Business

Big Tech’s Sudden Rush Into Nuclear Is A Win-Win For America

![]()

From the Daily Caller News Foundation

By David Blackmon

The U.S. power-generation sector has been hit in recent weeks with story after story about Big Tech firms entering into deals with power providers or developers to satisfy their electricity needs with nuclear generation.

Here are some examples:

—In mid-October, Google said it had entered into an agreement to purchase power for its data center needs from Kairos Power, a developer of small modular reactors (SMRs).

—A couple of weeks earlier, Microsoft and Constellation completed a deal that would involve the restart of Unit 1 at the Three Mile Island facility in Pennsylvania to power that company’s needs.

—On Dec. 3, Meta issued a request for proposals to nuclear developers to provide up to 4 gigawatts (GW) of electricity to power data centers and AI no later than the early 2030s.

—Perhaps the most extensive development of all came two days after Google’s announcement, when Amazon announced it has entered into deals to support the development of Small Modular Reactors (SMRs) with three developers in three different regions of the country.

So, what’s going on here? Aren’t all these Big Tech companies supposed to be totally bought into the climate-alarm narrative, a narrative that claims wind and solar are the only real “clean” energy solutions for power generation? Aren’t we constantly bombarded by boosters of those non-solutions that they are able to reliably provide uninterrupted electricity if backed up by stationary batteries?

Certainly, that has been the case in the past — few corporations could hope to match the volume of virtue signaling about green energy we have seen from these tech companies in recent years. That was all fine until, apparently, the AI revolution came along.

AI is an enormous power hog, one that these and other Big Tech firms must now rapidly adopt to remain competitive.

The trouble with AI and the data centers needed to make it go is that it requires the reliable, constant injection of electricity 24 hours a day, 7 days a week, 365 days every year. While these Big Tech firms would no doubt love to be able to virtue signal about sourcing their power from wind and solar backed up by enormous banks of batteries, each and every one of them has assessed that option and realized it cannot reliably fill their needs.

Thus, the recent rush to nuclear. After all, once they’ve been built and placed into service, nuclear reactors are a very real zero emissions power source. And unlike wind and solar, nuclear plants do not have to be backed up by an equal amount of generation capacity provided by another fuel, consisting most often of natural gas plants. Nuclear reactors are basically the Energizer Bunnies of power generation: They just keep going and going.

Another big advantage nuclear brings over renewables is the avoidance of the need to invest in massive new transmission networks. This is especially true of SMRs, which can be installed directly adjacent to the contracting data centers. By contrast, wind generation installations must be located in areas where the wind reliably blows. Such areas are often hundreds of miles away from big demand centers, as has been the case in Texas.

Where solar is concerned, the provision of multiple gigawatts (GWs) of generation capacity can require the condemnation of hundreds of acres of land, often thousands. The stationary battery centers for 1 GW of solar or wind would require another large swath of land to be condemned. By contrast, the land footprint for a pair of 500 megawatt (MW) SMRs would amount to no more than a few acres.

Where the deal between Microsoft and Constellation is concerned, sourcing power from an older generation nuclear plant like Three Mile Island will involve interconnecting into an already extant transmission system, though some upgrades and extensions will no doubt be required.

This sudden rush to nuclear by some of the largest companies in the country will benefit all Americans. The massive infusion of capital will accelerate development of SMRs and other advanced nuclear tech, pressure policymakers to modernize antiquated nuclear regulations, and to streamline Byzantine permitting processes that currently inhibit all forms of energy development.

It is a win-win situation for all of us.

David Blackmon is an energy writer and consultant based in Texas. He spent 40 years in the oil and gas business, where he specialized in public policy and communications.

Business

Some Of The Wackiest Things Featured In Rand Paul’s New Report Alleging $1,639,135,969,608 In Gov’t Waste

![]()

From the Daily Caller News Foundation

Republican Kentucky Sen. Rand Paul released the latest edition of his annual “Festivus” report Tuesday detailing over $1 trillion in alleged wasteful spending in the U.S. government throughout 2025.

The newly released report found an estimated $1,639,135,969,608 total in government waste over the past year. Paul, a prominent fiscal hawk who serves as the chairman of the Senate Homeland Security and Governmental Affairs Committee, said in a statement that “no matter how much taxpayer money Washington burns through, politicians can’t help but demand more.”

“Fiscal responsibility may not be the most crowded road, but it’s one I’ve walked year after year — and this holiday season will be no different,” Paul continued. “So, before we get to the Feats of Strength, it’s time for my Airing of (Spending) Grievances.”

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here.

Thank you!

The 2025 “Festivus” report highlighted a spate of instances of wasteful spending from the federal government, including the Department of Health and Human Services (HHS) spent $1.5 million on an “innovative multilevel strategy” to reduce drug use in “Latinx” communities through celebrity influencer campaigns, and also dished out $1.9 million on a “hybrid mobile phone family intervention” aiming to reduce childhood obesity among Latino families living in Los Angeles County.

The report also mentions that HHS spent more than $40 million on influencers to promote getting vaccinated against COVID-19 for racial and ethnic minority groups.

The State Department doled out $244,252 to Stand for Peace in Islamabad to produce a television cartoon series that teaches children in Pakistan how to combat climate change and also spent $1.5 million to promote American films, television shows and video games abroad, according to the report.

The Department of Veterans Affairs (VA) spent more than $1,079,360 teaching teenage ferrets to binge drink alcohol this year, according to Paul’s report.

The report found that the National Science Foundation (NSF) shelled out $497,200 on a “Video Game Challenge” for kids. The NSF and other federal agencies also paid $14,643,280 to make monkeys play a video game in the style of the “Price Is Right,” the report states.

Paul’s 2024 “Festivus” report similarly featured several instances of wasteful federal government spending, such as a Las Vegas pickleball complex and a cabaret show on ice.

The Trump administration has been attempting to uproot wasteful government spending and reduce the federal workforce this year. The administration’s cuts have shrunk the federal workforce to the smallest level in more than a decade, according to recent economic data.

Festivus is a humorous holiday observed annually on Dec. 23, dating back to a popular 1997 episode of the sitcom “Seinfeld.” Observance of the holiday notably includes an “airing of grievances,” per the “Seinfeld” episode of its origin.

From the Fraser Institute

By Nadeem Esmail and Mackenzie Moir

It’s an exciting time in Canadian health-care policy. But even the slew of new reforms in Alberta only go part of the way to using all the policy tools employed by high performing universal health-care systems.

For 2026, for the sake of Canadian patients, let’s hope Alberta stays the path on changes to how hospitals are paid and allowing some private purchases of health care, and that other provinces start to catch up.

While Alberta’s new reforms were welcome news this year, it’s clear Canada’s health-care system continued to struggle. Canadians were reminded by our annual comparison of health care systems that they pay for one of the developed world’s most expensive universal health-care systems, yet have some of the fewest physicians and hospital beds, while waiting in some of the longest queues.

And speaking of queues, wait times across Canada for non-emergency care reached the second-highest level ever measured at 28.6 weeks from general practitioner referral to actual treatment. That’s more than triple the wait of the early 1990s despite decades of government promises and spending commitments. Other work found that at least 23,746 patients died while waiting for care, and nearly 1.3 million Canadians left our overcrowded emergency rooms without being treated.

At least one province has shown a genuine willingness to do something about these problems.

The Smith government in Alberta announced early in the year that it would move towards paying hospitals per-patient treated as opposed to a fixed annual budget, a policy approach that Quebec has been working on for years. Albertans will also soon be able purchase, at least in a limited way, some diagnostic and surgical services for themselves, which is again already possible in Quebec. Alberta has also gone a step further by allowing physicians to work in both public and private settings.

While controversial in Canada, these approaches simply mirror what is being done in all of the developed world’s top-performing universal health-care systems. Australia, the Netherlands, Germany and Switzerland all pay their hospitals per patient treated, and allow patients the opportunity to purchase care privately if they wish. They all also have better and faster universally accessible health care than Canada’s provinces provide, while spending a little more (Switzerland) or less (Australia, Germany, the Netherlands) than we do.

While these reforms are clearly a step in the right direction, there’s more to be done.

Even if we include Alberta’s reforms, these countries still do some very important things differently.

Critically, all of these countries expect patients to pay a small amount for their universally accessible services. The reasoning is straightforward: we all spend our own money more carefully than we spend someone else’s, and patients will make more informed decisions about when and where it’s best to access the health-care system when they have to pay a little out of pocket.

The evidence around this policy is clear—with appropriate safeguards to protect the very ill and exemptions for lower-income and other vulnerable populations, the demand for outpatient healthcare services falls, reducing delays and freeing up resources for others.

Charging patients even small amounts for care would of course violate the Canada Health Act, but it would also emulate the approach of 100 per cent of the developed world’s top-performing health-care systems. In this case, violating outdated federal policy means better universal health care for Canadians.

These top-performing countries also see the private sector and innovative entrepreneurs as partners in delivering universal health care. A relationship that is far different from the limited individual contracts some provinces have with private clinics and surgical centres to provide care in Canada. In these other countries, even full-service hospitals are operated by private providers. Importantly, partnering with innovative private providers, even hospitals, to deliver universal health care does not violate the Canada Health Act.

So, while Alberta has made strides this past year moving towards the well-established higher performance policy approach followed elsewhere, the Smith government remains at least a couple steps short of truly adopting a more Australian or European approach for health care. And other provinces have yet to even get to where Alberta will soon be.

Let’s hope in 2026 that Alberta keeps moving towards a truly world class universal health-care experience for patients, and that the other provinces catch up.

Australian PM booed at Bondi vigil as crowd screams “shame!”

There’s No Bias at CBC News, You Say? Well, OK…

Georgia county admits illegally certifying 315k ballots in 2020 presidential election

FDA warns ‘breast binder’ manufacturers to stop marketing to gender-confused girls

-

International1 day ago

Georgia county admits illegally certifying 315k ballots in 2020 presidential election

-

International1 day ago

International1 day agoCommunist China arrests hundreds of Christians just days before Christmas

-

Business1 day ago

Some Of The Wackiest Things Featured In Rand Paul’s New Report Alleging $1,639,135,969,608 In Gov’t Waste

-

Energy15 hours ago

Energy15 hours agoThe Top News Stories That Shaped Canadian Energy in 2025 and Will Continue to Shape Canadian Energy in 2026

-

Alberta1 day ago

Alberta1 day agoCalgary’s new city council votes to ban foreign flags at government buildings

-

Business2 days ago

Business2 days agoWarning Canada: China’s Economic Miracle Was Built on Mass Displacement

-

International15 hours ago

International15 hours ago$2.6 million raised for man who wrestled shotgun from Bondi Beach terrorist

-

Alberta2 days ago

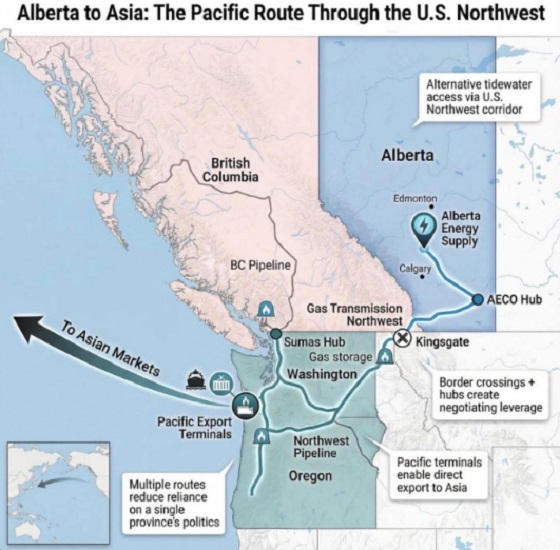

Alberta2 days agoWhat are the odds of a pipeline through the American Pacific Northwest