Elon Musk’s social media platform, X, is now clear to resume its online activities in Brazil with the settlement of one final penalty according to an announcement made last Friday by Brazil’s controversial justice official, Alexandre de Moraes. The supreme justice authority in the country, known as the Federal Supreme Court (STF), had previously sanctioned a nationwide suspension of X in late August, a decree that was sustained by a judicial panel on September 2 following X’s noncompliance with the court’s orders.

The controversy originated in the spring when STF’s Minister de Moraes initiated an investigation into Musk and X after the platform refused to heed its censorship demands.

Musk was bold in his defiance of the court’s requests to shut down selected accounts in Brazil. He proceeded to critique de Moraes publicly, labeling him a “criminal” and advocating for the cessation of US foreign aid to Brazil.

Nonetheless, this incident marks a turning point in the ordeal. Earlier this month, X submitted official documentation to Brazil’s supreme court indicating their compliance with the court’s instructions, a stance diverging from their previous rebellious approach.

However, as reported by Brazil’s G1 Globo, X still holds the responsibility of settling a new fine of 10 million reals (approximately $2 million) to close the chapter on two further days of noncompliance with court orders. Rachel de Oliveira, X’s legal representative in Brazil, is also obligated to settle a 300,000 real penalty.

The situation escalated in mid-August, when Musk opted to shutter X’s Brazilian offices, thereby leaving the company devoid of a mandated legal representative in the country for its continued operations. As a consequence, the absence of this representation led the STF to initiate restrictions on the organization’s business assets within Brazil, affecting both X and Musk’s additional venture, Starlink.

Influential individuals in Brazil, such as former President Jair Bolsonaro, have been heavily critical of STF’s measures to clamp down on online so-called “hate speech” and “misinformation.” Musk himself has called for retribution against President Luiz Inácio “Lula” da Silv and Moraes, the latter of whom was a staunch advocate of these federal regulations.

Todayville is a digital media and technology company. We profile unique stories and events in our community. Register and promote your community event for free.

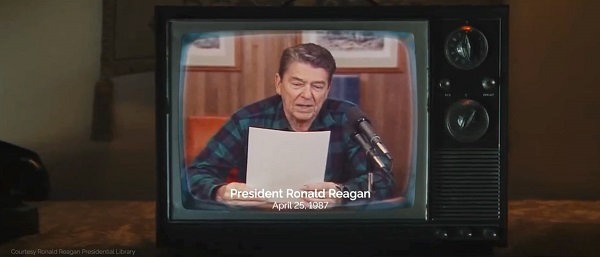

President Donald Trump announced late Thursday that trade negotiations with Canada “ARE HEREBY TERMINATED” after what he called “egregious behavior” tied to an Ontario TV ad that used former President Ronald Reagan’s voice to criticize tariffs.

The ad at the center of the feud was funded by Ontario Premier Doug Ford’s government as part of a multimillion-dollar campaign running on major U.S. networks. The spot features Reagan warning that tariffs may appear patriotic but ultimately “hurt every American worker and consumer.”

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

“They only did this to interfere with the decision of the U.S. Supreme Court, and other courts. TARIFFS ARE VERY IMPORTANT TO THE NATIONAL SECURITY, AND ECONOMY, OF THE U.S.A,” Trump wrote on his Truth Social platform late Thursday. “Based on their egregious behavior, ALL TRADE NEGOTIATIONS WITH CANADA ARE HEREBY TERMINATED.”

Ford first posted the ad online on Oct. 16, writing in a caption, “Using every tool we have, we’ll never stop making the case against American tariffs on Canada. The way to prosperity is by working together.”

The Ronald Reagan Presidential Foundation and Institute criticized the ad Thursday evening, saying it “misrepresents” Reagan’s 1987 radio address on free and fair trade. The foundation said Ontario did not request permission to use or alter the recording and that it is reviewing its legal options.

The president posted early Friday that Canada “cheated and got caught,” adding that Reagan actually “loved tariffs for our country.”

The ad splices audio from Reagan’s original remarks but includes his authentic statement: “When someone says, ‘let’s impose tariffs on foreign imports’, it looks like they’re doing the patriotic thing by protecting American products and jobs. And sometimes, for a short while it works, but only for a short time.”

Reagan also noted at the end of his remarks that, in “certain select cases,” he had taken steps to stop unfair trade practices against American products and added that the president’s “options” in trade matters should not be restricted, which the ad did not include.

Since returning to the White House, Trump has imposed tariffs on Canadian aluminum, steel, automobiles and lumber, arguing they are vital to protecting U.S. manufacturing and national security.

The Supreme Court is set to hear arguments in November over whether the administration overstepped its authority by invoking the International Emergency Economic Powers Act to impose reciprocal tariffs on dozens of nations, including Canada. Tariffs on commodities such as steel, aluminum and copper were implemented under Section 232 of the Trade Expansion Act and are not currently being challenged, as they align with longstanding precedent established by prior administrations.

Thursday’s move marks the second time this year Trump has canceled trade talks with Ottawa. In June, he briefly halted discussions after Canada imposed a digital services tax on American tech firms, though the Canadian government repealed the measure two days later.

Employees at Paccar’s Sainte-Thérèse, Quebec plant were informed Wednesday that the company will move production of trucks destined for the U.S. market back to its American facilities. According to Daniel Cloutier, Quebec director for Unifor, approximately 300 jobs will be eliminated, leaving roughly 500 workers at the plant.

Honking for Freedom Substack is a reader-supported publication.

To receive new posts and support my work, consider becoming a free or paid subscriber.

“They will continue building trucks for the Canadian market,” Cloutier said, noting that domestic demand represents a much smaller portion of output. At its peak, the plant produced 96 trucks per day; production will now drop to just 18 units daily. That is an 81% drop.

Paccar declined to confirm the restructuring or provide additional details. However, in a financial earnings call a day earlier, CEO Preston Feight described the U.S. tariff policy as advantageous for the company. “I think it helps Paccar significantly,” Feight said. “It gives us a competitive leg up from where we’ve been.”

U.S. Tariffs Driving Industry Shift

U.S. President Donald Trump has confirmed that all medium and heavy-duty trucks imported into the United States will face a 25-per-cent tariff beginning Nov. 1, along with an additional 10-per-cent duty on buses. The tariffs are being imposed under Section 232 of the Trade Expansion Act, which targets imports deemed to pose a national security risk.

These measures follow earlier tariffs that have already struck Canadian steel, aluminum, automobiles, copper, and lumber, forcing companies to shelve investments and reconsider their North American strategies.

Broader Auto Sector Retrenchment

Other automakers are also pulling back production in Canada. General Motors announced Tuesday it is ending production of the Chevrolet BrightDrop electric delivery van in Ingersoll, Ontario, costing over 1,100 workers their jobs. Stellantis recently confirmed plans to shift production of the Jeep Compass from Brampton, Ontario, to Belvidere, Illinois, as part of a strategy to increase U.S. output by 50 per cent by 2029.

Quebec Plant at Risk

The Sainte-Thérèse plant, which manufactures Class 5, 6 and 7 Kenworth and Peterbilt trucks, has already endured two rounds of layoffs over the past year as uncertainty around tariffs weakened demand. At peak production, the facility employed over 1,400 people.

Cloutier said the union is pressing both the Quebec and federal governments to prioritize the purchase of domestically made vehicles to sustain production levels. Without such measures, he warned, the plant could be forced to close due to high fixed costs and insufficient volume. “Let’s not pretend global trade hasn’t changed with this President,” Cloutier said. “We need to stop twiddling our thumbs.”

Bus Manufacturers Also Exposed

Quebec is also home to two major bus manufacturers, Prevost and Nova Bus, both owned by Volvo Group that could face similar challenges due to new tariffs on buses entering the U.S. Executives at both companies say they are still assessing the impact of the policy shift.

What can we learn from all this?

Perhaps our deep reliance on American innovation has consequences we have been unwilling to confront. The warning signs were evident well before Donald Trump’s election. He was explicit that tariffs would be used as a strategic tool to financially incentivize American companies to return to the United States. This was not hidden, it was a core pillar of his economic agenda.

I have said repeatedly on the Marc Patrone Show on Sauga 960 that my frustration is not with America’s strategy, but with Canada’s political class. Their smug arrogance lies in the belief that, as great as Canada can be, we could somehow dominate the greatest economy in the history of civilization rather than work with it. The Trump administration never wanted Canada to become the 51st state; they want our valuable resources and are willing to pay fair value for them, and they expect Canada to finally take our internal security threats seriously; something I have personally presented on in the United States. Yet instead of leveraging our strategic position, Canada’s leadership chose performative resistance over pragmatic partnership.

The most telling moment came when President Trump reportedly asked Justin Trudeau what would happen if the United States imposed a 25-per-cent tariff on all Canadian goods. Trudeau’s response, “It would destroy Canada” was an example of catastrophic stupidity. It handed Trump the gun he could use to execute Canada economically and perhaps cost Canada its sovereignty over the long term.

Reminiscent of the scene from The Hunt for Red October, when Captain Tupolev, in an act of smug Laurentian style arrogance, fires a torpedo at Ramius only for it to circle back and destroy his own submarine, a catastrophic miscalculation born of arrogance and a complete misunderstanding of the enemy’s capabilities. A catastrophic miscalculation that mirrors Elbows Up stupidity.