Business

The Strange Case of the Disappearing Public Accounts Report

A few days ago, Public Services and Procurement Canada tabled their audited consolidated financial statements of the Government of Canada for 2024. This is the official and complete report on the state of government finances. When I say “complete”, I mean the report’s half million words stretch across three volumes and total more than 1,300 pages.

Together, these volumes provide the most comprehensive and authoritative view of the federal government’s financial management and accountability for the fiscal year ending March 31, 2024. The tragedy is that no one has the time and energy needed to read and properly understand all that data. But the report identifies problems serious enough to deserve the attention of all Canadians – and especially policy makers.

The Audit is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Following the approach of my Parliamentary Briefings series, I uploaded all three volumes of the report to my AI research assistant and asked for its thoughts. Each one of the observations that came out the other end is significant and, in calmer and more rational times, could easily have driven a week’s worth of news coverage. But given the craziness of the past few weeks and months, they’re being largely ignored.

With that in mind, I’ve made this special edition of the Parliamentary Briefings series fully accessible to all subscribers.

We begin with a summary of the purpose and scope of the three uploaded volumes of the Public Accounts of Canada for 2023–2024:

Volume I: Summary Report and Consolidated Financial Statements

- Purpose: Provides a high-level overview of the federal government’s financial performance, presenting the consolidated financial statements audited by the Auditor General. It serves as the primary accountability report.

- Scope:

- Audited financial statements.

- Analysis of revenues, expenses, and the accumulated deficit.

- Overview of assets, liabilities, and financial position.

- Discussion of economic context, risks, uncertainties, and ten-year comparative financial data.

Volume II: Details of Expenses and Revenues

- Purpose: Presents the financial operations of the government, broken down by ministries and agencies, for detailed accountability.

- Scope:

- Financial transactions segregated by ministry.

- Details of appropriations, revenues, and transfer payments.

- Summary tables on ministerial expenditures by type, object, and other dimensions.

- Appendices providing additional details on budgetary authorities and their sources.

Volume III: Additional Information and Analyses

- Purpose: Offers supplementary analyses and financial data beyond what is included in the first two volumes, focusing on revolving funds, professional services, and shared-cost programs.

- Scope:

- Financial statements of revolving funds (e.g., Passport Canada, Canadian Grain Commission).

- Expenditure details on acquisitions, transfer payments, and public debt charges.

- Analyses of federal-provincial shared-cost programs and claims against the Crown.

- Miscellaneous financial and operational data for broader transparency.

The Audit: Based on these documents, could you identify the most serious threats to Canada’s economic stability?

From the Public Accounts of Canada 2023–2024, several serious threats to Canada’s economic security can be identified. These threats emerge from the broader fiscal and economic analyses, contingent liabilities, and uncertainties highlighted in the documents.

1. Growing Public Debt and Debt Servicing Costs

- Observation: Canada’s public debt charges increased significantly in 2024, rising by 35.2% year-over-year, largely due to higher interest rates on debt. The total accumulated federal debt stood at $1.24 trillion, representing 42.1% of GDP, up from 41.1% the previous year.

- Risk: Rising debt servicing costs reduce fiscal space for critical public investments, making the economy vulnerable to future economic shocks or downturns.

2. Contingent Liabilities and Indigenous Claims

- Observation: The government recorded $16.4 billion in contingent liabilities related to Indigenous claims in 2024, reflecting ongoing efforts to address past injustices. These liabilities have been increasing at an average annual growth rate of 30% since 2016.

- Risk: The unpredictable nature and scale of these liabilities could create significant financial pressures if settlements or court decisions require substantial payouts.

3. Legacy Costs from the COVID-19 Pandemic

- Observation: The government recorded $4.7 billion in pandemic-related expenses for 2024, including write-offs for expired vaccines and provisions for unrecovered loans and benefits.

- Risk: These costs highlight vulnerabilities in emergency financial planning and expose the government to further financial risks if similar large-scale public health crises occur.

4. Economic Pressures from High Inflation and Interest Rates

- Observation: Inflation returned to the Bank of Canada’s 2% target by mid-2024 after 41 consecutive months above this threshold. However, elevated interest rates (peaking at 5%) contributed to a softening economy.

- Risk: Prolonged periods of high interest rates could suppress household and business spending, slowing economic growth and increasing the likelihood of a recession.

5. Climate Change and Environmental Commitments

- Observation: Significant spending is allocated to addressing climate change, with over $1 billion dedicated to environmental programs in 2024, including pollution pricing proceeds and clean energy initiatives.

- Risk: Canada’s reliance on resource-intensive industries and increasing costs to meet climate targets create economic vulnerabilities, particularly in regions heavily reliant on fossil fuels.

6. Global Economic Instability

- Observation: Global supply chain disruptions, energy price volatility, and geopolitical events (e.g., Russia’s invasion of Ukraine) significantly impacted Canada’s economy, with slower GDP growth (1.5% in 2023) and reduced trade.

- Risk: External shocks could exacerbate domestic economic challenges, such as rising import costs or reduced demand for Canadian exports.

7. Labor Market and Productivity Challenges

- Observation: While job creation remained positive, population growth outpaced employment gains, leading to an increase in the unemployment rate to 6.5% by October 2024. Productivity improvements have been uneven.

- Risk: Labor shortages in key sectors and declining workforce participation among certain demographics (e.g., aging population) could undermine economic resilience.

8. Dependence on Resource Revenues

- Observation: Volatile global commodity prices impacted nominal GDP growth, with gains slowing to 2.9% in 2023 after double-digit growth in prior years.

- Risk: Fluctuations in resource revenues leave Canada exposed to external shocks, particularly in provinces like Alberta and Saskatchewan, heavily reliant on oil and gas.

These challenges underscore the need for proactive fiscal and policy measures to safeguard economic stability, manage liabilities, and address emerging risks.

The Audit: What would you recommend as the three most urgent areas to address to avoid deepening the economic crisis?

1. Manage Rising Public Debt and Debt Servicing Costs

- Why It’s Urgent: The rapid increase in public debt charges (35.2% in 2024) is crowding out fiscal space for essential programs. The federal debt, at 42.1% of GDP, has become a significant liability, with interest rate fluctuations posing an ongoing threat.

- Recommendations:

- Introduce stricter fiscal discipline by prioritizing expenditures that yield long-term economic benefits (e.g., infrastructure, innovation).

- Develop a comprehensive debt reduction strategy to stabilize the debt-to-GDP ratio in the medium term.

- Explore debt refinancing strategies to lock in lower interest rates where feasible.

- Impact: Reducing debt servicing pressures will free up resources for critical investments and improve Canada’s fiscal resilience.

2. Mitigate the Economic Impact of Contingent Liabilities

- Why It’s Urgent: Contingent liabilities related to Indigenous claims have grown exponentially (30% annually since 2016), creating fiscal unpredictability and potentially overwhelming future budgets.

- Recommendations:

- Accelerate settlement negotiations to limit litigation costs and interest on outstanding claims.

- Establish a transparent reserve fund specifically for contingent liabilities, ensuring predictable future payouts.

- Increase collaboration with Indigenous communities to address systemic issues and prevent further claims.

- Impact: Resolving liabilities promptly will reduce fiscal uncertainty and demonstrate Canada’s commitment to reconciliation.

3. Address Structural Labor Market and Productivity Challenges

- Why It’s Urgent: Despite job creation, rising unemployment (6.5% in late 2024) and productivity stagnation threaten long-term economic growth. Labor shortages in critical sectors further exacerbate vulnerabilities.

- Recommendations:

- Expand skilled immigration programs to address labor shortages in healthcare, technology, and green industries.

- Increase investment in workforce retraining programs, particularly for sectors undergoing automation or transition due to climate policies.

- Promote workplace flexibility and childcare access to increase labor force participation, particularly among women and aging workers.

- Impact: Enhancing workforce productivity and participation will strengthen the economic foundation and support GDP growth.

Rationale for Prioritization

These areas represent the most immediate threats to economic security and fiscal stability. Addressing them proactively can reduce vulnerabilities and position Canada for sustainable growth.

The Audit: What are the most surprising and disturbing details in these documents?

1. Rapid Growth of Public Debt Charges

- Detail: Public debt charges increased by 35.2% year-over-year to $47.3 billion, representing one of the fastest-growing expense categories. This reflects a combination of higher interest rates and the significant size of Canada’s debt.

- Why Disturbing: Such a rapid increase in debt servicing costs could divert funds from essential public services and programs. It also signals limited fiscal flexibility in the event of future economic shocks.

2. Ballooning Contingent Liabilities

- Detail: The federal government recorded $16.4 billion in expenses for Indigenous contingent liabilities in 2024. This is part of an ongoing surge, with liabilities increasing by 30% annually since 2016.

- Why Disturbing: While reconciliation efforts are vital, the sheer scale and rapid growth of these liabilities are fiscally unsustainable without structural changes or dedicated funding mechanisms. The risk of further liabilities emerging adds to fiscal uncertainty.

3. Significant Write-offs and Provisions for Pandemic Programs

- Detail: The government wrote off $1.2 billion in expired COVID-19 vaccines and therapeutics and recorded $3.5 billion in provisions for unrecovered pandemic-era loans.

- Why Disturbing: These figures highlight inefficiencies in planning and administration during the pandemic response, leading to substantial financial losses. The scale of unrecovered funds also raises questions about accountability in the deployment of emergency programs.

4. Rising Unemployment Despite Job Creation

- Detail: While 475,000 jobs were created in 2023, the unemployment rate rose to 6.5% by late 2024 due to population growth outpacing employment gains.

- Why Surprising: Despite strong job creation, an inability to keep pace with population growth signals structural issues in labor force integration. This poses a risk to Canada’s economic competitiveness and social cohesion.

5. Declining Corporate Income Tax Revenues

- Detail: Corporate income tax revenues decreased by 0.7%, driven by reduced taxable income despite an overall increase in total revenues.

- Why Surprising: The decline in corporate tax revenues during a period of economic recovery raises concerns about potential tax avoidance, economic inequality, or over-reliance on other revenue streams, such as personal income taxes.

6. Substantial Environmental and Climate Spending

- Detail: Over $1 billion was allocated to environmental programs, including pollution pricing proceeds. However, the documents note Canada’s slow progress toward net-zero targets and risks to resource-dependent provinces.

- Why Disturbing: While necessary, this spending may be insufficient given the scale of the climate challenge. The mismatch between spending and measurable progress on climate goals risks long-term environmental and economic consequences.

7. Unanticipated Costs of Indigenous Reconciliation

- Detail: Beyond contingent liabilities, the government is facing unpredictable settlement costs due to increasing litigation and the complexity of claims. These have already exceeded $60 billion since 2016.

- Why Disturbing: The ongoing financial impact of these settlements reflects Canada’s historical neglect of Indigenous issues. Resolving these claims is essential, but the lack of predictability or dedicated funding highlights systemic shortcomings in reconciliation strategies.

8. Softened GDP Growth and Inflation Challenges

- Detail: Real GDP growth slowed to 1.5% in 2023, and inflation remained high throughout the year, only reaching the Bank of Canada’s 2% target by mid-2024.

- Why Disturbing: The prolonged inflationary period and sluggish growth signal a fragile recovery. These economic conditions could exacerbate income inequality and lead to further fiscal strain.

9. High Provisions for Unrecovered Loans

- Detail: Provisions of $3.5 billion were recorded for emergency loans provided during the pandemic. The government continues to face difficulties in recovering these funds.

- Why Disturbing: This provision raises serious questions about the efficiency of loan administration and the government’s ability to safeguard public funds during emergencies.

10. Heavy Dependence on Volatile Resource Revenues

- Detail: Nominal GDP growth slowed to 2.9% in 2023, largely due to easing commodity prices after a surge in 2022. Resource dependence remains a key economic vulnerability.

- Why Surprising: Despite global shifts toward renewable energy, Canada’s reliance on resource revenues remains high, posing long-term risks to economic diversification and stability.

|

Invite your friends and earn rewards

2025 Federal Election

Poilievre will cancel Mark Carney’s new Liberal packaging law and scrap the Liberal plastic ban!

From Conservative Party Communications

Conservative Leader Pierre Poilievre promised today that a new Conservative government will stop Mark Carney’s proposed Liberal food tax and scrap the existing Liberal plastic ban. Poilievre will:

- Stop proposed new labelling and packaging requirements that will raise the cost of fresh produce by as much as 34% and cost the average Canadian household an additional $400 each year.

- Scrap the Liberal plastics ban, including the ban on straws, grocery bags, food containers and cutlery, and other single-use plastics, letting consumers and businesses choose what works for them.

- Protect restaurants, grocers, and low-income Canadians from one-size-fits-all packaging rules that disproportionately affect those who can least afford it.

“After the Lost Liberal Decade, many Canadians can barely afford to put food on the table. And now Mark Carney and the Liberals want to make it even harder with a new food packaging law that will raise the price of food–again,” said Poilievre. “A new Conservative government will keep food prices down by scrapping the Liberal plastic ban and stopping Carney’s new Liberal food tax.”

After a decade of out-of-control spending and massive tax increases, families are spending $800 more on food this year than they did in 2024, and food banks had to handle a record two million visits in a single month. In Montreal, 44 percent of CEGEP students are experiencing some form of food insecurity, while places like Hawkesbury, Kingston, Toronto and Mississauga have all declared food insecurity emergencies.

And food prices are still rocketing upwards, surging by 3.2% over the last year, with no end in sight. In the last month alone, food inflation increased by 1.9 percentage points—the largest monthly jump in food prices in decades.

As if this wasn’t bad enough, Liberals have made life even more expensive and inconvenient for Canadians by banning plastics – including everything from straws to bags to food packaging. The current Liberal ban on single-use plastics will cost Canadians $1.3 billion dollars over the next decade.

Now Mark Carney wants to make it worse by adding complicated and costly new food packaging rules that will drive up the price of food even more–in effect, a new Liberal food tax. Plastic food packaging makes up 1/3 of all plastic packaging in Canada. The proposed Liberal food tax will cost the average Canadian household an additional $400 each year, waste half a million tonnes of food, decrease access to imported fruit and produce, and increase food inflation. The Chemistry Industry Association of Canada has also warned that this tax will put up to 60,000 Canadians out of work.

“The Liberals’ ideological crusade against convenience has already driven up food prices and the last thing Canadians need is Mark Carney’s new food tax added directly to your grocery bill,” said Poilievre. “The choice for Canadians is clear, a fourth Liberal term that will make food even more expensive or a new Conservative government that will axe the food tax and bring back straws, grocery bags and other items, to make life more affordable and convenient for Canadians – For a Change.”

![]()

From the Daily Caller News Foundation

By Andi Shae Napier

Republican Texas Sen. Ted Cruz and Republican Ohio Rep. Jim Jordan are turning their attention to Google over concerns that the tech giant is censoring users and infringing on Americans’ free speech rights.

Google’s parent company Alphabet, which also owns YouTube, appears to be the GOP’s next Big Tech target. Lawmakers seem to be turning their attention to Alphabet after Mark Zuckerberg’s Meta ended its controversial fact-checking program in favor of a Community Notes system similar to the one used by Elon Musk’s X.

Cruz recently informed reporters of his and fellow senators’ plans to protect free speech.

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here. Thank you!

“Stopping online censorship is a major priority for the Commerce Committee,” Cruz said, as reported by Politico. “And we are going to utilize every point of leverage we have to protect free speech online.”

Following his meeting with Alphabet CEO Sundar Pichai last month, Cruz told the outlet, “Big Tech censorship was the single most important topic.”

Jordan, Chairman of the House Judiciary Committee, sent subpoenas to Alphabet and other tech giants such as Rumble, TikTok and Apple in February regarding “compliance with foreign censorship laws, regulations, judicial orders, or other government-initiated efforts” with the intent to discover how foreign governments, or the Biden administration, have limited Americans’ access to free speech.

“Throughout the previous Congress, the Committee expressed concern over YouTube’s censorship of conservatives and political speech,” Jordan wrote in a letter to Pichai in March. “To develop effective legislation, such as the possible enactment of new statutory limits on the executive branch’s ability to work with Big Tech to restrict the circulation of content and deplatform users, the Committee must first understand how and to what extent the executive branch coerced and colluded with companies and other intermediaries to censor speech.”

Jordan subpoenaed tech CEOs in 2023 as well, including Satya Nadella of Microsoft, Tim Cook of Apple and Pichai, among others.

Despite the recent action against the tech giant, the battle stretches back to President Donald Trump’s first administration. Cruz began his investigation of Google in 2019 when he questioned Karan Bhatia, the company’s Vice President for Government Affairs & Public Policy at the time, in a Senate Judiciary Committee hearing. Cruz brought forth a presentation suggesting tech companies, including Google, were straying from free speech and leaning towards censorship.

Even during Congress’ recess, pressure on Google continues to mount as a federal court ruled Thursday that Google’s ad-tech unit violates U.S. antitrust laws and creates an illegal monopoly. This marks the second antitrust ruling against the tech giant as a different court ruled in 2024 that Google abused its dominance of the online search market.

RCMP Whistleblowers Accuse Members of Mark Carney’s Inner Circle of Security Breaches and Surveillance

PPE Videos, CCP Letters Reveal Pandemic Coordination with Liberal Riding Boss and Former JCCC Leader—While Carney Denies Significant Meeting In Campaign

MEI-Ipsos poll: 56 per cent of Canadians support increasing access to non-governmental healthcare providers

AI-Driven Election Interference from China, Russia, and Iran Expected, Canadian Security Officials Warn

-

Daily Caller1 day ago

Daily Caller1 day agoTrump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid

-

2025 Federal Election1 day ago

2025 Federal Election1 day agoBREAKING from THE BUREAU: Pro-Beijing Group That Pushed Erin O’Toole’s Exit Warns Chinese Canadians to “Vote Carefully”

-

Business1 day ago

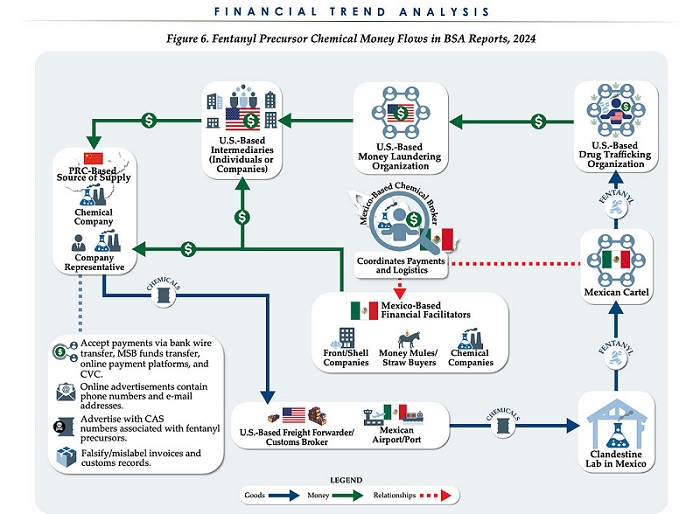

Business1 day agoChina, Mexico, Canada Flagged in $1.4 Billion Fentanyl Trade by U.S. Financial Watchdog

-

COVID-191 day ago

COVID-191 day agoTamara Lich and Chris Barber trial update: The Longest Mischief Trial of All Time continues..

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoTucker Carlson Interviews Maxime Bernier: Trump’s Tariffs, Mass Immigration, and the Oncoming Canadian Revolution

-

2025 Federal Election1 day ago

2025 Federal Election1 day agoAllegations of ethical misconduct by the Prime Minister and Government of Canada during the current federal election campaign

-

Energy1 day ago

Energy1 day agoStraits of Mackinac Tunnel for Line 5 Pipeline to get “accelerated review”: US Army Corps of Engineers

-

Business2 days ago

Business2 days agoDOGE Is Ending The ‘Eternal Life’ Of Government