Energy

Ottawa’s emissions cap—all pain, no gain

From the Fraser Institute

By: Julio Mejía, Elmira Aliakbari and Tegan Hill

According to a recent analysis by the Conference Board of Canada think-tank, the cap could reduce Canada’s GDP by up to $1 trillion between 2030 and 2040, eliminate up to 151,000 jobs by 2030, reduce federal government revenue by up to $151 billion between 2030 and 2040, and reduce Alberta government revenue by up to $127 billion over the same period.

According to an announcements last week by Premier Danielle Smith, the Alberta government will use the Alberta Sovereignty within a United Canada Act to challenge Ottawa’s proposal to cap greenhouse gas emissions from the oil and gas sector at 35 per cent below 2019 levels by 2030.

Premier Smith, who said the cap will harm the economy and represents an overstep of federal authority, also plans to prevent emissions data from individual oil and gas companies from being shared with Ottawa. While the federal government said the cap is necessary to fight climate change, several studies suggest the cap will impose significant costs on Canadians without yielding detectable environmental benefits.

According to a recent report by Deloitte, a leading audit and consulting firm, the cap will force Canadian firms to curtail oil production by 626,000 barrels per day by 2030 or by approximately 10.0 per cent of the expected production—and curtail gas production by approximately 12.0 per cent.

Deloitte estimates that Alberta will be hit hardest, with 3.6 per cent less investment, almost 70,000 fewer jobs, and a 4.5 per cent decrease in the province’s economic output (i.e. GDP) by 2040. Ontario will lose 15,000 jobs and $2.3 billion from its economy by 2040. And Quebec will lose more than 3,000 jobs and $0.4 billion from its economy during the same period.

Overall, the country will experience an economic loss equivalent to 1.0 per cent of the value of the entire economy (GDP), translating into lower wages, the loss of nearly 113,000 jobs and a 1.3 per cent reduction in government tax revenues. Canada’s inflation-adjusted GDP growth in 2023 was a paltry 1.3 per cent, so a 1 per cent reduction would be a significant economic loss.

Deloitte’s findings echo previous studies. According to a recent analysis by the Conference Board of Canada think-tank, the cap could reduce Canada’s GDP by up to $1 trillion between 2030 and 2040, eliminate up to 151,000 jobs by 2030, reduce federal government revenue by up to $151 billion between 2030 and 2040, and reduce Alberta government revenue by up to $127 billion over the same period.

Similarly, another recent study published by the Fraser Institute found that the cap would reduce production and exports, leading to at least $45 billion in lost economic activity in 2030 alone, accompanied by a substantial drop in government revenue.

Crucially, these huge economic costs to Canadians will come without any discernable environmental benefits. Even if Canada entirely shut down its oil and gas industry by 2030, eliminating all GHG emissions from the sector, the resulting reduction in global GHG emissions would amount to a mere four-tenths of one per cent with virtually no impact on the climate or any detectable environmental, health or safety benefits.

Given the demand for fossil fuels, constraining oil and gas production and exports in Canada would likely merely shift production to other countries with lower environmental and human rights standards such as Iran, Russia and Venezuela. Consequently, global GHG emissions would increase, not decrease. No other major oil and gas-producing country has imposed a similar cap on its leading export sector.

The Trudeau government’s proposed cap, which still must pass the House and Senate, would further strain an already struggling Canadian economy, and to make matters worse, do virtually nothing to improve the environment. The government should cancel the cap plan given the economic costs and nonexistent environmental benefits.

Julio Mejía

Policy Analyst

Elmira Aliakbari

Director, Natural Resource Studies, Fraser Institute

Tegan Hill

Director, Alberta Policy, Fraser Institute

From the Fraser Institute

Two recent events exemplify the fundamental irrationality that is Canada’s electric vehicle (EV) policy.

First, the Carney government re-committed to Justin Trudeau’s EV transition mandate that by 2035 all (that’s 100 per cent) of new car sales in Canada consist of “zero emission vehicles” including battery EVs, plug-in hybrid EVs and fuel-cell powered vehicles (which are virtually non-existent in today’s market). This policy has been a foolish idea since inception. The mass of car-buyers in Canada showed little desire to buy them in 2022, when the government announced the plan, and they still don’t want them.

Second, President Trump’s “Big Beautiful” budget bill has slashed taxpayer subsidies for buying new and used EVs, ended federal support for EV charging stations, and limited the ability of states to use fuel standards to force EVs onto the sales lot. Of course, Canada should not craft policy to simply match U.S. policy, but in light of policy changes south of the border Canadian policymakers would be wise to give their own EV policies a rethink.

And in this case, a rethink—that is, scrapping Ottawa’s mandate—would only benefit most Canadians. Indeed, most Canadians disapprove of the mandate; most do not want to buy EVs; most can’t afford to buy EVs (which are more expensive than traditional internal combustion vehicles and more expensive to insure and repair); and if they do manage to swing the cost of an EV, most will likely find it difficult to find public charging stations.

Also, consider this. Globally, the mining sector likely lacks the ability to keep up with the supply of metals needed to produce EVs and satisfy government mandates like we have in Canada, potentially further driving up production costs and ultimately sticker prices.

Finally, if you’re worried about losing the climate and environmental benefits of an EV transition, you should, well, not worry that much. The benefits of vehicle electrification for climate/environmental risk reduction have been oversold. In some circumstances EVs can help reduce GHG emissions—in others, they can make them worse. It depends on the fuel used to generate electricity used to charge them. And EVs have environmental negatives of their own—their fancy tires cause a lot of fine particulate pollution, one of the more harmful types of air pollution that can affect our health. And when they burst into flames (which they do with disturbing regularity) they spew toxic metals and plastics into the air with abandon.

So, to sum up in point form. Prime Minister Carney’s government has re-upped its commitment to the Trudeau-era 2035 EV mandate even while Canadians have shown for years that most don’t want to buy them. EVs don’t provide meaningful environmental benefits. They represent the worst of public policy (picking winning or losing technologies in mass markets). They are unjust (tax-robbing people who can’t afford them to subsidize those who can). And taxpayer-funded “investments” in EVs and EV-battery technology will likely be wasted in light of the diminishing U.S. market for Canadian EV tech.

If ever there was a policy so justifiably axed on its failed merits, it’s Ottawa’s EV mandate. Hopefully, the pragmatists we’ve heard much about since Carney’s election victory will acknowledge EV reality.

Kenneth P. Green

Senior Fellow, Fraser Institute

![]()

From the Daily Caller News Foundation

By Audrey Streb

President Donald Trump issued an executive order calling for the end of green energy subsidies by strengthening provisions in the One Big Beautiful Bill Act on Monday night, citing national security concerns and unnecessary costs to taxpayers.

The order argues that a heavy reliance on green energy subsidies compromise the reliability of the power grid and undermines energy independence. Trump called for the U.S. to “rapidly eliminate” federal green energy subsidies and to “build upon and strengthen” the repeal of wind and solar tax credits remaining in the reconciliation law in the order, directing the Treasury Department to enforce the phase-out of tax credits.

“For too long, the Federal Government has forced American taxpayers to subsidize expensive and unreliable energy sources like wind and solar,” the order states. “Reliance on so-called ‘green’ subsidies threatens national security by making the United States dependent on supply chains controlled by foreign adversaries.”

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here.

Thank you!

Former President Joe Biden established massive green energy subsidies under his signature 2022 Inflation Reduction Act (IRA), which did not receive a single Republican vote.

The reconciliation package did not immediately terminate Biden-era federal subsidies for green energy technology, phasing them out over time instead, though some policy experts argued that drawn-out timelines could lead to an indefinite continuation of subsidies. Trump’s executive order alludes to potential loopholes in the bill, calling for a review by Secretary of the Treasury Scott Bessent to ensure that green energy projects that have a “beginning of construction” tax credit deadline are not “circumvented.”

Additionally, the executive order directs the U.S. to end taxpayer support for green energy supply chains that are controlled by foreign adversaries, alluding to China’s supply chain dominance for solar and wind. Trump also specifically highlighted costs to taxpayers, market distortions and environmental impacts of subsidized green energy development in explaining the policy.

Ahead of the reconciliation bill becoming law, Trump told Republicans that “we’ve got all the cards, and we are going to use them.” Several House Republicans noted that the president said he would use executive authority to enhance the bill and strictly enforce phase-outs, which helped persuade some conservatives to back the bill.

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

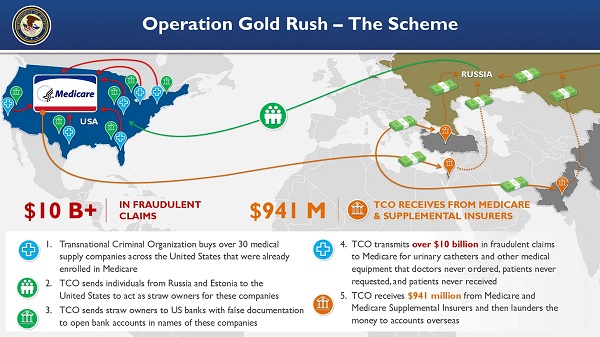

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Fraser Institute1 day ago

Fraser Institute1 day agoBefore Trudeau average annual immigration was 617,800. Under Trudeau number skyrocketted to 1.4 million annually

-

Crime2 days ago

Crime2 days ago“This is a total fucking disaster”

-

International2 days ago

International2 days agoChicago suburb purchases childhood home of Pope Leo XIV

-

Daily Caller2 days ago

Daily Caller2 days ago‘I Know How These People Operate’: Fmr CIA Officer Calls BS On FBI’s New Epstein Intel

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is already killing the disabled. It’s about to get worse

-

Daily Caller2 days ago

Daily Caller2 days agoBlackouts Coming If America Continues With Biden-Era Green Frenzy, Trump Admin Warns

-

Red Deer2 days ago

Red Deer2 days agoJoin SPARC in spreading kindness by July 14th

-

Business1 day ago

Business1 day agoPrime minister can make good on campaign promise by reforming Canada Health Act