Business

Proposed changes to Canada’s Competition Act could kneecap our already faltering economy

From the Macdonald Laurier Institute

Aaron Wudrick, for Inside Policy

No party wants to be seen as soft on “big business” but that is a bad reason to pass potentially harmful, counterproductive competition policy legislation.

The recent federal budget was widely panned – in particular by the entrepreneurial class – for its proposal to raise the capital gains inclusion rate. As it turns out, “soak the rich” might sound like clever politics (it’s not) but it’s definitely a poor narrative if your goal is to incentivize and encourage risk-taking and investment.

But while this damaging measure in the federal budget has at least drawn plenty of public ire, other harmful legislative changes are afoot that are getting virtually no attention at all. They’re contained in Bill C-59 – the omnibus bill still wending its way through Parliament to enact measures contained in last fall’s economic statement – and consist of major proposed amendments to Canada’s Competition Act. The lack of coverage and debate on these changes is all the more concerning given that, if enacted, they could have a long-term negative impact on our economy comparable to the capital gains inclusion rate hike.

Worst of all, the most potentially damaging changes weren’t even in the original bill, but were brought forward by the NDP at the House of Commons Standing Committee on Finance, and are lifted directly from a previous submission made to the committee by the Commissioner of Competition himself. In effect, they would change competition law to put a new onus on businesses to prove a negative: that having a large market share isn’t harmful to consumers.

MPs on the committee have acknowledged they don’t really understand the changes – they involve a “concentration index” described as “the sum of the squares of the market shares of the suppliers or customers” – but the government itself previously cast doubt on the need for this additional change. It’s obvious that a lot of politics are at play here: no party wants to be seen as soft on “big business.” But this is about much more than “big business.” It’s about whether we want to enshrine in law unfounded, and potentially very harmful, assumptions about how competition operates in the real world.

The changes in question are what are known in legal circles as “structural presumptions” – which, as the name implies, involve creating presumptions in law based on market “structure” – in this case, regarding the concentration level of a given market. Presumptions in law matter, because they determine which side in a competition dispute – the regulatory authority, or the impugned would-be merging parties – bears the burden of proof.

So why is this a bad idea? There are at least three reasons.

First of all, the very premise is faulty: most economists consider concentration measures alone (as opposed to market power) to be a poor proxy for the level of competition that prevails in a given market. In fact, competition for customers often increases concentration.

This may strike most people as counterintuitive. But because robust competition often leads to one company in particular offering lower prices, higher quality, or more innovative products, those who break from the pack tend to attract more customers and increase their market share. In this respect, higher concentration can actually signal more, rather than less, competition.

Second, structural presumptions for mergers are not codified in the US or any other developed country other than Germany (and even then, at a 40 percent combined share rather than 30 percent). In other words, at a time when Canada’s economy is suffering from the significant dual risks of stalled productivity growth and net foreign investment flight, the amendments proposed by the NDP would introduce one of the most onerous competition laws in the world.

There is a crucial distinction between parliamentarians putting such wording into legislation – which bind the courts – and regulatory agencies putting them in enforcement guidelines, which leave courts with a degree of discretion.

Incorporating structural presumptions into legislation surpasses what most advanced economies do and could lead to false negatives (blocking mergers that would, if permitted, actually benefit consumers), chill innovation (as companies seeking to up their game in the hopes of selling or merging are deterred from even bothering), and result in more orphaned Canadian businesses (as companies elect not to acquire Canadian operations on global transactions).

Finally, the impact on merger review will not be a simplification but will likely just fetter the discretion and judgment of the expert and impartial Competition Tribunal in determining which mergers are truly harmful for consumers and give more power to the Competition Bureau, the head of which is appointed by the federal Cabinet. Although the Competition Bureau is considered an independent law enforcement agency, it must still make its case before a court (the Tribunal, in this case).The battleground at the Tribunal will shift from focusing on the likely effect of the merger on consumers to instead entertaining arguments between the Bureau’s and companies’ opposing arguments about defining the relevant market and shares.

Even if, after further study, the government decided that rebuttable structural presumptions are desirable, C-59 already repeals subsection 92(2) of the Competition Act, which allows the Tribunal to develop the relevance of market shares through case law – a far better process than a blanket rule in legislation. Nothing prevents the Bureau from incorporating structural presumptions as an enforcement screen for mergers in its guidelines, which is what the United States has done for decades, rather than putting strict (and therefore inflexible) metrics into statute and regulations.

No one disputes that Canada needs a healthy dose of competition in a wide range of sectors. But codifying dubious rules around mergers risks doing more harm than good. In asking for structural presumptions to be codified, the Competition Bureau is missing the mark. Most proposed mergers that will get caught by these changes should in fact be permitted on the basis that consumers would be better off – and the uncertainty of being an extreme outlier on the global stage in terms of competition policy will create yet another disincentive to start and grow businesses in Canada.

This is the opposite of what Canada needs right now. Rather than looking for ill-advised shortcuts that entangle more companies in litigation and punt disputes about market definition rather than effects to the Tribunal, the Bureau should be focusing on doing its existing job better: building evidence-backed cases against mergers that would actually harm Canadians.

Aaron Wudrick is the domestic policy director at the Macdonald-Laurier Institute.

From the Fraser Institute

According to a recent study, living standards in Canada have declined over the past five years. And the country’s economic growth has been “ugly.” Crucially, all 10 provinces are experiencing this economic stagnation—there are no exceptions to Canada’s “ugly” growth record. In 2026, reversing this trend should be the top priority for the Carney government and provincial governments across the country.

Indeed, demographic and economic data across the country tell a remarkably similar story over the past five years. While there has been some overall economic growth in almost every province, in many cases provincial populations, fuelled by record-high levels of immigration, have grown almost as quickly. Although the total amount of economic production and income has increased from coast to coast, there are more people to divide that income between. Therefore, after we account for inflation and population growth, the data show Canadians are not better off than they were before.

Let’s dive into the numbers (adjusted for inflation) for each province. In British Columbia, the economy has grown by 13.7 per cent over the past five years but the population has grown by 11.0 per cent, which means the vast majority of the increase in the size of the economy is likely due to population growth—not improvements in productivity or living standards. In fact, per-person GDP, a key indicator of living standards, averaged only 0.5 per cent per year over the last five years, which is a miserable result by historic standards.

A similar story holds in other provinces. Prince Edward Island, Nova Scotia, Quebec and Saskatchewan all experienced some economic growth over the past five years but their populations grew at almost exactly the same rate. As a result, living standards have barely budged. In the remaining provinces (Newfoundland and Labrador, New Brunswick, Ontario, Manitoba and Alberta), population growth has outstripped economic growth, which means that even though the economy grew, living standards actually declined.

This coast-to-coast stagnation of living standards is unique in Canadian history. Historically, there’s usually variation in economic performance across the country—when one region struggles, better performance elsewhere helps drive national economic growth. For example, in the early 2010s while the Ontario and Quebec economies recovered slowly from the 2008/09 recession, Alberta and other resource-rich provinces experienced much stronger growth. Over the past five years, however, there has not been a “good news” story anywhere in the country when it comes to per-person economic growth and living standards.

In reality, Canada’s recent record-high levels of immigration and population growth have helped mask the country’s economic weakness. With more people to buy and sell goods and services, the overall economy is growing but living standards have barely budged. To craft policies to help raise living standards for Canadian families, policymakers in Ottawa and every provincial capital should remove regulatory barriers, reduce taxes and responsibly manage government finances. This is the great policy challenge for governments across the country in 2026 and beyond.

Ben Eisen

Senior Fellow, Fraser Institute

Jake Fuss

Director, Fiscal Studies, Fraser Institute

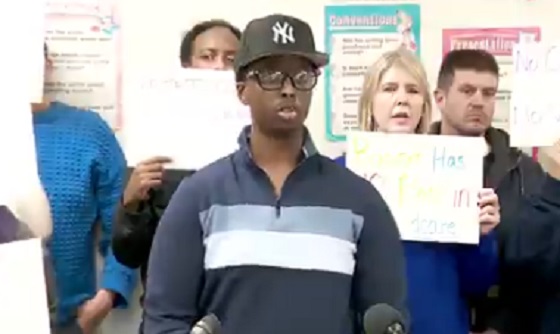

A Minneapolis day care run by Somali immigrants is claiming that a mysterious break-in wiped out its most sensitive records, even as police say officers were never told that anything was actually stolen — a discrepancy that’s drawing sharp attention amid Minnesota’s spiraling child care fraud scandal.

According to the center’s manager, Nasrulah Mohamed, someone forced their way into Nakomis Day Care Center earlier this week by entering through a rear kitchen area, damaging a wall and accessing the office. Mohamed told reporters the intruder made off with “important documentation,” including children’s enrollment records, employee files, and checkbooks tied to the facility’s operations.

But a preliminary report from the Minneapolis Police Department tells a different story. Police say no loss was reported to officers at the time of the call. While the department confirmed the center later contacted police with additional information, an updated report was not immediately available.

Video released by the day care purporting to show damage from the incident depicts a hole punched through drywall inside what appears to be a utility closet, with stacks of cinder blocks visible just behind the wall — imagery that has only fueled skepticism as investigators continue to unravel what authorities have described as one of the largest fraud schemes ever tied to Minnesota’s human services programs.

Mohamed blamed the alleged break-in on fallout from a viral investigation by YouTuber Nick Shirley, who recently toured nearly a dozen Minnesota day care sites while questioning whether they were legitimately operating. Shirley’s video has racked up more than 110 million views. Mohamed insisted the coverage unfairly targeted Somali operators and said his center has since received what he described as hateful and threatening messages.

A manager at the Nokomis Daycare Center in Minneapolis detailed "extensive vandalism" at the facility during a Wednesday news conference.

Manager Nasrulah Mohamed reported that the suspect stole important employee and client documents, an incident he attributed to YouTuber Nick… pic.twitter.com/71nNTSXdTT

— FOX 9 (@FOX9) December 31, 2025

“This is devastating news, and we don’t know why this is targeting our Somali community,” Mohamed said, calling Shirley’s reporting false. Nakomis Day Care Center was not among the facilities featured in the video.

The break-in claim surfaced as law enforcement and federal officials continue to expose a massive fraud network centered in Minneapolis, involving food assistance, housing, and child care payments. Authorities say at least $1 billion has already been identified as fraudulent, with federal prosecutors warning the total could climb as high as $9 billion. Ninety-two people have been charged so far, 80 of them Somali immigrants.

Late Tuesday, the U.S. Department of Health and Human Services announced it was freezing all federal child care payments to Minnesota unless the state can prove the funds are being used lawfully. The payments totaled roughly $185 million in 2025 alone.

Minnesota Gov. Tim Walz, under intensifying scrutiny for allowing fraud to metastasize for years, responded by attacking the Trump administration rather than addressing the substance of the findings. “This is Trump’s long game,” Walz wrote on X Tuesday night, claiming the administration was politicizing fraud enforcement to defund programs — despite federal officials pointing to documented abuse and ongoing criminal cases.

Meanwhile, questions continue to swirl around facilities already flagged by investigators. Reporters visiting several sites highlighted in Shirley’s video found at least one — Quality “Learing” Center — operating with children inside despite state officials previously saying it had been shut down. The Minnesota Department of Children, Youth, and Families later issued a confusing clarification, saying the center initially reported it would close but later claimed it would remain open.

As Minnesota scrambles to respond to the funding freeze and mounting arrests, the conflicting accounts surrounding the Nakomis Day Care incident underscore a broader problem confronting state leaders: a system so riddled with gaps and contradictions that even basic facts — like whether records were actually stolen — are now in dispute, while taxpayers are left holding the bill.

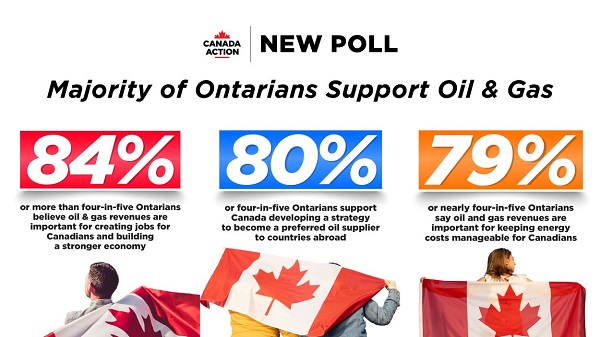

New Poll Shows Ontarians See Oil & Gas as Key to Jobs, Economy, and Trade

Alberta Next Panel calls for less Ottawa—and it could pay off

“Magnitude cannot be overstated”: Minnesota aid scam may reach $9 billion

Largest fraud in US history? Independent Journalist visits numerous daycare centres with no children, revealing massive scam

US Under Secretary of State Slams UK and EU Over Online Speech Regulation, Announces Release of Files on Past Censorship Efforts

Sweden Fixed What Canada Won’t Even Name

Socialism vs. Capitalism

-

Business1 day ago

Business1 day agoDark clouds loom over Canada’s economy in 2026

-

Business1 day ago

Business1 day agoThe Real Reason Canada’s Health Care System Is Failing

-

Business1 day ago

Business1 day agoFederal funds FROZEN after massive fraud uncovered: Trump cuts off Minnesota child care money

-

Addictions1 day ago

Addictions1 day agoCoffee, Nicotine, and the Politics of Acceptable Addiction

-

Opinion1 day ago

Opinion1 day agoGlobally, 2025 had one of the lowest annual death rates from extreme weather in history

-

International10 hours ago

International10 hours agoTrump confirms first American land strike against Venezuelan narco networks

-

Business10 hours ago

How convenient: Minnesota day care reports break-in, records gone

-

Business9 hours ago

The great policy challenge for governments in Canada in 2026