Economy

Trudeau balloons bureaucracy by 42 per cent, adds 108,000 employees

From the Canadian Taxpayers Federation

Author: Franco Terrazzano

The Trudeau government’s addiction to hiring bureaucrats continues unabated.

The government added another 10,525 bureaucrats to its payroll last year, bringing the size of the federal bureaucracy up to 367,772, according to data from the Treasury Board of Canada Secretariat released July 11.

“Was there a bureaucrat shortage in Ottawa before Trudeau took over?” said Franco Terrazzano, Federal Director of the Canadian Taxpayers Federation. “Canadians need a more efficient government, not a bloated government full of highly paid bureaucrats.”

Since Prime Minister Justin Trudeau came to power in 2015, the feds have added 108,793 new bureaucrats to the government dole – an increase of 42 per cent.

Canada’s population grew by just 14 per cent during the same time period. Had the bureaucracy only increased with population growth, there would be 72,491 fewer federal employees today.

Table: Size of federal bureaucracy, per TBS data

|

Year (As of March 31) |

Number of federal bureaucrats |

|

2016 |

258,979 |

|

2017 |

262,696 |

|

2018 |

273,571 |

|

2019 |

287,983 |

|

2020 |

300,450 |

|

2021 |

319,601 |

|

2022 |

335,957 |

|

2023 |

357,247 |

|

2024 |

367,772 |

It isn’t just the size of the federal bureaucracy that’s ballooning – the cost is too.

The cost of the federal payroll hit $67.4 billion in 2023, a record high, according to a report from the Parliamentary Budget Officer, Ottawa’s independent, non-partisan budget watchdog.

That’s a 68 per cent increase over 2016, when the federal payroll sat at 40.2 billion.

The Trudeau government also handed out more than one million pay raises to bureaucrats over the past four years alone, according to government records obtained by the CTF.

The government has consistently declined to reveal how much those raises cost taxpayers.

The federal government also rubberstamped more than $1.5 billion in bonuses for bureaucrats since 2015.

Meanwhile, despite the bureaucratic hiring spree, spending on consultants has also skyrocketed under the Trudeau government. Consultant spending now sits at $21.6 billion annually.

Given the rash of bonuses and pay raises, on top of spate of new hires, Canadians might wonder: how well are things running in Ottawa?

Well, the reviews are in and the results aren’t good.

Less than 50 per cent of the government’s own performance targets are consistently met by federal departments within each year, according to a March 2023 report from the PBO.

“We’ve seen an increase in the number of public servants and in public expenditures, but year after year, despite the fact that departments choose their performance indicators and the targets, they don’t seem to be getting significantly better at reaching them,” Budget Officer Yves Giroux testified to a parliamentary committee in March 2024.

The average annual compensation for full-time federal bureaucrats is $125,300, when pay, pension, and other perks are accounted for, according to the PBO.

Meanwhile, data from Statistics Canada suggests the average annual salary among all full-time workers in Canada was less than $70,000 in 2023.

“The feds have hired tens of thousands of extra bureaucrats, handed out more than one million raises and rubber stamped hundreds of million in bonuses in recent years and still can’t deliver good services,” Terrazzano said. “Any government that cares about balancing the budget must take air out of the ballooning bureaucracy.”

It finally happened. Canada received a federal budget earlier this month, after more than a year without one. It’s far from a budget that’s great. It’s far from what many expected and distant from what the country needs. But it still passed.

With the budget vote drama now behind us, there may be space for some general observations beyond the details of the concerning deficits and debt. What kind of budget did Canada get?

Haultain’s Substack is a reader-supported publication.

To receive new posts and support our work, please consider becoming a free or paid subscriber.

Try it out.

For a government that built its political identity on social-program expansion and moralized spending, Budget 2025 arrives wearing borrowed clothing. It speaks in the language of productivity, infrastructure, and capital formation, the diction of grown-up economics, yet keeps the full spending reflex of the Trudeau era. The result feels like a cabinet trying to change its fiscal costume without changing the character inside it. Time will tell, to be fair, but it feels like more rhetoric, and we have seen this same rhetoric before lead to nothing. So, I remain skeptical of what they say and how they say it.

The government insists it has found a new path, one where public investment leads private growth. That sounds bold. However, it is more a rebranding than a reform. It is a shift in vocabulary, not in discipline.

A comparison with past eras makes this clear.

Jean Chrétien and Paul Martin did not flirt with restraint; they executed it. Their budgets were cut deeply, restored credibility, and revived Canada’s fiscal health when it was most needed. The Chrétien years were unsentimental. Political capital was spent so financial capital could return. Ottawa shrank so the country could grow. Budget 2025 tries to invoke their spirit but not their actions. Nothing in this plan resembles the structural surgery of the mid 1990s.

Stephen Harper, by contrast, treated balanced budgets as policy and principle. Even during the global financial crisis, his government used stimulus as a bridge, not a way of life. It cut taxes widely and consistently, limited public service growth, and placed the long-term burden on restraint rather than rhetoric. Budget 2025 nods toward Harper’s focus on productivity and capital assets, yet it rejects the tax relief and spending controls that made his budgets coherent.

Then there is Justin Trudeau, the high tide of redistribution, vacuous identity politics, and deficit-as-virtue posturing. Ottawa expanded into an ideological planner for everything, including housing, climate, childcare, inclusion portfolios, and every new identity category. Much of that ideological scaffolding consisted of mere words, weakening the principle of equality under the law and encouraging the government to referee culture rather than administer policy.

Budget 2025 is the first hint of retreat from that style. The identity program fireworks are dimmer, though they have not disappeared. The social policy boosterism is quieter. Perhaps fiscal gravity has begun to whisper in the prime minister’s ear.

However, one cannot confuse tone for transformation.

Spending is still vast. Deficits grew. The new fiscal anchor, balancing only the operating budget, is weaker than the one it replaced. The budget relies on the hopeful assumption that Ottawa’s capital spending will attract private investment on a scale that economists politely describe as ambitious.

The housing file illustrates the contradiction. The budget announces new funding for the construction of purpose-built rentals and a larger federal role in modular and subsidized housing builds. These are presented as productivity measures, yet they continue the Trudeau-era instinct to centralize housing policy rather than fix the levers that matter. Permitting delays, zoning rigidity, municipal approvals, and labour shortages continue to slow actual construction. Ottawa spends, but the foundations still cure at the same pace.

Defence spending tells the same story. Budget 2025 offers incremental funding and some procurement gestures, but it avoids the core problem: Canada’s procurement system is broken. Delays stretch across decades. Projects become obsolete before contracts are signed. The system cannot buy a ship, an aircraft, or an armoured vehicle without cost overruns and missed timelines. Spending more through this machinery will waste time and money. It adds motion, not capability.

Most importantly, the structural problems remain untouched: no regulatory reform for major projects, no tax competitiveness agenda, no strategy for shrinking a federal bureaucracy that has grown faster than the economy it governs. Ottawa presides over a low-productivity country but insists that a new accounting framework will solve what decades of overregulation and policy clutter have created. More bluster.

To receive new posts and support our work, please consider becoming a free or paid subscriber.

From an Alberta vantage, the pivot is welcome but inadequate. The economy that pays for Confederation, energy, mining, agriculture, and transportation receives more rhetorical respect in Budget 2025, yet the same regulatory thicket that blocks pipelines and mines remains intact. The government praises capital formation but still undermines the key sectors that generate it.

Budget 2025 tries to walk like Chrétien and talk like Harper while spending like Trudeau. That is not a transformation; it is a costume change. The country needed a budget that prioritized growth rooted in tangible assets and real productivity. What it got instead is a rhetorical turn without the courage to cut, streamline, or reform.

Canada does not require a new budgeting vocabulary. It requires a government willing to govern in the best interest of the country.

Haultain’s Substack is a reader-supported publication.

Help us bring you more quality research and commentary.

From the Fraser Institute

By Tegan Hill and Elmira Aliakbari

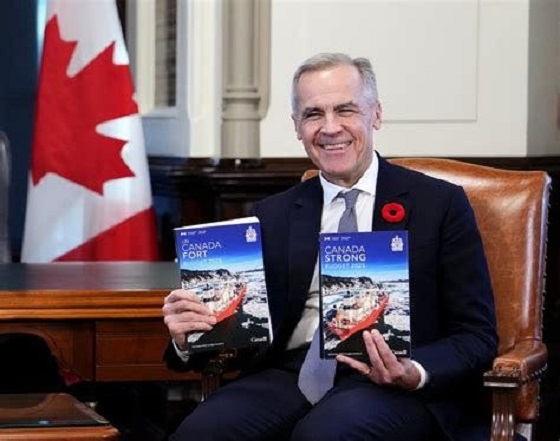

On the campaign trail and after he became prime minister, Mark Carney has repeatedly promised to make Canada an “energy superpower.” But, as evidenced by its first budget, the Carney government has simply reaffirmed the failed plans of the past decade and embraced the damaging energy policies of the Trudeau government.

First, consider the Trudeau government’s policy legacy. There’s Bill C-69 (the “no pipelines act”), the new electricity regulations (which aim to phase out natural gas as a power source starting this year), Bill C-48 (which bans large oil tankers off British Columbia’s northern coast and limit Canadian exports to international markets), the cap on emissions only from the oil and gas sector (even though greenhouse gas emissions have the same effect on the environment regardless of the source), stricter regulations for methane emissions (again, impacting the oil and gas sector), and numerous “net-zero” policies.

According to a recent analysis, fully implementing these measures under Trudeau government’s emissions reduction plan would result in 164,000 job losses and shrink Canada’s economic output by 6.2 per cent by the end of the decade compared to a scenario where we don’t have these policies in effect. For Canadian workers, this will mean losing $6,700 (annually, on average) by 2030.

Unfortunately, the Carney government’s budget offers no retreat from these damaging policies. While Carney scrapped the consumer carbon tax, he plans to “strengthen” the carbon tax on industrial emitters and the cost will be passed along to everyday Canadians—so the carbon tax will still cost you, it just won’t be visible.

There’s also been a lot of buzz over the possible removal of the oil and gas emissions cap. But to be clear, the budget reads: “Effective carbon markets, enhanced oil and gas methane regulations, and the deployment at scale of technologies such as carbon capture and storage would create the circumstances whereby the oil and gas emissions cap would no longer be required as it would have marginal value in reducing emissions.” Put simply, the cap remains in place, and based on the budget, the government has no real plans to remove it.

Again, the cap singles out one source (the oil and gas sector) of carbon emissions, even when reducing emissions in other sectors may come at a lower cost. For example, suppose it costs $100 to reduce a tonne of emissions from the oil and gas sector, but in another sector, it costs only $25 a tonne. Why force emissions reductions in a single sector that may come at a higher cost? An emission is an emission regardless of were it comes from. Moreover, like all these policies, the cap will likely shrink the Canadian economy. According to a 2024 Deloitte study, from 2030 to 2040, the cap will shrink the Canadian economy (measured by inflation-adjusted GDP) by $280 billion, and result in lower wages, job losses and a decline in tax revenue.

At the same time, the Carney government plans to continue to throw money at a range of “green” spending and tax initiatives. But since 2014, the combined spending and forgone revenue (due to tax credits, etc.) by Ottawa and provincial governments in Ontario, Quebec, British Columbia and Alberta totals at least $158 billion to promote the so-called “green economy.” Yet despite this massive spending, the green sector’s contribution to Canada’s economy has barely changed, from 3.1 per cent of Canada’s economic output in 2014 to 3.6 per cent in 2023.

In his first budget, Prime Minister Carney largely stuck to the Trudeau government playbook on energy and climate policy. Ottawa will continue to funnel taxpayer dollars to the “green economy” while restricting the oil and gas sector and hamstringing Canada’s economic potential. So much for becoming an energy superpower.

Carney fails to undo Trudeau’s devastating energy policies

Trump says release the Epstein files

Calgary mayor should retain ‘blanket rezoning’ for sake of Calgarian families

Sports 50/50 Draws: Make Sure You Read The Small Print

Cost of bureaucracy balloons 80 per cent in 10 years: Public Accounts

Alberta Offers Enormous Advantages for AI Data Centres

National Crisis Approaching Due To The Carney Government’s Centrally Planned Green Economy

-

Carbon Tax21 hours ago

Carney fails to undo Trudeau’s devastating energy policies

-

Business17 hours ago

Budget 2025: Ottawa Fakes a Pivot and Still Spends Like Trudeau

-

Health17 hours ago

Health17 hours agoTens of thousands are dying on waiting lists following decades of media reluctance to debate healthcare

-

Business2 days ago

Business2 days agoI Was Hired To Root Out Bias At NIH. The Nation’s Health Research Agency Is Still Sick

-

Business2 days ago

Business2 days agoLarge-scale energy investments remain a pipe dream

-

armed forces1 day ago

armed forces1 day agoCanada At Risk Of Losing Control Of Its Northern Territories

-

International1 day ago

International1 day agoCanada’s lost decade in foreign policy

-

Opinion12 hours ago

Opinion12 hours agoLandmark 2025 Study Says Near-Death Experiences Can’t Be Explained Away