Business

US firms like BlackRock are dropping their climate obsession while Europe ramps theirs up

Larry Fink on stage at the 2022 New York Times DealBook on November 30, 2022. in New York CityPhoto by Thos Robinson/Getty Images for The New York Times

From LifeSiteNews

By David James

As U.S. firms such as BlackRock and JPMorgan Chase continue to distance themselves from the ESG and ‘climate change’ agendas, Europe has been moving aggressively in the opposite direction, suggesting a rift is forming on the global economic landscape.

The climate change debate is usually thought to be focused on scientific analyses of the earth’s atmosphere. But that is only what is on the surface. It is also very much about money and politics and there has been a big shift that looks likely to threaten support for the net zero initiative. It may lead to a deep economic and political rift between the U.S. and Europe.

Estimates of the cost of decarbonizing the economy by 2050 have varied, but it is generally agreed that it is a financial bonanza. Goldman Sachs is at the low end with a modest $80 trillion while Bank of America estimates an extraordinary $275 trillion, about 10 times the current value of the U.S. stock market.

The finance sector, dizzy with the prospect of a huge investment opportunity, imposed a metric on corporations called Environmental, Social and Governance (ESG), a mechanism for demanding that companies go down the net zero route – and also comply with diversity equity and inclusion (DEI) requirements, the “S” part of ESG. Corporations that did not cooperate were threatened with a loss of support in the market and lower relative share prices.

That trend is starting to reverse. BlackRock, JPMorgan Chase, and State Street recently exited from Climate Action 100+, a coalition of the world’s largest institutional investors that pledges to “ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change.” The passive fund Vanguard, the world’s second largest, exited over a year ago.

These four fund managers oversee assets of about $25 trillion, which is approximately a quarter of the entire funds under management in the world.

They are changing direction for two reasons. First, there was an implicit bargain with ESG, whereby compliant companies would not only get to save the environment but also get to see their share prices outperform non-compliant companies. It is not turning out that way. In fact, better returns have come from investing against ESG-compliant companies.

More compellingly, 16 conservative state attorneys general in the U.S. have demanded answers from BlackRock’s directors regarding the Climate Action and ESG initiatives. Other fund managers and banks have also attracted unwanted scrutiny.

Nothing concentrates the mind of fund managers more than the prospect of clients withdrawing their funds – in this case state government pension money. Larry Fink, chief executive of BlackRock, is now saying he does not think it is helpful to use the term ESG, having been one of the most aggressive advocates. In his 2022 letter to CEOs he was issuing veiled threats to companies not complying with ESG. In 2024, he omitted the term entirely.

Meanwhile in Europe, very different choices are being made. The European Union (EU) is looking to impose sustainability reporting standards on all medium and large businesses. The intention is to have European companies set up a new accounting system by the end of the decade. Rather than recording financial transactions, it will instead aggregate data related to climate, pollution, especially carbon dioxide emissions, biodiversity and social issues.

As one (anonymous) analyst writes: “It is a very detailed control system for European companies where the European Commission can, in the future, dictate anything it wants – and punish for any violations any way it wants. Apart from the crazy regulatory load, this initiative can only be seen as a direct seizure of operational control of European companies, and thereby the European economy.”

So, while the U.S. looks to restore an unsteady version of capitalism, Europe is heading towards some kind of climate-driven socialism.

The EU plan seems to be to eventually direct their banks’ lending, which would radically undermine the region’s free-market system and establish something more like communist-style centralized control.

This does not mean U.S. governments and bureaucrats will stop pushing their climate agenda. A court case brought by the city of Honolulu, for example, is one of several attempts to bankrupt the American energy industry. But when the big institutional money changes direction then corporations and governments eventually follow.

The situation is further complicated by the emergence of the expanded BRICS alliance, which will soon represent a bigger proportion of the world economy than the G7. Saudi Arabia, Iran, United Arab Emirates, Ethiopia and Egypt will be added to the original group of Brazil, Russia, India, China and South Africa.

The BRICS nations will not allow the West’s climate change agenda to reshape their polities. Most of them are either sellers or heavy consumers of fossil fuels. Both India and China are increasing their use of coal, for instance, which makes Western attempts to reduce emissions largely pointless.

The promise that hundreds of trillions of investment opportunities would come from converting to net zero was always just a financial projection, mere speculation. The scale of transiting to a decarbonized economy would be so enormous it would inevitably become a logistical nightmare, if not an impossibility.

Energy expenditure represents about an eighth of the world’s GDP. Oil, natural gas and coal still provide 84 percent of the world’s energy, down just two per cent from 20 years ago. Production of renewable energy has increased but so has overall consumption. Oil powers 97 percent of all transportation.

Relying solely on renewable energy was never realistic and now that the financial dynamic is changing the prospects of achieving net zero have become even more remote. As the finance website ZeroHedge opines: “Both the DEI and ESG gravy trains on Wall Street are finally coming to an unceremonious end.” Financial markets continually get seduced by fads; the ESG agenda is starting to look like yet another example.

From LifeSiteNews

By Matt Lamb

They got rid of all the older children essentially and just had younger children who were too young to be diagnosed and they stratified that, stratified the data

The Centers for Disease Control and Prevention (CDC) found newborn babies who received the Hepatitis B vaccine had 1,135-percent higher autism rates than those who did not or received it later in life, Robert F. Kennedy Jr. told Tucker Carlson recently. However, the CDC practiced “trickery” in its studies on autism so as not to implicate vaccines, Kennedy said.

RFK Jr., who is the current Secretary of Health and Human Services, said the CDC buried the results by manipulating the data. Kennedy has pledged to find the causes of autism, with a particular focus on the role vaccines may play in the rise in rates in the past decades.

The Hepatitis B shot is required by nearly every state in the U.S. for children to attend school, day care, or both. The CDC recommends the jab for all babies at birth, regardless of whether their mother has Hep B, which is easily diagnosable and commonly spread through sexual activity, piercings, and tattoos.

“They kept the study secret and then they manipulated it through five different iterations to try to bury the link and we know how they did it – they got rid of all the older children essentially and just had younger children who were too young to be diagnosed and they stratified that, stratified the data,” Kennedy told Carlson for an episode of the commentator’s podcast. “And they did a lot of other tricks and all of those studies were the subject of those kind of that kind of trickery.”

But now, Kennedy said, the CDC will be conducting real and honest scientific research that follows the highest standards of evidence.

“We’re going to do real science,” Kennedy said. “We’re going to make the databases public for the first time.”

He said the CDC will be compiling records from variety of sources to allow researchers to do better studies on vaccines.

“We’re going to make this data available for independent scientists so everybody can look at it,” the HHS secretary said.

— Matt Lamb (@MattLamb22) July 1, 2025

Health and Human Services also said it has put out grant requests for scientists who want to study the issue further.

Kennedy reiterated that by September there will be some initial insights and further information will come within the next six months.

Carlson asked if the answers would “differ from status quo kind of thinking.”

“I think they will,” Kennedy said. He continued on to say that people “need to stop trusting the experts.”

“We were told at the beginning of COVID ‘don’t look at any data yourself, don’t do any investigation yourself, just trust the experts,”‘ he said.

In a democracy, Kennedy said, we have the “obligation” to “do our own research.”

“That’s the way it should be done,” Kennedy said.

He also reiterated that HHS will return to “gold standard science” and publish the results so everyone can review them.

From LifeSiteNews

By Robert Jones

The Tesla CEO warned that Trump’s $5 trillion plan erases DOGE’s cost-cutting gains, while threatening to unseat lawmakers who vote for it.

Elon Musk has reignited his feud with President Donald Trump by denouncing his “Big Beautiful Bill” in a string of social media posts, warning that it would add $5 trillion to the national debt.

“I’m sorry, but I just can’t stand it anymore. This massive, outrageous, pork-filled Congressional spending bill is a disgusting abomination. Shame on those who voted for it: you know you did wrong. You know it,” Musk exclaimed in an X post last month.

I’m sorry, but I just can’t stand it anymore.

This massive, outrageous, pork-filled Congressional spending bill is a disgusting abomination.

Shame on those who voted for it: you know you did wrong. You know it.

— Elon Musk (@elonmusk) June 3, 2025

Musk renewed his criticism Monday after weeks of public silence, shaming lawmakers who support it while vowing to unseat Republicans who vote for it.

“They’ll lose their primary next year if it is the last thing I do on this Earth,” he posted on X, while adding that they “should hang their heads in shame.”

Every member of Congress who campaigned on reducing government spending and then immediately voted for the biggest debt increase in history should hang their head in shame!

And they will lose their primary next year if it is the last thing I do on this Earth.

— Elon Musk (@elonmusk) June 30, 2025

The Tesla and SpaceX CEO also threatened to publish images branding those lawmakers as “liars.”

Trump responded on Truth Social by accusing Musk of hypocrisy. “He may get more subsidy than any human being in history,” the president wrote. “Without subsidies, Elon would probably have to close up shop and head back home to South Africa… BIG MONEY TO BE SAVED!!!”

( @realDonaldTrump – Truth Social Post )

( Donald J. Trump – Jul 01, 2025, 12:44 AM ET )Elon Musk knew, long before he so strongly Endorsed me for President, that I was strongly against the EV Mandate. It is ridiculous, and was always a major part of my campaign. Electric cars… pic.twitter.com/VPadoTBoEt

— Donald J. Trump 🇺🇸 TRUTH POSTS (@TruthTrumpPosts) July 1, 2025

Musk responded by saying that even subsidies to his own companies should be cut.

Before and after the 2024 presidential election, Musk spoke out about government subsidies, including ones for electric vehicles, stating that Tesla would benefit if they were eliminated.

This latest exchange marks a new escalation in the long-running and often unpredictable relationship between the two figures. Musk contributed more than $250 million to Trump’s reelection campaign and was later appointed to lead the Department of Government Efficiency (DOGE), which oversaw the termination of more than 120,000 federal employees.

Musk has argued that Trump’s new bill wipes out DOGE’s savings and reveals a deeper structural problem. “We live in a one-party country – the PORKY PIG PARTY!!” he wrote, arguing that the legislation should be knows as the “DEBT SLAVERY bill” before calling for a new political party “that actually cares about the people.”

It is obvious with the insane spending of this bill, which increases the debt ceiling by a record FIVE TRILLION DOLLARS that we live in a one-party country – the PORKY PIG PARTY!!

Time for a new political party that actually cares about the people.

— Elon Musk (@elonmusk) June 30, 2025

In June, Musk deleted several inflammatory posts about the president, including one claiming that Trump was implicated in the Jeffrey Epstein files. He later acknowledged some of his comments “went too far.” Trump, in response, said the apology was “very nice.”

With the bill still under Senate review, the dispute underscores growing pressure on Trump from fiscal hardliners and tech-aligned conservatives – some of whom helped deliver his return to power. Cracks in the coalition may spell longer term problems for the Make America Great Again movement.

The Quiet Invasion: How Transnational Crime and Chinese State Actors Infiltrated Vancouver and Eroded Canada’s Sovereignty

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

World Economic Forum Aims to Repair Relations with Schwab

-

Business6 hours ago

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

-

Alberta1 day ago

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

-

Crime19 hours ago

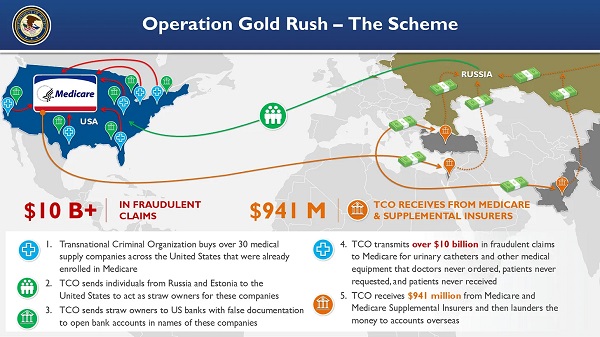

Crime19 hours agoNational Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Crime1 day ago

Crime1 day agoSuspected ambush leaves two firefighters dead in Idaho

-

Health19 hours ago

Health19 hours agoRFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

-

Alberta1 day ago

Alberta1 day agoWhy the West’s separatists could be just as big a threat as Quebec’s

-

Business1 day ago

Business1 day agoCanada Caves: Carney ditches digital services tax after criticism from Trump

-

Business1 day ago

Business1 day agoMassive government child-care plan wreaking havoc across Ontario