Energy

A full-throated endorsement of the Secretary of Energy nominee Chris Wright.

In Praise of Chris Wright

Like others, we have watched with curiosity as President-elect Donald Trump has rolled out his nominees for the various leadership positions of his administration. Whatever your views on any particular candidate, an undeniable pattern has emerged. First, Trump is selecting people who strongly support the specific campaign promises on which he ran, and those chosen are vowing to implement them to the letter. Second, lack of prior government experience seems to be an attribute rather than a detriment. Finally, the helminthoid establishment in Washington appears utterly ill-prepared for the deluge that is set to befall them, and Trump can expect significant bipartisan resistance as it dawns on lawmakers just how literal he was being on the campaign trail.

Of particular interest to this publication were the President-elect’s positions on energy. During his many rallies and speeches, candidate Trump vowed to be extremely supportive of domestic energy production, promising to unleash a wave of new investment in oil, natural gas, coal, and nuclear energy. He also committed to ending participation in various international climate change initiatives, much to the horror of those on the progressive environmental left. The shackles of federal regulation would soon be lifted, he said, and the US would come to dominate the global energy scene once again.

Against this backdrop, President-elect Trump electrified those in industry by nominating Chris Wright to the position of Secretary of Energy on Saturday. We can think of no better person for the job.

|

Consider his impressive biography. Wright earned an undergraduate degree in mechanical engineering from the Massachusetts Institute of Technology (MIT) and did graduate work in electrical engineering at both MIT and the University of California, Berkeley. He was a pioneer in the development of US shale gas resources, creating enormous value for shareholders over the past two decades. He has grown his current company, Liberty Energy, into one of the premier energy industry service providers in North America. Finally, he is an investor in and board member of Oklo Inc., a next-generation small modular nuclear reactor (SMR) company that has seen its market cap soar in 2024.

Things get even more promising when one studies Wright’s policy positions on energy. In early 2024, Liberty Energy published a 180-page policy document titled “Bettering Human Lives,” and we are hard-pressed to find anything to disagree with. The ten “Key Takeaways” from the summary page read as follows:

1. Energy is essential to life and the world needs more of it!

2. The modern world today is powered by and made of hydrocarbons.

3. Hydrocarbons are essential to improving the wealth, health, and life opportunities for the less energized seven billion people who aspire to be among the world’s lucky one billion.

4. Hydrocarbons supply more than 80% of global energy and thousands of critical materials and products.

5. The American Shale Revolution transformed energy markets, energy security, and geopolitics.

6. Global demand for oil, natural gas, and coal are all at record levels and rising – no energy transition has begun.

7. Modern alternatives, like solar and wind, provide only a part of electricity demand and do not replace the most critical uses of hydrocarbons. Energy-dense, reliable nuclear could be more impactful.

8. Making energy more expensive or unreliable compromises people, national security, and the environment.

9. Climate change is a global challenge but is far from the world’s greatest threat to human life.

10. Zero Energy Poverty by 2050 is a superior goal compared to Net Zero 2050.

|

What’s not to like? The first nine of these takeaways are objectively true statements of fact, although few executives of publicly traded companies have had the courage to say them out loud. Wright has consistently done so throughout his career. The last is a brilliant reformulation of the climate change debate, as it forces a consideration of the impact on humans, not just the impact of humans.

Wright’s nomination is sure to trigger vigorous opposition by all the predictable people, and we hope he is well prepared to run the gauntlet of personal destruction that the left will undoubtedly use to derail him. Should he win approval in the Senate, Wright has the opportunity to be a historic and transformational figure. His talent, knowledge, leadership attributes, and track record of success make him more than qualified for the job. Count us among those excited at the prospect.

If you’re interested to hear from Wright himself, listen to this episode of Energy News Beat, featuring a discussion with Wright and yours truly, recorded in March of this year.

|

Thank you for reading. Please subscribe to access all articles and support our work.

From Resource Works

Can we please just get on with building one through British Columbia instead?

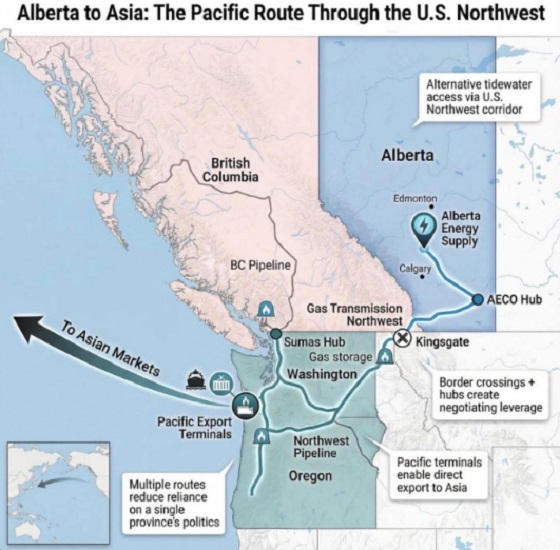

Alberta Premier Danielle Smith is signalling she will look south if Canada cannot move quickly on a new pipeline, saying she is open to shipping oil to the Pacific via the U.S. Pacific Northwest. In a year-end interview, Smith said her “first preference” is still a new West Coast pipeline through northern British Columbia, but she is willing to look across the border if progress stalls.

“Anytime you can get to the West Coast it opens up markets to get to Asia,” she said. Smith also said her focus is building along “existing rights of way,” pointing to the shelved Northern Gateway corridor, and she said she would like a proposal submitted by May 2026.

Deadlines and strings attached

The timing matters because Ottawa and Edmonton have already signed a memorandum of understanding that backs a privately financed bitumen pipeline to a British Columbia port and sends it to the new Major Projects Office. The agreement envisages at least one million barrels a day and sets out a plan for Alberta to file an application by July 1, 2026, while governments aim to finish approvals within two years.

The bargain comes with strings. The MOU links the pipeline to the Pathways carbon capture network, and commits Alberta to strengthen its TIER system so the effective carbon credit price rises to at least 130 dollars a tonne, with details to be settled by April 1, 2026.

Shifting logistics

If Smith is floating an American outlet, it is partly because Pacific Northwest ports are already drawing Canadian exporters. Nutrien’s plan for a $1-billion terminal at Washington State’s Port of Longview highlighted how trade logistics can shift when proponents find receptive permitting lanes.

But the political terrain in Washington and Oregon is unforgiving for fossil fuel projects, even for natural gas. In 2023, federal regulators approved TC Energy’s GTN Xpress expansion over protests from environmental groups and senior officials in West Coast states, with opponents warning about safety and wildfire risk. The project would add about 150 million cubic feet per day of capacity.

A record of resistance

That decision sits inside a longer record of resistance. The anti-development activist website “DeSmog” eagerly estimated that more than 70 percent of proposed coal, oil, and gas projects in the Pacific Northwest since 2012 were defeated, often after sustained local organizing and legal challenges.

Even when a project clears regulators, economics can still kill it. Gas Outlook reported that GTN later said the expansion was “financially not viable” unless it could obtain rolled-in rates to spread costs onto other utilities, a request regulators rejected when they approved construction.

Policy direction is tightening too. Washington’s climate framework targets cutting climate pollution 95 percent by 2050, alongside “clean” transport, buildings, and power measures that push electrification. Recent state actions described by MRSC summaries and NRDC notes reinforce that direction, including moves to help utilities plan a transition away from gas.

Oregon is moving in the same direction. Gov. Tina Kotek issued an executive order directing agencies to move faster on clean energy permitting and grid connections, tied to targets of cutting emissions 50 percent by 2035 and 90 percent by 2050, the Capital Chronicle reported.

For Smith, the U.S. corridor talk may be leverage, but it also underscores a risk, the alternative could be tougher than the Canadian fight she is already waging. The surest way to snuff out speculation is to make it unnecessary by advancing a Canadian project now that the political deal is signed. As Resource Works argued after the MOU, the remaining uncertainty sits with private industry and whether it will finally build, rather than keep testing hypothetical routes.

Resource Works News

![]()

Not for the first time, the Macdonald-Laurier Institute’s Policymaker of the Year is not a Canadian.

In 2019, our laureate was Xi Jinping, leader of the People’s Republic of China, whose long arm reached far into many aspects of policymaking in our nation’s capital.

That helps to underline our intention in conferring this recognition. Policy influence can be used to Canada’s benefit or detriment. In naming our annual Policymaker of the Year, MLI does not endorse their policies; instead, we seek to draw to the attention of Canadians those people who have had the most influence on public policy in this country – for good or ill – in the past year.

And in 2025, who can deny that US President Donald Trump, the Disruptor-in-Chief, has exercised an outsized influence on Canadians – on their hopes and fears, on their political preferences, and, most importantly for our purposes, on the policies pursued by the Canadian government?

How has Donald Trump spurred policy change in Canada? Let us count the ways:

First, set aside for the moment any focus on specific policy areas and just think about the President’s style and strategy. Anyone who has read The Art of the Deal knows that Trump is quite straightforward in avowing that his dealmaking strategy sets out to frighten and intimidate the other party with a degree of unpredictability, bravado, and unwillingness to be bound by past assumptions that is sometimes just breathtaking to contemplate.

On the other hand, what on the surface appears to his opponents as simply irrational is in fact nothing of the sort. He sets out to frighten and intimidate, but he also sets out to get deals done, which cannot happen with negotiating partners paralyzed by fear. And in fact, the list of deals he has done in less than a year in office is impressive: NATO members have made big commitments to increase defence spending, the war in Gaza is paused by a (shaky) ceasefire of his design, trade deals have been struck with many partners, including the EU, the UK, Mexico, and even China … though notably, not with Canada.

Here at home, Trump has riled Canadians with his comments about annexation and disputed borders, laid a heavy finger on the 2025 electoral scales, and met repeatedly with Prime Minister Mark Carney – but equally repeatedly sent him on his way with little to show for the Prime Minister’s efforts as supplicant. Policies that seemed settled, like our purchase of the F-35 fighter jet, our deep integration with the US economy, and our feeble attempts at even-handedness in the conflict in the Middle East, all seem to have fallen victim to Ottawa’s ill-advised urge to stick a finger in Donald Trump’s eye, whatever the cost.

Like it or not, Trump has reminded Canadians in no uncertain terms that America is the elephant and we are, if not exactly a mouse, certainly a beast whose wellbeing depends on American forbearance and good will. The question of whether we can calm the rampaging elephant and charm him into a better humour or fall back on much less profitable relations with other countries far away is THE question that will preoccupy policymakers in Ottawa this year and for several years to come.

It is against this backdrop that several major dimensions of Canada-US relations have been thrust into the spotlight – none more dramatically than trade.

Weaponized Tariffs and Fractured Trade

Tim Sargent

For many Canadians, Donald Trump’s re-election on November 5, 2024, while not a cause for celebration, was also not an existential threat to our economy. After all, when Trump was first elected in 2016, his threats to tear up the North American Free Trade Agreement (NAFTA) ultimately came to nothing, and the new version of NAFTA that was negotiated by the US, Canada, and Mexico (we call it CUSMA, the Americans call it USMCA), was broadly similar to its predecessor, with almost all Canadian goods able to enter the US market tariff-free.

That complacency was almost immediately shattered when the President, even before his inauguration, announced his intent to slap a tariff of 25 per cent on Canadian (and Mexican exports), supposedly in response to Canada’s failure to stop fentanyl from crossing over the US border. The shock was rapid, and the implications unmistakable.

Once in office, Trump made good on his threat and imposed the 25 per cent tariff on all Canadian exports except energy, which was subject to “only” a 10 per cent tariff. The sheer interconnectedness of the North American economy forced Trump to partially back down and exempt CUSMA-compliant goods from the tariffs. However, because they raised input costs for US manufacturers, Trump opened another front by slapping tariffs on steel, aluminum, autos, copper, lumber, and furniture in the name of national security, overriding the CUSMA treaty that he had signed. While these tariffs apply to all countries, these are all commodities for which Canadian exporters are very dependent on the US market, and which are very important for the Canadian economy.

While trade disputes with the US have not been unknown since the signing of the original Canada-US Free Trade Agreement in 1988 – softwood lumber is the most obvious example – no one expected Trump to take aim at the whole Canada–US trading relationship, which accounts for almost a quarter of our GDP. This escalation marks a break not just with economic norms but with decades of strategic restraint.

None of this augers well for the negotiations for the renewal of CUSMA, which are supposed to conclude in the summer of 2026, or the broader Canada-US trading relationship. Indeed, it is not clear that the renewal document will be worth the paper it is written on, given that Trump has shown no compunction in violating the terms of the original agreement. Perhaps even more fundamentally, the President, reflecting a broader strand of America-first nationalism, simply does not see trade as a mutually beneficial activity; rather, it is a zero-sum game in which the only way for the US to win is for others to lose. The fact that basic economics says the opposite seems to be neither here nor there.

All this leaves Canadian policymakers with some unpleasant alternatives. While the Carney government originally attempted to retaliate by imposing tariffs of its own, the reality is that these are pinpricks to the US, for which Canadian exports are only a few percentage points of GDP. Furthermore, tariffs hurt Canadian consumers. The other alternative, which the government is now pursuing, is to diversify Canada’s trade away from the US. However, Canadian governments have been trying to reduce their reliance on the United States since at least the 1970s, with little success. Geography and economic gravity continue to dominate: the US will always be the most obvious market for our exports, even with tariffs.

Perhaps the most that Canadians can hope for is that Americans will, as has happened in the past, come to realize that a close and stable trading relationship with Canada is in their national interest just as much as it is in ours.

Trade Tensions Fuel Canadian Oil Revival

Heather Exner-Pirot

Donald Trump’s tariffs and threat to the Canadian economy have meaningfully shifted both the public understanding and attitude towards oil and gas. Perhaps in the past it could be seen simply as something Alberta produced, an embarrassing source of global emissions. After 2025, it became clear how essential oil production is both to our economic health and our global standing.

Oil is Canada’s largest export, and most of it goes to the United States. When Trump declared in January 2025 that “we don’t need their oil and gas. We have more than anybody,” it was a tell. Canadian oil and gas is precisely the thing we produce that the United States needs more than anything else. In fact, that same month the US imported a record amount of Canadian crude oil: 4.27 million barrels; the most any country has ever imported from another in the history of the world.

This newfound appreciation of oil and its geopolitical importance brought a long-dead idea back to life: an oil pipeline to the northwest coast of British Columbia, the value of which has always been in diversifying our market for heavy oil from the US to Asia. The source of hard fought culture wars in the 2010s before being approved in 2014, rejected by Trudeau in 2018, and handed the final indignity of a tanker ban in 2019, a Northern Gateway-type pipeline is now not only possible, but even likely. In every public opinion poll in 2025, such a pipeline has enjoyed majority support. It is the centrepiece of the landmark MOU between the federal and Alberta government that has as an explicit goal increasing oil and gas production.

Canada has always had the resources of an energy superpower. Trump’s threats have done more to give us the ambition of one than anyone or anything before him.

“Elbows up” and the New Anti-American Nationalism

Mark Reid

Donald Trump’s return to the White House drastically altered the course of Canadian politics. The ensuing fallout – fuelled by threats of tariffs and incendiary “51st state” rhetoric – became the key catalyst that propelled Mark Carney’s Liberals to victory on an “elbows up” platform.

This resurgent Canadian nationalism was defined by a sharp strain of anti-Americanism in general, and a profound dislike of Trump in particular.

As Trump slapped tariffs on Canada (and mused about annexing Greenland), the Prime Minister and provincial leaders promised a “Team Canada” approach to counter the President’s aggression. Canadian politicians from coast to coast earnestly vowed to remove interprovincial trade barriers, back major national projects, and present a common front.

That unity quickly faded.

Faced with new rounds of tariff threats, Carney’s government shifted to diplomatic conciliation, rolling back the Digital Sales Tax and offering border security concessions to avert economic disaster. Supporters called it pragmatism; critics called it a surrender.

Meanwhile, the Team Canada vision turned out to be a mirage. Interprovincial squabbles over a bitumen pipeline to tidewater in BC persists, while a multi-million-dollar Ontario anti-tariff ad, which aired on US television, infuriated Trump.

These internal divisions underscore a dangerous reality: Canada’s very sovereignty may be at risk. The US President’s recent “Trump Corollary” to the Monroe Doctrine clearly articulates his vision of American hegemony over the Americas, with Canada, presumably, as a sort of vassal state. The federal government now faces an impossible task – buying time in the hope that the US political climate shifts, while protecting Canadian autonomy from an American president who sees it as negotiable.

Smashing the Overton Window on social policy

Peter Copeland

Donald Trump is polarizing for good reason. He is rude, crude, lewd, and norm-breaking to an extraordinary degree: a former Manhattan Democrat and social liberal whose transgressiveness and contempt for precedent embody many of the very cultural tendencies the left has long celebrated. His impulsiveness seems to threaten alliances and raise geopolitical risks by the day – yet he now leads the most effective conservative movement in decades.

He also possesses unusual strengths. His entrepreneurial instinct has allowed him to see the gap created by an oblivious, or unwilling, left- and right- establishment political class on trade, immigration, cultural and social decline – and to seize the opportunity. His unfiltered political style contrasts sharply with the scripted, risk-averse habits of career politicians and the professional-managerial class. He seeks no validation from the Davos set or the media-academic establishment, making him unafraid to challenge orthodoxy. Trump’s rise is a sharp indictment of liberal elites on both sides of the political spectrum, who proved incapable of addressing the deep social and economic issues that he foregrounded from the outset of his presidency.

On issues like gender identity, DEI, and mass migration, rooted in an extreme open-society ideology of hyper-individualism and autonomy, establishment leaders had long been unwilling even to acknowledge the problems. Then Trump came along and threw open the Overton window on just about every issue.

For Canada, Trump’s impact is mixed. He expanded the envelope of the politically possible on topics thought untouchable just years ago, but his abrasive style has made Canadian elites – whose defining characteristic is anti-Americanism – more reluctant to pursue parallel reforms. On immigration, borders and defence, Ottawa is now moving; on gender, DEI, and education, it is retreating behind “Trump did it, so we won’t.”

Shredding Canada’s US security blanket

Richard Shimooka

President Trump’s successful upending of American foreign policy in 2025 has had profound and potentially long-term consequences, but few are as acutely felt as the changes he has forced upon the Canada-US security relationship. Trump’s actions have effectively ended the decades-long expectation that the United States would forever underwrite Canada’s defence and security, forcing a sea-change in Ottawa’s strategic calculus.

Since the Second World War, the foundation of the Canada-US security and economic relationship has been an interlocking system of security guarantees through alliances and free trade blocs. This synergistic mix, which bound states like Canada to a rules and values based international order conceived in Washington, allowed Canada to maintain a relatively small defence footprint, relying instead on overwhelming American firepower to deter its enemies.

However, Trump’s skepticism towards this foundation, evident since his first term, consolidated into decisive policy changes in his second term. By launching a devastatingly counterproductive trade war against Canada and other major trading partners and directly questioning the value of major alliances like NATO, he effectively declared America’s security commitments are no longer unconditional.

For Canada, this has meant a new urgency to foot a larger portion of the bill for continental security, a renewed focus on securing both the Canada-US border and the Arctic, and for finally meeting long-standing pledges to spend two per cent of GDP on NATO.

Ironically, while Trump’s pressure tactics have succeeding in pushing Canada (and other allies like Japan and Germany) to increase defence spending and become more self-sufficient, it comes at the cost of America’s ability to lead like-minded states. As US leverage wanes, Trump’s strategy may end up pushing America’s allies into the arms of strategic rivals like China.

Without American global leadership, states may prioritize a narrower brand of self-interest – one that is counterproductive to America’s overall strategic ends. Observe how Canada is now looking to rebuild its economic relationship with the People’s Republic of China, not merely for trade, but as a deliberate economic counterweight to its highly integrated trade relationship with the United States.

This impulse will likely be shared by many US allies. Indeed, allied nations in Southeast Asia may begin to doubt Washington’s commitment to the current geopolitical alignment and seek to balance their relationship with China. Some may even fall further into Beijing’s grasp, becoming the 21st-century equivalent of tributary states.

“Trump the Peacemaker” and the Politics of Force

Casey Babb

Donald Trump’s bold and fearless foreign policy decisions – especially regarding Israel’s war in Gaza and the broader Middle East – make him one of the most consequential and transformative political leaders in a generation. His combination of disruption, recalibration, and strategic risk-taking sought to redirect the trajectory of the Middle East in ways few leaders have attempted.

Some of these changes began during Trump’s first administration. The Abraham Accords, which normalized relations between Israel and several Arab states, reflected a shift toward open regional co-operation against shared security concerns. His decisions, like recognizing Jerusalem as Israel’s capital and cutting aid to Palestinian institutions, were commonsense corrections to what he viewed as unnecessary diplomatic ambiguities.

However, his most transformative actions in the Middle East happened in the aftermath of the October 7, 2023, Hamas terror attacks on Israel. From his 20-point plan for peace in Gaza and his efforts to bring home hostages, to the “12 Day War” between Israel and Iran, Trump made it clear that America’s support for Israel remains unwavering – signalling that Washington is willing to take decisive action in the Middle East to protect US and allied security.

Beyond the Middle East, Trump’s approach to China marked a sharp departure from previous presidents. Replacing engagement tactics with tariffs, export controls, and the framing of China as a key rival, Trump pushed for a shift in US policy that continues in his second term in office.

In Europe, Trump’s record on the Russia-Ukraine war is mixed. The President has pressured NATO allies to carry a greater load in terms of supporting Ukraine, and the US has continued to provide Kyiv with lethal military aid. However, critics worry about Trump’s personal relationship with Russian President Vladimir Putin: as the peace negotiations continue, will Ukraine eventually be sacrificed for American expediency?

Conclusion

Trump’s legacy remains unwritten. It may destabilize Western institutions, or it may be the jolt needed to shake a complacent boomer establishment out of its decadent, dogmatic slumbers.

Trump has clearly shifted the geopolitical landscape in both Canada and around the world – in ways no conventional figure could have. It is worth asking: would Europe have increased defence spending without American pressure? Would Canada have taken border security, immigration, defence, or energy policy seriously?

Even conservative governments – often differing little from liberal ones in practice – have lacked the capital or resolve to confront entrenched bureaucracies, and it remains doubtful whether any old-school Canadian libertarian-oriented fusionist, or a typical Wall Street Republican in the US, would have had what it took to win, yet alone enact the needed the reforms.

Trump was, and is, very much the man for the moment. Whether this shift leads to renewal or decline, only time will tell. Those same disruptive instincts have defined his approach to the world stage as well, reshaping geopolitics in ways Canadians cannot ignore.

Brian Lee Crowley is managing director of the Macdonald-Laurier Institute.

Tim Sargent is a senior fellow and the director of Domestic Policy at MLI.

Heather Exner-Pirot is a senior fellow and MLI’s director of Energy, Natural Resources, and the Environment.

Mark Reid is the senior editor at MLI.

Peter Copeland is the deputy director of Domestic Policy at MLI.

Richard Shimooka is a senior fellow at MLI.

Casey Babb is the director of MLI’s The Promised Land program.

Argentina’s Milei delivers results free-market critics said wouldn’t work

Australian PM booed at Bondi vigil as crowd screams “shame!”

‘Almost Sounds Made Up’: Jeffrey Epstein Was Bill Clinton Plus-One At Moroccan King’s Wedding, Per Report

There’s No Bias at CBC News, You Say? Well, OK…

-

International2 days ago

Australian PM booed at Bondi vigil as crowd screams “shame!”

-

Uncategorized2 days ago

Uncategorized2 days agoMortgaging Canada’s energy future — the hidden costs of the Carney-Smith pipeline deal

-

Automotive1 day ago

Automotive1 day agoCanada’s EV gamble is starting to backfire

-

Alberta1 day ago

Alberta1 day agoAlberta Next Panel calls to reform how Canada works

-

Digital ID15 hours ago

Digital ID15 hours agoCanadian government launches trial version of digital ID for certain licenses, permits

-

Agriculture1 day ago

Agriculture1 day agoEnd Supply Management—For the Sake of Canadian Consumers

-

Business14 hours ago

The “Disruptor-in-Chief” places Canada in the crosshairs

-

International15 hours ago

International15 hours agoWorld-leading biochemist debunks evolutionary theory