Business

Canada should match or eclipse Trump’s red-tape cutting plan

From the Fraser Institute

With all eyes focused on WWT (World War Tariff), another Trump initiative was quietly put in place last week in one of the now-signature Trump “flood the zone” initiative waves.

On Jan. 31, the Trump administration published an executive order (EO) titled “Unleashing Prosperity Through Deregulation,” and as regulatory reform initiatives go, well, it’s every anti-regulatory analyst’s dream as “each new regulation issued, at least 10 prior regulations be identified for elimination.”

For reference, one of Canada’s strongest regulatory-reform efforts (in British Columbia back in 2001) only called for a 2-for-1 ratio. Although B.C.’s effort did somewhat foreshadow Trump’s, in that it created something of a DOGE (Department of Government Efficiency) when the B.C. government appointed an actual minister of deregulation to oversee the effort rather than leaving it to the bureaucracy to reform itself. And it worked. By 2004, 37 per cent of regulatory requirements in B.C. had been eliminated (exceeding the initial one-third target).

Trump’s new plan is less explicit in defining regulations, but it makes sure that new regulations cost less than the 10 regulations they replace. “For fiscal year 2025,” reads the EO, “the heads of all agencies are directed to ensure that the total incremental cost of all new regulations, including repealed regulations, being finalized this year, shall be significantly less than zero, and any new incremental costs associated with new regulations shall, to the extent permitted by law, be offset by the elimination of existing costs associated with at least 10 prior regulations.”

And Trump’s plan will put regulators in government agencies on a permanent diet, as a “total amount of incremental costs… will be allowed for each agency in issuing new regulations and repealing regulations for each fiscal year after fiscal year 2025.”

Why does this matter to Canadians?

Because, unlike those few years of B.C. regulatory reform, Canada has been wrapping itself in regulatory red-tape for decades, making our economy less competitive globally and with the United States. Between 2006 to 2018, the number of restrictive regulations in Canada grew from about 66,000 to 72,000. And according to the Canadian Federation of Independent Business, the cost of regulation from all three levels of government to Canadian businesses totalled $38.8 billion in 2020, for a total of 731 million hours—the equivalent of nearly 375,000 fulltime jobs.

Clearly, Canada has a regulatory problem—our governments generate seemingly endless spools of regulatory red tape, which keep Canadian businesses tangled in inefficiency, wasted labour and non-competitiveness. President Trump’s new regulatory reform initiative will further increase the “red-tape gap” between Canada and the U.S.

Policymakers in Ottawa and the provinces would do well to learn about Canada’s experiences with deregulatory programs and strive to match—or beat—the new U.S. regulatory reform efforts before a massive lack of regulatory competitiveness becomes a serious problem, adding insult to injury on top of World War Tariff.

Kenneth P. Green

MxM News

MxM News

Quick Hit:

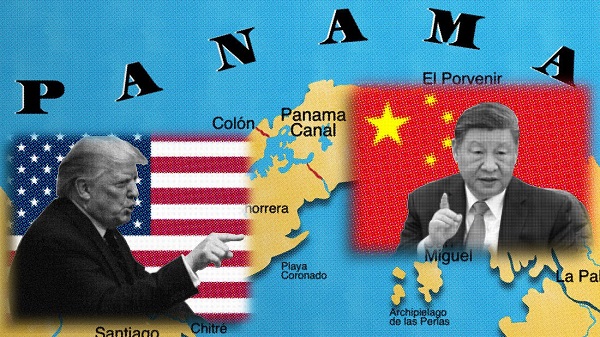

President Donald Trump is pushing for U.S. ships to transit the Panama and Suez canals without paying tolls, arguing the waterways would not exist without America.

Key Details:

-

In a Saturday Truth Social post, Trump said, “American Ships, both Military and Commercial, should be allowed to travel, free of charge, through the Panama and Suez Canals! Those Canals would not exist without the United States of America.”

-

Trump directed Secretary of State Marco Rubio to “immediately take care of, and memorialize” the issue, signaling a potential new diplomatic initiative with Panama and Egypt.

-

The Panama Canal generated about $3.3 billion in toll revenue in fiscal 2023, while the Suez Canal posted a record $9.4 billion. U.S. vessels account for roughly 70% of Panama Canal traffic, according to government figures.

Diving Deeper:

President Donald Trump is pressing for American ships to receive free passage through two of the world’s most critical shipping lanes—the Panama and Suez canals—a move he argues would recognize the United States’ historic role in making both waterways possible. In a post shared Saturday on Truth Social, Trump wrote, “American Ships, both Military and Commercial, should be allowed to travel, free of charge, through the Panama and Suez Canals! Those Canals would not exist without the United States of America.”

— Rapid Response 47 (@RapidResponse47) April 26, 2025

Trump added that he has instructed Secretary of State Marco Rubio to “immediately take care of, and memorialize” the situation. His comments, first reported by FactSet, come as U.S. companies face rising shipping costs, with tolls for major vessels ranging from $200,000 to over $500,000 per Panama Canal crossing, based on canal authority schedules.

The Suez Canal, operated by Egypt, reportedly saw record revenues of $9.4 billion in 2023, largely driven by American and European shipping amid ongoing Red Sea instability. After a surge in attacks by Houthi militants on commercial ships earlier this year, Trump authorized a sustained military campaign targeting missile and drone sites in northern Yemen. The Pentagon said the strikes were part of an effort to “permanently restore freedom of navigation” for global shipping near the Suez Canal.

Trump has framed the military operations as part of a broader strategy to counter Iranian-backed destabilization efforts across the Middle East.

Meanwhile, in Central America, Trump’s administration is working to counter Chinese influence near the Panama Canal. On April 9th, Defense Secretary Pete Hegseth announced an expanded partnership with Panama to bolster canal security, including a memorandum of understanding allowing U.S. warships and support vessels to move “first and free” through the canal. “The Panama Canal is key terrain that must be secured by Panama, with America, and not China,” Hegseth emphasized during a press conference in Panama City.

American commercial shipping has long depended on the canal, which reduces the shipping route between the U.S. East Coast and Asia by nearly 8,000 miles. About 40% of all U.S. container traffic uses the Panama Canal annually, according to the U.S. Maritime Administration.

The United States originally constructed and controlled the Panama Canal following a monumental effort championed by President Theodore Roosevelt in the early 20th century. After backing Panama’s independence from Colombia in 1903, the U.S. secured the rights to build and operate the canal, which opened in 1914. Although U.S. control ended in 1999 under the Torrijos-Carter Treaties, the canal remains vital to U.S. trade.

2025 Federal Election

Columnist warns Carney Liberals will consider a home equity tax on primary residences

From LifeSiteNews

The Liberals paid a group called Generation Squeeze, led by activist Paul Kershaw, to study how the government could tap into Canadians’ home equity — including their primary residences.

Winnipeg Sun Columnist Kevin Klein is sounding the alarm there is substantial evidence the Carney Liberal Party is considering implementing a home equity tax on Canadians’ primary residences as a potential huge source of funds to bring down the massive national debt their spending created.

Klein wrote in his April 23 column and stated in his accompanying video presentation:

The Canada Mortgage and Housing Corporation (CMHC) — a federal Crown corporation — has investigated the possibility of a home equity tax on more than one occasion, using taxpayer dollars to fund that research. This was not backroom speculation. It was real, documented work.

The Liberals paid a group called Generation Squeeze, led by activist Paul Kershaw, to study how the government could tap into Canadians’ home equity — including their primary residences.

Kershaw, by the way, believes homeowners are “lottery winners” who didn’t earn their wealth but lucked into it. That’s the ideology being advanced to the highest levels of government.

It didn’t stop there. These proposals were presented directly to federal cabinet ministers. That’s on record, and most of those same ministers are now part of Mark Carney’s team as he positions himself as the Liberals’ next leader.

Watch below Klein’s 7-minute, impassionate warning to Canadians about this looming major new tax should the Liberals win Monday’s election.

Klein further adds:

The total home equity held by Canadians is over $4.7 trillion. It’s the largest pool of private wealth in the country. For millions of Canadians — especially baby boomers — it’s the only retirement fund they have. They don’t have big pensions. They have a paid-off house and a hope that it will carry them through their later years. Yet, that’s what Ottawa has quietly been circling.

The Canadian Taxpayer’s Federation has researched this issue and published a report on the alarming amount of new taxation a homeowner equity tax could cost Canadians who sell their homes that have increased in value over the years they have lived in it. It is a shocker!

A Google search on the question, “what is a home equity tax?” returns the response:

A home equity tax, simply put, it’s a proposed levy on the increased value of your home, specifically, on your principal residence. The idea is for Government to raise money by taxing wealth accumulation from rising property values.

The Canadian Taxpayers Federation has provided a Home Equity Tax Calculator Backgrounder to help Canadians understand what the impact of three different types of Home Equity Tax Calculators would have on home owners. The required tax payment resulting from all three is a shocker.

Keep in mind that World Economic Forum policies intend to eventually eliminate all private home ownership and have the state own and control not only all residences, but also eliminate car ownership, and control when and where you may live and travel.

Carney, Trudeau and several other members of the Liberal government in key positions are heavily connected to the WEF.

Red Deer Justice Centre Grand Opening: Building access to justice for Albertans

Police Associations Endorse Conservatives. Poilievre Will Shut Down Tent Cities

Mark Carney Wants You to Forget He Clearly Opposes the Development and Export of Canada’s Natural Resources

Ottawa Confirms China interfering with 2025 federal election: Beijing Seeks to Block Joe Tay’s Election

Pope Francis has died aged 88

Former WEF insider accuses Mark Carney of using fear tactics to usher globalism into Canada

Canada’s press tries to turn the gender debate into a non-issue, pretend it’s not happening

-

Alberta2 days ago

Alberta2 days agoGovernments in Alberta should spur homebuilding amid population explosion

-

International2 days ago

International2 days agoHistory in the making? Trump, Zelensky hold meeting about Ukraine war in Vatican ahead of Francis’ funeral

-

Alberta2 days ago

Alberta2 days agoLow oil prices could have big consequences for Alberta’s finances

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoCarney’s budget is worse than Trudeau’s

-

Business2 days ago

Business2 days agoIt Took Trump To Get Canada Serious About Free Trade With Itself

-

C2C Journal2 days ago

C2C Journal2 days ago“Freedom of Expression Should Win Every Time”: In Conversation with Freedom Convoy Trial Lawyer Lawrence Greenspon

-

2025 Federal Election22 hours ago

Columnist warns Carney Liberals will consider a home equity tax on primary residences

-

Opinion1 day ago

Opinion1 day agoCanadians Must Turn Out in Historic Numbers—Following Taiwan’s Example to Defeat PRC Election Interference