Fraser Institute

Endless spending increases will not fix Canada’s health-care system

From the Fraser Institute

By Mackenzie Moir and Jake Fuss

Canada’s health-care system ranked as the most expensive (as a share of the economy) among 30 universal health-care countries. And despite these relatively high levels of spending, Canada continues to lag behind its peers on key indicators of performance.

In February 2023, the federal government announced the money they send to the provinces for health care would increase, yet again. Despite being billed as a fix for health care, these spending increases will not actually provide any relief for Canadian patients.

The Canada Health Transfer (CHT), the main federal financial tool for funding provincial health care, has increased from $34.0 billion in 2015/16 to $52.1 billion this year (2024/25), a 53.1 per cent increase in about a decade. Moreover, the federal government has committed to increases in the transfer at a guaranteed 5 per cent until 2027/28.

This latest increase in the CHT, however, is only one part of the $46.2 billion in new money being doled out over the next 10 years. More than half (roughly $25 billion) is currently being given to provinces who’ve signed up to work towards a number of “shared priorities” with Ottawa, such as mental health and substance abuse.

Clearly, the federal government has decided to substantially increase health-care spending in more than one way. But will it produce results?

These periodic “fixes” occasionally championed by Ottawa every few years are nothing new. And unfortunately, the data show that longstanding problems, including long waits for medical care and doctor shortages, will persist even though Canada is certainly no slouch when compared to its peers on health-care spending.

A recent study found that, when adjusted for differences in age (because older populations tend to spend more on health care), Canada’s health-care system ranked as the most expensive (as a share of the economy) among 30 universal health-care countries. And despite these relatively high levels of spending, Canada continues to lag behind its peers on key indicators of performance.

For example, Canada had some of the fewest physicians (ranked 28th of 30 countries), hospital beds (ranked 23rd of 29) and diagnostic technology such as MRIs (ranking 25th of 29 countries) and CT scanners (ranking 26th out of 30 countries) compared to other high-income countries with universal health care.

It also ranked at or near the bottom on measures such as same-day medical appointments, how easy it is to find afterhours care, and the timeliness of specialist appointments and surgical care.

And wait times have been getting worse. Just last year Canada recorded the longest ever delay for non-emergency care at 27.7 weeks, a 198 per cent increase from the 9.3 week wait experienced in 1993 (the first year national estimates were published).

But it’s not just the health-care system that’s in shambles, despite our high spending. Our federal finances are, too. Years of substantial increases in federal spending have strained the country’s finances. The Trudeau government’s latest budget projects a deficit of $39.8 billion this year, with more spent on debt interest ($54.1 billion) than on what the federal government gives to the provinces for health care.

Again, these periodic injections of federal funds to the provinces to supposedly fix health care are nothing new. Ottawa has relied on this strategy in the past and wait times have grown longer over the last three decades. Endless increases in spending will not fix our health-care system.

Authors:

2025 Federal Election

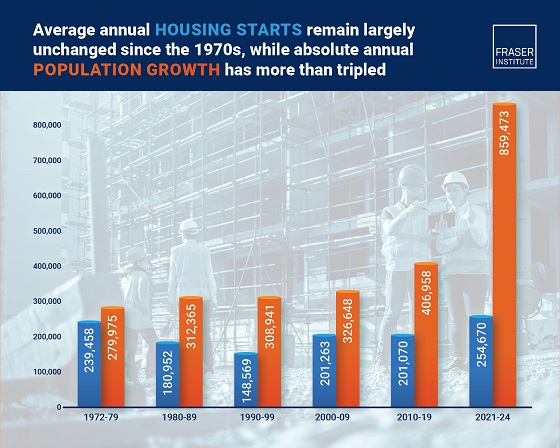

Housing starts unchanged since 1970s, while Canadian population growth has more than tripled

From the Fraser Institute

By: Austin Thompson and Steven Globerman

The annual number of new homes being built in Canada in recent years is virtually the same as it was in the 1970s, despite annual population growth

now being three times higher, finds a new study published today by the Fraser Institute, an independent, non-partisan Canadian public policy think tank.

“Despite unprecedented levels of immigration-driven population growth following the COVID-19 pandemic, Canada has failed to ramp up homebuilding sufficiently to meet housing demand,” said Steven Globerman, Fraser Institute senior fellow and co-author of The Crisis in Housing Affordability: Population Growth and Housing Starts 1972–2024.

Between 2021 and 2024, Canada’s population grew by an average of 859,473 people per year, while only 254,670 new housing units were started annually. From 1972 to 1979, a similar number of new housing units were built—239,458—despite the population only growing by 279,975 people a year.

As a result, more new residents are competing for each new home than in the past, which is driving up housing costs.

“The evidence is clear—population growth has been outpacing housing construction for decades, with predictable results,” Globerman said.

“Unless there is a substantial acceleration in homebuilding, a slowdown in population growth, or both, Canada’s housing affordability crisis is unlikely to improve.”

The Crisis in Housing Affordability: Population Growth and Housing Starts 1972–2024

- Canada experienced unprecedented population growth following the COVID-19 pandemic without a commensurately large increase in new homebuilding.

- The imbalance between population growth and new housing construction is reflected in a significant gap between housing demand and supply, which is driving up housing costs.

- Canada’s population grew by a record 1.23 million new residents in 2023 almost entirely due to immigration. That growth was more than double the pre-pandemic record set in 2019.

- Population growth slowed to 951,517 in 2024, still well above any year before 2023.

- Nationally, construction began on about 245,367 new housing units in 2024, down from a recent high of 271,198 starts in 2021—Canada’s annual number of housing starts peaked at 273,203 in 1976.

- Canada’s annual number of housing starts regularly exceeded 200,000 in past decades, when absolute population growth was much lower.

- In 2023, Canada added 5.1 new residents for every housing unit started, which was the highest ratio over the study’s timeframe and well above the average rate of 1.9 residents for every unit started observed over the study period (1972–2024).

- This ratio improved modestly in 2024, with 3.9 new residents added per housing start. However, the ratio remains far higher than at any point prior to the COVID-19 pandemic.

- These national trends are broadly mirrored across all 10 provinces, where annual population growth relative to housing starts is, to varying degrees, elevated when compared to long-run averages.

- Without an acceleration in homebuilding, a slowdown in population growth, or both, Canada’s housing affordability crisis will likely persist.

Austin Thompson

Steven Globerman

Senior Fellow and Addington Chair in Measurement, Fraser Institute

From the Fraser Institute

In 2019 Toronto District School Board (TDSB) trustees passed a “climate emergency” resolution and promised to develop a climate action plan. Not only does the TDSB now have an entire department in their central office focused on this goal, but it also publishes an annual climate action report.

Imagine you were to ask a random group of Canadian parents to describe the primary mission of schools. Most parents would say something along the lines of ensuring that all students learn basic academic skills such as reading, writing and mathematics.

Fewer parents are likely to say that schools should focus on reducing their environmental footprints, push students to engage in environmental activism, or lobby for Canada to meet the 2016 Paris Agreement’s emission-reduction targets.

And yet, plenty of school boards across Canada are doing exactly that. For example, the Seven Oaks School Division in Winnipeg is currently conducting a comprehensive audit of its environmental footprint and intends to develop a climate action plan to reduce its footprint. Not only does Seven Oaks have a senior administrator assigned to this responsibility, but each of its 28 schools has a designated climate action leader.

Other school boards have gone even further. In 2019 Toronto District School Board (TDSB) trustees passed a “climate emergency” resolution and promised to develop a climate action plan. Not only does the TDSB now have an entire department in their central office focused on this goal, but it also publishes an annual climate action report. The most recent report is 58 pages long and covers everything from promoting electric school buses to encouraging schools to gain EcoSchools certification.

Not to be outdone, the Vancouver School District (VSD) recently published its Environmental Sustainability Plan, which highlights the many green initiatives in its schools. This plan states that the VSD should be the “greenest, most sustainable school district in North America.”

Some trustees want to go even further. Earlier this year, the British Columbia School Trustees Association released its Climate Action Working Group report that calls on all B.C. school districts to “prioritize climate change mitigation and adopt sustainable, impactful strategies.” It also says that taking climate action must be a “core part” of school board governance in every one of these districts.

Apparently, many trustees and school board administrators think that engaging in climate action is more important than providing students with a solid academic education. This is an unfortunate example of misplaced priorities.

There’s an old saying that when everything is a priority, nothing is a priority. Organizations have finite resources and can only do a limited number of things. When schools focus on carbon footprint audits, climate action plans and EcoSchools certification, they invariably spend less time on the nuts and bolts of academic instruction.

This might be less of a concern if the academic basics were already understood by students. But they aren’t. According to the most recent data from the Programme for International Student Assessment (PISA), the math skills of Ontario students declined by the equivalent of nearly two grade levels over the last 20 years while reading skills went down by about half a grade level. The downward trajectory was even sharper in B.C., with a more than two grade level decline in math skills and a full grade level decline in reading skills.

If any school board wants to declare an emergency, it should declare an academic emergency and then take concrete steps to rectify it. The core mandate of school boards must be the education of their students.

For starters, school boards should promote instructional methods that improve student academic achievement. This includes using phonics to teach reading, requiring all students to memorize basic math facts such as the times table, and encouraging teachers to immerse students in a knowledge-rich learning environment.

School boards should also crack down on student violence and enforce strict behaviour codes. Instead of kicking police officers out of schools for ideological reasons, school boards should establish productive partnerships with the police. No significant learning will take place in a school where students and teachers are unsafe.

Obviously, there’s nothing wrong with school boards ensuring that their buildings are energy efficient or teachers encouraging students to take care of the environment. The problem arises when trustees, administrators and teachers lose sight of their primary mission. In the end, schools should focus on academics, not environmental activism.

Michael Zwaagstra

Senior Fellow, Fraser Institute

RCMP Whistleblowers Accuse Members of Mark Carney’s Inner Circle of Security Breaches and Surveillance

MEI-Ipsos poll: 56 per cent of Canadians support increasing access to non-governmental healthcare providers

AI-Driven Election Interference from China, Russia, and Iran Expected, Canadian Security Officials Warn

Trump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid

-

Daily Caller2 days ago

Trump Executive Orders ensure ‘Beautiful Clean’ Affordable Coal will continue to bolster US energy grid

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoBREAKING from THE BUREAU: Pro-Beijing Group That Pushed Erin O’Toole’s Exit Warns Chinese Canadians to “Vote Carefully”

-

Business2 days ago

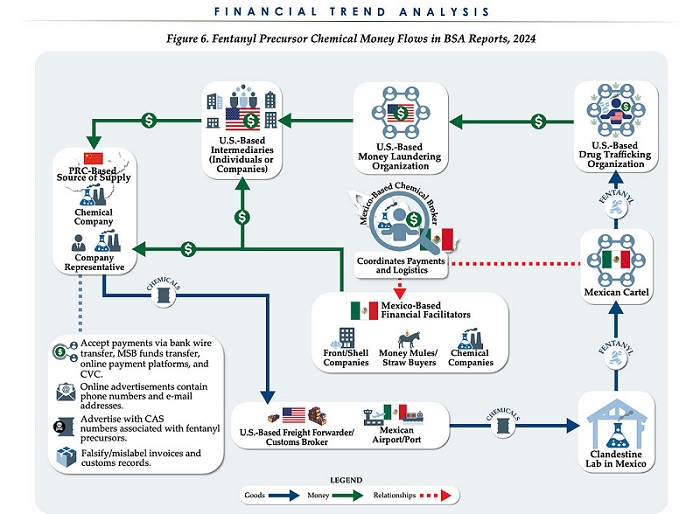

Business2 days agoChina, Mexico, Canada Flagged in $1.4 Billion Fentanyl Trade by U.S. Financial Watchdog

-

COVID-192 days ago

COVID-192 days agoTamara Lich and Chris Barber trial update: The Longest Mischief Trial of All Time continues..

-

2025 Federal Election18 hours ago

2025 Federal Election18 hours agoPRC-Linked Disinformation Claims Conservatives Threaten Chinese Diaspora Interests, Take Aim at PM Carney’s Debate Remark

-

Energy2 days ago

Energy2 days agoStraits of Mackinac Tunnel for Line 5 Pipeline to get “accelerated review”: US Army Corps of Engineers

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoAllegations of ethical misconduct by the Prime Minister and Government of Canada during the current federal election campaign

-

Daily Caller2 days ago

Daily Caller2 days agoDOJ Releases Dossier Of Deported Maryland Man’s Alleged MS-13 Gang Ties