Energy

Government policies diminish Alberta in eyes of investors

From the Fraser Institute

By Julio Mejía and Tegan Hill

Canada’s economy has stagnated, with a “mild to moderate” recession expected this year. Alberta can help Canada through this economic growth crisis by reaping the benefits of a strong commodity market. But for this to happen, the federal and provincial governments must eliminate damaging policies that make Alberta a less attractive place to invest.

Every year, the Fraser Institute surveys senior executives in the oil and gas industry to determine what jurisdictions in Canada and the United States are attractive—or unattractive—to investment based on policy factors. According to the latest results, red tape and high taxes are dampening the investment climate in the province’s energy sector.

Consider the difference between Alberta and two large U.S. energy jurisdictions—Wyoming and Texas. According to the survey, oil and gas investors are particularly wary of environmental regulations in Alberta with 50 per cent of survey respondents indicating that “stability, consistency and timeliness of environmental regulatory process” scared away investment compared to 14 per cent in Wyoming and only 11 per cent in Texas.

Investors also suggest that the U.S. regulatory environment offers greater certainty and predictability compared to Alberta. For example, 42 per cent of respondents indicated that “uncertainty regarding the administration, interpretation, stability, or enforcement of existing regulations” is a deterrent to investment in Alberta, compared to only 9 per cent in Wyoming and 13 per cent in Texas. Similarly, 43 per cent of respondents indicated that the cost of regulatory compliance was a deterrent to investment in Alberta compared to just 9 per cent for Wyoming and 19 per cent for Texas.

And there’s more—41 per cent of respondents for Alberta indicated that taxation deters investment compared to only 21 per cent for Wyoming and 14 per cent for Texas. Overall, Wyoming was more attractive than Alberta in 14 out of 16 policy factors assessed by the survey and Texas was more attractive in 11 out of 16.

Indeed, Canadian provinces are generally less attractive for oil and gas investment compared to U.S. states. This should come as no surprise—Trudeau government policies have created Canada’s poor investment climate. Consider federal Bill C-69, which imposes complex, uncertain and onerous review requirements on major energy projects. While this bill was declared unconstitutional, uncertainty remains until new legislation is introduced. During the COP28 conference in Dubai last December, the Trudeau government also announced its draft framework to cap oil and gas sector greenhouse gas emissions, adding uncertainty for investors due to the lack of details. These are just a few of the major regulations imposed on the energy industry in recent years.

As a result of these uncertain and onerous regulations, the energy sector has struggled to complete projects and reach markets overseas. Not surprisingly, capital investment in Alberta’s oil and gas sector plummeted from $58.1 billion (in 2014) to $26.0 billion in 2023.

The oil and gas sector is one of the country’s largest industries with a major influence on economic growth. Alberta can play a key role in helping Canada overcome the current economic challenges but the federal and provincial governments must pay attention to investor concerns and establish a more competitive regulatory and fiscal environment to facilitate investment in the province’s energy sector—for the benefit of all Canadians.

Authors:

Energy

Straits of Mackinac Tunnel for Line 5 Pipeline to get “accelerated review”: US Army Corps of Engineers

![]()

From the Daily Caller News Foundation

By Audrey Streb

The Army Corps of Engineers on Tuesday announced an accelerated review of a Michigan pipeline tunnel under the Straits of Mackinac following President Donald Trump’s declaration of a “national energy emergency” on day one of his second term.

Enbridge’s Line 5 oil pipeline is among 600 projects to receive an emergency designation following Trump’s January executive order declaring a national energy emergency and expediting reviews of pending energy projects. The action instructed the Army Corps to use emergency authority under the Clean Water Act to speed up pipeline construction.

“An energy supply situation which would result in an unacceptable hazard to life, a significant loss of property, or an immediate, unforeseen, and significant economic hardship,” if not acted upon quickly, the public notice reads.

U.S. President Donald Trump holds up a signed executive order as (L-R) U.S. Treasury Secretary Scott Bessent, Secretary of Commerce Howard Lutnick and Interior Secretary Doug Burgum look on in the Oval Office of the White House on April 09, 2025 in Washington, DC. (Photo by Anna Moneymaker/Getty Images)

“Line 5 is critical energy infrastructure,” Calgary-based Enbridge wrote to the DCNF. The company noted that it submitted its permit applications to state and federal regulators five years ago and described the project as “designed to make a safe pipeline safer while also ensuring the continued safe, secure, and affordable delivery of essential energy to the Great Lakes region.”

Army Corps’ Detroit District did not respond to the DCNF’s request for a copy of the notice or for comment.

The pipeline has been active since 1953 and extends for 645 miles across the state of Michigan, according to the Department of Environment, Great Lakes, and Energy website. Line 5 supplies 65% of the propane needs in Michigan’s Upper Peninsula and 55% of the state’s overall propane demand, according to Enbridge.

The project has faced legal trouble and permitting delays that have hindered its expansion. Michigan Democratic Gov. Gretchen Whitmer in 2019 used a legal opinion by Attorney General Dana Nessel to argue that the law that created the authority to approve the project “because its provisions go beyond the scope of what was disclosed in its title.”

The State of Michigan greenlit the project in 2021 and the Michigan Public Service Commission approved placing the new pipeline segment in 2023.

Trump has championed an American energy production revival, stating throughout his 2024 campaign that he wanted to “drill, baby, drill,” in reference to oil drilling on U.S. soil.

Daily Caller

Trump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid

![]()

From the Daily Caller News Foundation

By

President Trump signed several executive orders Tuesday that will allow coal-fired power plants to stay online past planned retirement dates, identify coal resources on federal lands, and bolster the reliability of the electric grid. The orders may help the U.S. face an uncomfortable truth: wind turbines and solar panels can’t cost-effectively meet the U.S.’ growing electricity needs.

Coal provides an important source of the reliable and fuel-secure energy needed to keep the lights on. Our organization’s research shows that it is more affordable than wind and solar, too.

Mr. Trump’s executive orders will allow coal operators the flexibility to delay the premature closures caused in part by President Biden’s policies. A May 2024 rule from the Biden Environmental Protection Agency would have forced coal plants to spend billions on unproven technology to capture 90% of their carbon dioxide emissions. If coal plants failed to comply by 2035, they would be forced to shutter by 2039. The Trump EPA has since announced it will reconsider this rule, but the process could take years.

Coal should be allowed to help keep the lights on, especially because U.S. electricity demand is rising. The North American Electric Reliability Council’s 2024 long-term reliability assessment warns that “resource additions are not keeping up with generator retirements and demand growth” in most regions of the U.S. Coal produced 16% of the U.S.’ electricity in 2023, and coal, natural gas and petroleum together produced 60%. Nuclear comprised another 18%. It is folly to believe that the U.S. can meet its growing power demands while kneecapping a significant source of its baseload power.

Not only is reliable baseload power a must for the grid, but electricity generated by coal is less expensive than intermittent resources like wind and solar. It’s easy to understand why: the cheapest source of electricity is from plants that have already been built. Most of the U.S.’ coal fleet is like houses where the mortgages have been paid off. With no loans or interest left to repay, operating costs for existing coal plants typically consist of property taxes, insurance, labor, maintenance, and fuel.

Our organization models the full costs of building enough wind, solar, and battery storage to replace coal, natural gas, and nuclear plants. Powering a grid on wind, solar, and batteries is more expensive than coal because connecting wind turbines and solar panels to the grid entails system-wide costs like constructing new transmission lines. The intermittency of wind and solar means you need more power plant capacity to generate the same amount of power. More power plant infrastructure means more property taxes. More weather-dependent resources means more costs to managing the grid, like turning off wind turbines and solar panels when they are producing too much electricity for the grid to absorb — or conversely, ramping up natural gas generation on cloudy and still days when wind and solar aren’t producing.

Our research incorporates system-wide costs and shows that a realistic midpoint estimate for wind turbines is $72 per MWh. Electricity from new solar can range between $50 per MWh to $85 per MWh. Data from the Federal Energy Regulatory Commission shows that the average coal plant generated electricity for only $34 per megawatt-hour (MWh) in 2020 (the last year of available data). It could be even less expensive for coal plants to generate electricity if states and utilities allowed coal plants to operate more often. In 2024, the coal fleet generated electricity only about 43% of the time. If that approached 80%, costs could go as low as $29.

Keeping America’s “beautiful, clean coal” plants online is the right thing for the country and it is good news for consumers that the U.S. has recognized the electric grid’s reliability hole and decided to stop digging.

Isaac Orr is vice president of research, and Mitch Rolling is the director of research at Always On Energy Research, a nonprofit energy modeling firm.

Mark Carney To Ban Free Speech if Elected

Mark Carney Vows Internet Speech Crackdown if Elected

RCMP Whistleblowers Accuse Members of Mark Carney’s Inner Circle of Security Breaches and Surveillance

MEI-Ipsos poll: 56 per cent of Canadians support increasing access to non-governmental healthcare providers

-

2025 Federal Election2 days ago

RCMP Whistleblowers Accuse Members of Mark Carney’s Inner Circle of Security Breaches and Surveillance

-

2025 Federal Election2 days ago

MEI-Ipsos poll: 56 per cent of Canadians support increasing access to non-governmental healthcare providers

-

Health2 days ago

Health2 days agoTrump admin directs NIH to study ‘regret and detransition’ after chemical, surgical gender transitioning

-

Daily Caller12 hours ago

Trump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid

-

Business14 hours ago

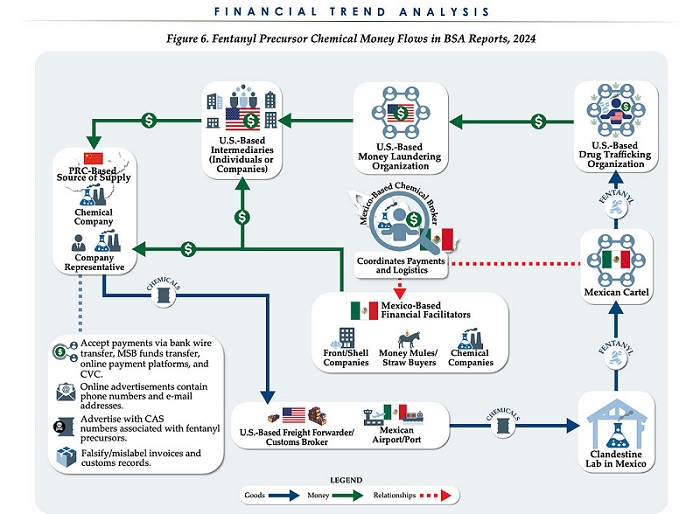

Business14 hours agoChina, Mexico, Canada Flagged in $1.4 Billion Fentanyl Trade by U.S. Financial Watchdog

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoBureau Exclusive: Chinese Election Interference Network Tied to Senate Breach Investigation

-

2025 Federal Election23 hours ago

2025 Federal Election23 hours agoTucker Carlson Interviews Maxime Bernier: Trump’s Tariffs, Mass Immigration, and the Oncoming Canadian Revolution

-

Autism2 days ago

Autism2 days agoAutism Rates Reach Unprecedented Highs: 1 in 12 Boys at Age 4 in California, 1 in 31 Nationally