says.

“Canada-based subjects were primarily identified by Bank Secrecy Act filers due to their suspected involvement in drug trafficking organizations allegedly sourcing fentanyl and other drugs from traditional drug source countries, such as Mexico,” it explains, adding that banking intelligence “identified activity indicative of Canada-based individuals and companies purchasing precursor chemicals and laboratory equipment that may be related to the synthesis of fentanyl in Canada. Canada-based subjects were primarily reported with addresses in the provinces of British Columbia and Ontario.”

FinCEN also flagged activity from Hong Kong-based shell companies—often subsidiaries or intermediaries for Chinese chemical exporters. These entities were used to obscure the PRC’s role in transactions and to move funds through U.S.-linked bank corridors.

Breaking down the fascinating and deadly world of Chinese underground banking used to move fentanyl profits from American cities back to producers, the report explains how Chinese nationals in North America are quietly enlisted to move large volumes of cash across borders—without ever triggering traditional wire transfers.

These networks, formally known as Chinese Money Laundering Organizations (CMLOs), operate within a global underground banking system that uses “mirror transfers.” In this system, a Chinese citizen with renminbi in China pays a local broker, while the U.S. dollar equivalent is handed over—often in cash—to a recipient in cities like Los Angeles or New York who may have no connection to the original Chinese depositor aside from their role in the laundering network. The renminbi, meanwhile, is used inside China to purchase goods such as electronics, which are then exported to Mexico and delivered to cartel-linked recipients.

FinCEN reports that US-based money couriers—often Chinese visa holders—were observed depositing large amounts of cash into bank accounts linked to everyday storefront businesses, including nail salons and restaurants. Some of the cash was then used to purchase cashier’s checks, a common method used to obscure the origin and destination of the funds. To banks, the activity might initially appear consistent with a legitimate business. However, modern AI-powered transaction monitoring systems are increasingly capable of flagging unusual patterns—such as small businesses conducting large or repetitive transfers that appear disproportionate to their stated operations.

On the Mexican side, nearly one-third of reports named subjects located in Sinaloa and Jalisco, regions long controlled by the Sinaloa Cartel and Cartel Jalisco Nueva Generación. Individuals in these states were often cited as recipients of wire transfers from U.S.-based senders suspected of repatriating drug proceeds. Others were flagged as originators of payments to Chinese chemical suppliers, raising alarms about front companies and brokers operating under false pretenses.

The report outlines multiple cases where Mexican chemical brokers used generic payment descriptions such as “goods” or “services” to mask wire transfers to China. Some of these transactions passed through U.S.-based intermediaries, including firms owned by Chinese nationals. These shell companies were often registered in unrelated sectors—like marketing, construction, or hardware—and exhibited red flags such as long dormancy followed by sudden spikes in large transactions.

Within the United States, California, Florida, and New York were most commonly identified in fentanyl-related financial filings. These locations serve as key hubs for distribution and as collection points for laundering proceeds. Cash deposits and peer-to-peer payment platforms were the most cited methods for fentanyl-linked transactions, appearing in 54 percent and 51 percent of filings, respectively.

A significant number of flagged transactions included slang terms and emojis—such as “blues,” “ills,” or blue dots—in memo fields. Structured cash deposits were commonly made across multiple branches or ATMs, often linked to otherwise legitimate businesses such as restaurants, salons, and trucking firms.

FinCEN also tracked a growing number of trade-based laundering schemes, in which proceeds from fentanyl sales were used to buy electronics and vaping devices. In one case, U.S.-based companies owned by Chinese nationals made outbound payments to Chinese manufacturers, using funds pooled from retail accounts and shell companies. These goods were then shipped to Mexico, closing the laundering loop.

Another key laundering method involved cryptocurrency. Nearly 10 percent of all fentanyl-related reports involved virtual currency, with Bitcoin the most commonly cited, followed by Ethereum and Litecoin. FinCEN flagged twenty darknet marketplaces as suspected hubs for fentanyl distribution and cited failures by some digital asset platforms to catch red-flag activity.

Overall, FinCEN warns that fentanyl-linked funds continue to enter the U.S. financial system through loosely regulated or poorly monitored channels, even as law enforcement ramps up enforcement. The Drug Enforcement Administration reported seizures of over 55 million counterfeit fentanyl pills in 2024 alone.

The broader pattern is unmistakable: precursor chemicals flow from China, manufacturing occurs in Mexico, Canada plays an increasing role in chemical acquisition and potential synthesis, and drugs and proceeds flood into the United States, supported by global financial tools and trade structures. The same infrastructure that enables lawful commerce is being manipulated to sustain the deadliest synthetic drug crisis in modern history.

The Bureau is a reader-supported publication.

To receive new posts and support my work, consider becoming a free or paid subscriber.

Invite your friends and earn rewards

MxM News

MxM News

Quick Hit:

Canada has announced it will roll back retaliatory tariffs on automakers and pause several other tariff measures aimed at the United States. The move, unveiled by Finance Minister François-Philippe Champagne, is designed to give Canadian manufacturers breathing room to adjust their supply chains and reduce reliance on American imports.

Key Details:

- Canada will suspend 25% tariffs on U.S. vehicles for automakers that maintain production, employment, and investment in Canada.

- A broader six-month pause on tariffs for other U.S. imports is intended to help Canadian sectors transition to domestic sourcing.

- A new loan facility will support large Canadian companies that were financially stable before the tariffs but are now struggling.

Diving Deeper:

Ottawa is shifting its approach to the escalating trade war with Washington, softening its economic blows in a calculated effort to stabilize domestic manufacturing. On Tuesday, Finance Minister François-Philippe Champagne outlined a new set of trade policies that provide conditional relief from retaliatory tariffs that have been in place since March. Automakers, the hardest-hit sector, will now be eligible to import U.S. vehicles duty-free—provided they continue to meet criteria that include ongoing production and investment in Canada.

“From day one, the government has reacted with strength and determination to the unjust tariffs imposed by the United States on Canadian goods,” Champagne stated. “We’re giving Canadian companies and entities more time to adjust their supply chains and become less dependent on U.S. suppliers.”

The tariff battle, which escalated in April with Canada slapping a 25% tax on U.S.-imported vehicles, had caused severe anxiety within Canada’s auto industry. John D’Agnolo, president of Unifor Local 200, which represents Ford employees in Windsor, warned the BBC the situation “has created havoc” and could trigger a recession.

Speculation about a possible Honda factory relocation to the U.S. only added to the unrest. But Ontario Premier Doug Ford and federal officials were quick to tamp down the rumors. Honda Canada affirmed its commitment to Canadian operations, saying its Alliston facility “will operate at full capacity for the foreseeable future.”

Prime Minister Mark Carney reinforced the message that the relief isn’t unconditional. “Our counter-tariffs won’t apply if they (automakers) continue to produce, continue to employ, continue to invest in Canada,” he said during a campaign event. “If they don’t, they will get 25% tariffs on what they are importing into Canada.”

Beyond the auto sector, Champagne introduced a six-month tariff reprieve on other U.S. imports, granting time for industries to explore domestic alternatives. He also rolled out a “Large Enterprise Tariff Loan Facility” to support big businesses that were financially sound prior to the tariff regime but have since been strained.

While Canada has shown willingness to ease its retaliatory measures, there’s no indication yet that the U.S. under President Donald Trump will reciprocate. Nevertheless, Ottawa signaled its openness to further steps to protect Canadian businesses and workers, noting that “additional measures will be brought forward, as needed.”

Conservative Party urges investigation into Carney plan to spend $1 billion on heat pumps

Mark Carney To Ban Free Speech if Elected

Expert Medical Record Reviews Of The Two Girls In Texas Who Purportedly Died of Measles

Disability rights panel calls out Canada, US states pushing euthanasia on sick patients

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoRCMP Whistleblowers Accuse Members of Mark Carney’s Inner Circle of Security Breaches and Surveillance

-

Also Interesting2 days ago

Also Interesting2 days agoBetFury Review: Is It the Best Crypto Casino?

-

Autism2 days ago

Autism2 days agoRFK Jr. Exposes a Chilling New Autism Reality

-

COVID-192 days ago

COVID-192 days agoCanadian student denied religious exemption for COVID jab takes tech school to court

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoBureau Exclusive: Chinese Election Interference Network Tied to Senate Breach Investigation

-

International2 days ago

International2 days agoUK Supreme Court rules ‘woman’ means biological female

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoNeil Young + Carney / Freedom Bros

-

Health2 days ago

Health2 days agoWHO member states agree on draft of ‘pandemic treaty’ that could be adopted in May