Also Interesting

Medicare 101 Guide

Medicare was established in the United States as a national health insurance program for those 65 or older. Medicare Parts A, B, and D are the parts of Medicare that most people pay for individually. The program is chiefly funded through a payroll tax, though recipients are responsible for a monthly premium and cost-sharing. Medicare provides benefits to eligible beneficiaries who meet specific eligibility requirements. Participants are encouraged to enrol in a supplemental private supplementary policy through Medicare Advantage or private fee-for-service plans. The premium for these policies is paid by the beneficiary, not the federal government. Those eligible for Medicare enrolment must be at least 65 years old. Those under 65 must be permanently disabled or suffer from specific terminal illnesses.

1. What is Medicare?

Medicare is the federal healthcare program for seniors and the disabled. Its age eligibility rules are confusing, so some of those who qualify get stuck in a coverage gap that leaves them unable to afford necessary medical care. The government has been trying to help out with an updated guide on how Medicare works, but there’s still confusion about what benefits people should expect from this program. Here are some things you should know about Medicare from a healthcare perspective to make the most of your coverage and stay healthy for as long as possible.

It provides medical services to those covered by Parts A and B of the plan, which covers hospital expenses and doctor visits, respectively. Part C is Medicare Advantage (MA), which offers additional benefits such as prescription drug coverage, outpatient care, and hearing aids or eyeglasses for seniors. Those who enrol in Medicare Part D receive coverage for prescription drug costs.

2. Medicare Part A

Part A covers most of the hospital expenses for Medicare beneficiaries. The amount of coverage is based on financial needs determined by complicated formulas adjusted annually for inflation. You might wonder why this coverage gap exists in the first place, but it’s important to remember that Medicare is also a government program—i.e., you pay taxes into it, and the government gives you healthcare back. The government limits the hospital expenses covered by Part A each year.

People who have certain types of employer-sponsored insurance—such as pensions or other retirement plans—also get Medicare Part A coverage. These people are known as “dual eligible” which means they are both Medicare beneficiaries and members of an eligible group.

3. Medicare Part B

Part B covers the costs of doctors and outpatient care, such as doctor office visits and in-patient hospital stays. Medicare beneficiaries must pay a monthly premium for that coverage. Recipients also have to pay a deductible each year for any covered services. You must pay the deductible for each service before Medicare kicks in to cover the remainder.

The Social Security Administration (SSA) sets cost-of-living increases yearly. The program also covers certain preventive services with no cost sharing. You can expect to pay about $4 for your doctor visits and up to $150 for prescription drugs.

4. Medicare Part C (Medicare Advantage)

It is privatized Medicare, offered by health insurance companies and paid directly to Medicare beneficiaries. It covers various healthcare benefits and services, from screenings to hospital stays, with cost-sharing or copayments. It’s private, beneficiaries don’t have to pay anything for their plans, and neither does the government for most of those benefits.

Private insurance companies offer these plans and don’t have an annual limit on Medicare benefits. They can cover the same services as Part B and cost less because they aren’t required to follow Medicare’s formula for setting premiums and deductibles. Beneficiaries must know precisely what’s covered by each plan.

5. Medicare Part D

Part D is the prescription drug coverage offered through Medicare Part A. It covers the costs of most, but not all, prescription drugs. Some of the covered drugs are generic versions of brand-name drugs. You have to pay a monthly premium for your prescription drug coverage, and there is no cost-sharing requirement as with other parts of Medicare Part A. There’s no annual limit on the total drug costs covered, but there is a limit on what you pay out-of-pocket each year for prescriptions. Part D plans also have pre-set out-of-pocket limits that beneficiaries must pay before their plans kick in again. Beneficiaries pay their premiums and cost-sharing annually, which are set by the insurance companies offering the plans.

6. How to Enroll in Medicare?

Most people eligible for Medicare enrol in the program through their employers. If you’re self-employed, it’s wise to enroll in employer-sponsored health insurance as a dual eligible. If you’re not covered by an employer-provided plan and don’t qualify for Medicaid or a state plan, you can enroll in Medicare at any time during open enrollment. Plans often allow you to pick which parts of Medicare the federal government will cover and which ones you want to be responsible for paying out of pocket.

7. How is Medicare Paid For?

The government pays a fixed amount to beneficiaries based on their income and a sliding scale for those who are disabled or elderly. There are also premiums for MA plans. Medicare is a federal program, so it is subject to all the laws passed by Congress that regulate the establishment of insurance companies and the prosecution of fraud committed against them. Participants have access to all the information about their benefits from the Social Security Administration, which maintains a database with all Medicare enrolees’ personal information.

Medicare is a good program that helps seniors when they need it most. The government will pay its share of the costs of hospitalization or doctor visits during its 50-year lifetime. Since Medicare pays so much less than private insurance, beneficiaries often have to pay more out-of-pocket for many services, especially prescription drugs and other medical supplies.

In today’s competitive online casino market, BetFury emerges as an innovative platform that seamlessly blends cryptocurrency integration with classic gaming excitement. The platform has attracted both casual players and experienced gamblers with its engaging user experience, wide range of games, and attractive rewards that keep users coming back. BetFury’s sleek design and robust technical foundation ensure fast, secure, and entertaining gameplay. Visit https://betfury.com to explore its offerings and learn more about its unique features.

This review examines BetFury in detail, highlighting its key strengths, benefits, and the data that underpins its success. The platform’s commitment to transparency and fairness – enabled by advanced blockchain technology – sets it apart. Regular updates and a strong focus on user satisfaction have earned BetFury a loyal community and a reputation for excellence. In this comprehensive review, we provide clear insights supported by data and genuine user feedback to explain why BetFury is rapidly becoming a top choice in the online gaming world.

Platform Overview

BetFury is a next-generation online casino that merges traditional gambling with modern blockchain technology. Operating on a decentralized system, it guarantees fairness and security for every game and transaction. The user-friendly interface caters to both newcomers and seasoned players. With support for multiple cryptocurrencies, BetFury offers flexibility and convenience to a global audience. Its transparent operational framework provides clear details about game mechanics and bonus structures.

Continuous improvements and a solid technological foundation ensure that the platform remains reliable and innovative. This steady evolution reinforces trust among users and demonstrates BetFury’s commitment to quality. Its ability to adapt quickly to emerging trends makes it a

trailblazer in online gaming.

Key Features and Advantages

BetFury offers an impressive array of features designed to cater to diverse gaming preferences. A vast selection of games is one of its core strengths. Whether you prefer classic slots or immersive live dealer experiences, BetFury delivers. The platform is optimized for both desktop and mobile devices, ensuring smooth gameplay regardless of your setup. Key advantages include:

● Fast transaction speeds

● Transparent gaming mechanics

● Generous bonus structures

● A diverse game portfolio

● Multi-cryptocurrency support

The table below summarizes essential performance metrics:

Metric Value

Average Transaction Time 2 seconds

Game Variety 10k+ titles

Daily Active Users 15k+

Supported Cryptocurrencies 10+

These features combine to create a superior gaming environment that meets modern demands with high security and fairness.

Game Selection and Diversity

The game selection at BetFury is both extensive and varied. Hosting over 10000 titles, the platform offers slots, table games, and live dealer options. Each game is designed for immersive entertainment and reliable performance. Collaboration with top-tier developers ensures high-quality graphics and sound. The variety allows players to enjoy familiar favorites and explore new experiences. Seasonal tournaments and special events add extra excitement and bonus opportunities. The breakdown of game categories is as follows:

Game Category Number of Titles

Slots 9095+

Table Games 290+

Live Dealer 1055+

Specialty Games 30+

Regular updates and a robust performance record reinforce BetFury’s commitment to delivering an engaging, dynamic gaming experience.

Bonuses, Rewards, and Loyalty Programs

BetFury’s bonus and rewards system is one of its most attractive features. New players benefit from a generous welcome bonus, while regular users enjoy daily cashback and special promotions. The loyalty program rewards players progressively, offering increased benefits as they advance through tiers. Each bonus is clearly defined and easily accessible, adding excitement to every session. The table below illustrates common bonus offerings:

Bonus Type Offer Details

Welcome Bonus Up to 150% deposit bonus

Daily Cashback 10% on losses

Referral Bonus 5% commission on referrals

Loyalty Rewards Progressive tier benefits

Many players praise the rewards system for enhancing their overall experience. As one satisfied user put it, “BetFury transformed my online gaming experience; the rewards and smooth interface are unmatched!” This positive feedback underscores how the bonus structures keep players engaged and continuously rewarded.

Payment Methods and Security Measures

BetFury supports a wide range of payment methods, primarily through various cryptocurrencies. This ensures that transactions are fast, secure, and convenient. The platform uses advanced encryption and security protocols to protect user data and funds. Deposits and withdrawals are processed swiftly, which is crucial for a seamless gaming experience. Key payment options include:

● Bitcoin (BTC)

● Ethereum (ETH)

● Litecoin (LTC)

● Ripple (XRP)

● Other altcoins

The integration of blockchain technology provides additional transparency, making every transaction verifiable and tamper-proof. Continuous monitoring by a dedicated security team further safeguards the platform. These measures instill confidence in players, making BetFury a trusted name in online gaming.

Community, Customer Support, and Performance

BetFury has built a vibrant community that contributes to its dynamic ecosystem. Regular tournaments and community events foster a sense of camaraderie among players. The customer support team is available 24/7, ensuring that any issues are resolved quickly and efficiently. Users appreciate the friendly, knowledgeable assistance, which enhances their overall experience. Performance metrics further validate the platform’s reliability:

Performance Metric Value

Uptime 99.9%

Average Load Time 1.3 seconds

Customer Support Rating 4.9/5

Response Time Under 1 minute

Ongoing software updates and active developer engagement help maintain a stable and responsive system. These efforts have resulted in high user satisfaction and consistent performance, reinforcing BetFury’s position as a leader in the online gaming industry.

A Minor Drawback

Despite its many strengths, BetFury has one minor drawback. The interface can feel a bit overwhelming due to the extensive array of options and detailed information. However, this slight complexity is quickly outweighed by the platform’s overall functionality and continuous improvements.

Final Thoughts and Conclusion

BetFury is a leading online gaming platform that uniquely combines traditional casino experiences with innovative blockchain technology. Its robust features, diverse game selection, rewarding bonus structures, and reliable security measures make it an excellent choice for players. An active community and responsive customer support further enhance the overall experience. BetFury continues to impress with its forward-thinking approach and commitment to excellence.

Overall, BetFury delivers a cutting-edge gaming experience characterized by rapid transactions, engaging gameplay, and attractive rewards. Its blend of advanced technology, diverse options, and user-focused design makes it a standout choice for both newcomers and experienced players. With only a minor drawback in interface complexity, BetFury remains one of the most promising online casino platforms available today.

Alberta’s online gaming scene continues to grow, with players across the province seeking trusted platforms offering attractive incentives. One name that has captured attention recently is Casino Days, a platform known for its diverse game selection and generous promotions. For those interested in maximizing their gaming experience, the current Casino Days bonus options provide an excellent starting point. These offers are tailored to appeal to both new and seasoned players, enhancing the overall appeal of Casino Days in the Alberta gaming community.

Understanding Casino Days: A Brief Overview

Casino Days has quickly established itself as a reputable online casino for Canadian players. Launched in 2020, the platform was created with a player-first philosophy, emphasizing user-friendly navigation, secure transactions, and, most importantly, exciting promotional offers. Alberta players, in particular, have found value in Casino Days due to its seamless accessibility and a game library that includes thousands of slots, live casino games, and progressive jackpots.

The Appeal of Casino Days Bonus Offers

What sets Casino Days apart is its commitment to rewarding players. From generous welcome bonuses to ongoing promotions, Alberta players have ample opportunities to boost their bankrolls. Typically, new players are greeted with a match bonus on their initial deposit, often accompanied by free spins on popular slot games. These offers help players extend their playtime and explore a wider range of games without immediate risk.

Additionally, Casino Days frequently updates its bonus structures to stay competitive, ensuring Alberta players always have something new to look forward to. Reload bonuses, cashback offers, and exclusive game promotions keep the excitement alive long after the initial sign-up.

Expert Insights: Trustworthy Information Matters

When navigating the world of online gaming, having access to reliable information is essential. This is where GamblingInformation.com becomes an invaluable resource. Managed by industry veterans with extensive experience, the site provides players with thoroughly analyzed insights into various online casinos, including Casino Days. Ed Roberts, the main author of GamblingInformation.com, is particularly known for his deep dives into bonus structures and promotional fairness, ensuring that readers receive the most accurate and trustworthy information available.

For Alberta players seeking clarity about Casino Days bonus offers, GamblingInformation.com delivers detailed evaluations, making it easier to understand wagering requirements, game eligibility, and withdrawal terms.

How Casino Days Supports Responsible Gaming

Casino Days doesn’t just focus on entertainment; it places a strong emphasis on responsible gaming. Players from Alberta can benefit from a variety of tools designed to encourage safe gambling habits. Features like deposit limits, time reminders, and self-exclusion options allow users to maintain control over their gaming activities.

According to the Government of Alberta, responsible gambling tools are essential in helping individuals enjoy gaming as a form of entertainment without adverse consequences. Casino Days aligns with these recommendations, fostering a safe and enjoyable environment for its players.

Payment Methods Tailored for Alberta Players

Image from Unsplash

Casino Days offers a wide array of payment options that cater specifically to Canadian users. Alberta players can easily make deposits and withdrawals using trusted methods such as Interac, Visa, Mastercard, and popular e-wallet services. All transactions are protected by advanced encryption technology, ensuring a secure experience from start to finish.

Processing times are competitive, with most withdrawals being processed within 24 to 48 hours. This commitment to efficiency and security makes Casino Days a preferred choice for players looking for reliable financial transactions.

Game Variety and User Experience

Beyond bonuses, Casino Days impresses with its extensive game selection. Alberta players have access to thousands of slot titles, including classic favorites and the latest releases from top-tier developers. The live casino section offers an immersive experience, complete with real dealers and high-definition streaming.

The platform’s user interface is designed for simplicity and ease of use. Whether accessed on desktop or mobile devices, Casino Days ensures that navigation is intuitive, allowing players to focus on enjoying their favorite games.

Promotions Beyond the Welcome Bonus

Casino Days understands the importance of keeping players engaged over time. In addition to the initial welcome package, Alberta players can benefit from ongoing promotions that include weekly reload bonuses, free spins, and prize drops. These recurring offers provide continuous value, encouraging players to return and explore new gaming opportunities.

Seasonal promotions and special events further enhance the Casino Days experience. These limited-time offers often come with exciting prizes, such as free bets, cash rewards, or exclusive game access, adding an extra layer of excitement to the platform.

Customer Support and Community Engagement

Reliable customer support is a cornerstone of any successful online casino, and Casino Days excels in this area. Alberta players can access 24/7 customer service through live chat and email, ensuring that assistance is always available when needed.

Moreover, Casino Days fosters a sense of community by engaging with players through social media channels and promotional events. This approach helps build a loyal player base and keeps users informed about the latest bonuses and platform updates.

Security Measures and Licensing

Casino Days operates under a license from the Government of Curacao, adhering to strict regulatory standards. While not a Canadian authority, this licensing ensures that the platform maintains high levels of fairness and security. Independent audits and RNG (Random Number Generator) certifications further validate the integrity of the games offered.

In addition to regulatory compliance, Casino Days employs advanced cybersecurity measures to protect player data. Encryption protocols and secure servers safeguard personal and financial information, providing peace of mind to Alberta players.

Mobile Gaming Experience

For Alberta players who prefer gaming on the go, Casino Days delivers an exceptional mobile experience. The platform is fully optimized for smartphones and tablets, with no need for additional downloads. Players can access the full suite of games, manage their accounts, and claim bonuses directly from their mobile browsers.

This flexibility allows players to enjoy their favorite games anytime, anywhere, making Casino Days a convenient choice for busy lifestyles.

Future Prospects: What’s Next for Casino Days?

As the online gaming industry continues to evolve, Casino Days remains committed to innovation. The platform regularly expands its game library and explores new promotional opportunities to enhance the player experience.

For Alberta players, this commitment translates into more exciting bonuses, improved gameplay features, and ongoing improvements to security and user experience. Casino Days’ proactive approach ensures that it will remain a top choice for Canadian players well into the future.

Whether you’re new to online gaming or a seasoned player, Casino Days provides a platform that combines excitement, security, and value, making it a standout option in Alberta’s thriving online casino landscape.

Casino Days Bonus Offers Available for Players from Alberta

Is HNIC Ready For The Winnipeg Jets To Be Canada’s Heroes?

Province to expand services provided by Alberta Sheriffs: New policing option for municipalities

No Matter The Winner – My Canada Is Gone

-

Business1 day ago

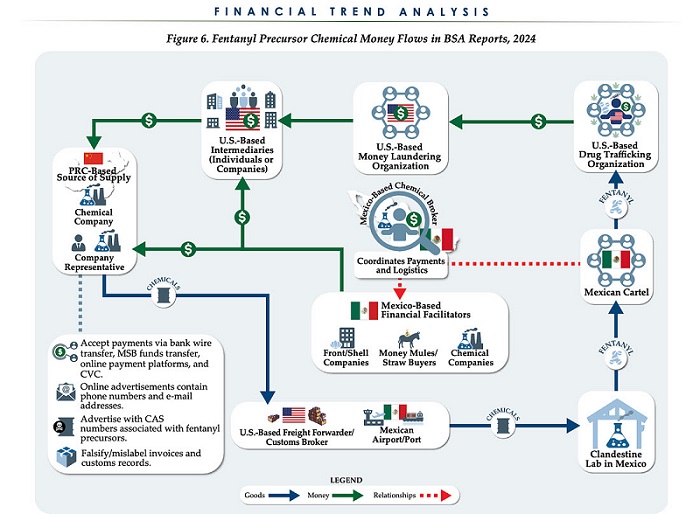

Business1 day agoChina, Mexico, Canada Flagged in $1.4 Billion Fentanyl Trade by U.S. Financial Watchdog

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoTucker Carlson Interviews Maxime Bernier: Trump’s Tariffs, Mass Immigration, and the Oncoming Canadian Revolution

-

espionage2 days ago

espionage2 days agoEx-NYPD Cop Jailed in Beijing’s Transnational Repatriation Plot, Canada Remains Soft Target

-

Business2 days ago

Business2 days agoDOGE Is Ending The ‘Eternal Life’ Of Government

-

2025 Federal Election1 day ago

2025 Federal Election1 day agoBREAKING from THE BUREAU: Pro-Beijing Group That Pushed Erin O’Toole’s Exit Warns Chinese Canadians to “Vote Carefully”

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoCanada drops retaliatory tariffs on automakers, pauses other tariffs

-

Daily Caller1 day ago

Daily Caller1 day agoDOJ Releases Dossier Of Deported Maryland Man’s Alleged MS-13 Gang Ties

-

Daily Caller1 day ago

Daily Caller1 day agoTrump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid