Business

Proposed federal tax hike would make Canada’s top capital gains tax rate among the highest of 37 advanced countries

From the Fraser Institute

By Jake Fuss and Grady Munro

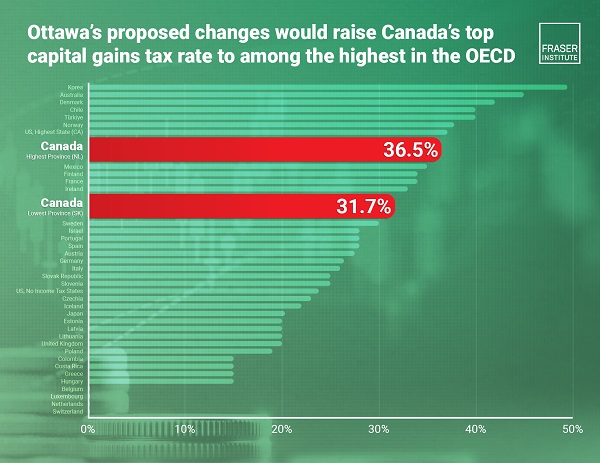

Ottawa’s proposed increase to the effective capital gains tax rate will result in Canada having among the highest—and least competitive—top capital gains tax rates in the industrialized world, finds a new study released today by the Fraser Institute, an independent, non-partisan, Canadian public policy think-tank.

“The evidence is clear—taxing capital gains deters investment, particularly smaller and start-up firms, which in turn slows productivity gains and innovation, all things Canada needs right now to raise living standards for workers,” said Jake Fuss, director of fiscal studies at the Fraser Institute and co-author of Canada’s Waning Competitiveness on Capital Gains Taxes.

The study finds that by increasing the inclusion rate, the federal government has made Canada less competitive compared to other advanced countries. At a 50 per cent inclusion rate, Canada’s top capital gains tax rate ranked between 17th and 23rd (depending on the province) out of 37 high-income developed countries in the Organization for Economic Co-operation and Development (OECD).

Raising the inclusion rate to 66.7 per cent means Canada’s top capital gains tax rate would be among the highest and least competitive (between 8th and 13th highest, depending on the province).

The study notes that if Canada’s capital gains inclusion rate were lowered to 33.3 per cent, Canada would be among the most competitive in the OECD, ranking 30th and 31st, again, depending on the province.

“Instead of raising taxes on capital gains, policymakers should consider reducing taxes as a way of attracting much-needed investment, and reversing Canada’s current economic slump,” Fuss said.

Jake Fuss

Director, Fiscal Studies, Fraser Institute

Grady Munro

From the Frontier Centre for Public Policy

By Jay Goldberg

Rosy projections, chronic deficits, and opaque budgeting. If nothing changes, Carney’s credibility could collapse under the same weight.

Carney promised a fresh start. His budget makes it look like we’re still stuck with the same old Trudeau playbook

It turns out the Trudeau government really did look at Canada’s economy through rose-coloured glasses. Is the Carney government falling into the same pattern?

New research from the Frontier Centre for Public Policy shows that federal budgets during the Trudeau years “consistently overestimated [Canada’s] fiscal health” when it came to forecasting the state of the nation’s economy and finances over the long term.

In his research, policy analyst Conrad Eder finds that, when looking specifically at projections of where the economy would be four years out, Trudeau-era budgets tended to have forecast errors of four per cent of nominal GDP, or an average of $94.4 billion.

Because budgets were so much more optimistic about long-term growth, they consistently projected that government revenue would grow at a much faster pace. The Trudeau government then made spending commitments, assuming the money would be there. And when the forecasts did not keep up, deficits simply grew.

As Eder writes, “these dramatic discrepancies illustrate how the Trudeau government’s longer-term projections consistently underestimated the persistence of fiscal challenges and overestimated its ability to improve the budgetary balance.”

Eder concludes that politics came into play and influenced how the Trudeau government framed its forecasts. Rather than focusing on the long-term health of Canada’s finances, the Trudeau government was focused on politics. But presenting overly optimistic forecasts has long-term consequences.

“When official projections consistently deviate from actual outcomes, they obscure the scope of deficits, inhibit effective fiscal planning, and mislead policymakers and the public,” Eder writes.

“This disconnect between projected and actual fiscal outcomes undermines the reliability of long-term planning tools and erodes public confidence in the government’s fiscal management.”

The public’s confidence in the Trudeau government’s fiscal management was so low, in fact, that by the end of 2024 the Liberals were polling in the high teens, behind the NDP.

The key to the Liberal Party’s electoral survival became twofold: the “elbows up” rhetoric in response to the Trump administration’s tariffs, and the choice of a new leader who seemed to have significant credibility and was disconnected from the fiscal blunders of the Trudeau years.

Mark Carney was recruited to run for the Liberal leadership as the antidote to Trudeau. His résumé as governor of the Bank of Canada during the Great Recession and his subsequent years leading the Bank of England seemed to offer Canadians the opposite of the fiscal inexperience of the Trudeau years.

These two factors together helped turn around the Liberals’ fortunes and secured the party a fourth straight mandate in April’s elections.

But now Carney has presented a budget of his own, and it too spills a lot of red ink.

This year’s deficit is projected to be a stunning $78.3 billion, and the federal deficit is expected to stay over $50 billion for at least the next four years.

The fiscal picture presented by Finance Minister François-Philippe Champagne was a bleak one.

What remains to be seen is whether the chronic politicking over long-term forecasts that plagued the Trudeau government will continue to be a feature of the Carney regime.

As bad as the deficit figures look now, one has to wonder, given Eder’s research, whether the state of Canada’s finances is even worse than Champagne’s budget lets on.

As Eder says, years of rose-coloured budgeting undermined public trust and misled both policymakers and voters. The question now is whether this approach to the federal budget continues under Carney at the helm.

Budget 2025 significantly revises the economic growth projections found in the 2024 fall economic statement for both 2025 and 2026. However, the forecasts for 2027, 2028 and 2029 were left largely unchanged.

If Eder is right, and the Liberals are overly optimistic when it comes to four-year forecasts, then the 2025 budget should worry Canadians. Why? Because the Carney government did not change the Trudeau government’s 2029 economic projections by even a fraction of a per cent.

In other words, despite the gloomy fiscal numbers found in Budget 2025, the Carney government may still be wearing the same rose-coloured budgeting glasses as the Trudeau government did, at least when it comes to long-range fiscal planning.

If the Carney government wants to have more credibility than the Trudeau government over the long term, it needs to be more transparent about how long-term economic projections are made and be clear about whether the Finance Department’s approach to forecasting has changed with the government. Otherwise, Carney’s fiscal credibility, despite his résumé, may meet the same fate as Trudeau’s.

Jay Goldberg is a fellow with the Frontier Centre for Public Policy.

From the Fraser Institute

By Alex Whalen and Jake Fuss

This holiday season, many Canadians will fly to spend time to with family and friends. But air travellers in Canada consistently report frustration with service, cost and choice. In its recent budget, the Carney government announced it will consider “options for the privatization of airports.” What does this mean for Canadians?

Up until the 1990s, the federal government served as both the owner and operator of Canada’s major airports. The Chrétien government partially privatized and transferred the operation of major airports to not-for-profit airport authorities, while the federal government remained the owner of the land. Since then, the federal government has effectively been the landlord for Canada’s airports, collecting rent each year from the not-for-profit operating authorities.

What would full privatization of airports look like?

If the government allows private for-profit businesses to own Canada’s major airports, their incentives would be to operate as efficiently as possible, serve customers and generate profits. Currently, there’s little incentive to compete as the operating authorities are largely unaccountable because they only report to government officials in a limited form, rather than reporting directly to shareholders as they would under privatization. Private for-profit airports exist in many other countries, and research has shown they are often less costly for passengers and more innovative.

Yet, privatization of airports should be only the first step in a broader package of reforms to improve air travel in Canada. The federal government should also open up competition by creating the conditions for new airports, new airlines and new investment. Currently, Canada restricts foreign ownership of Canadian airlines, while also restricting foreign airlines from flying within Canada. Consequently, Canadians are left with little choice when booking air travel. Opening up the industry by reversing these policies would force incumbent airlines to compete with a greater number of airlines, generating greater choice and likely lower costs for consumers.

Moreover, the federal government should reduce the taxes and fees on air travel that contribute to the cost of airline tickets. Indeed, according to our recent research, among peer countries, Canada has among the most expensive air travel taxes and fees. These costs get passed on to consumers, so it’s no surprise that Canada consistently ranks as a very expensive country for air travel.

If the Carney government actually privatizes Canada’s airports, this would be a good first step to introducing greater competition in an industry where it’s badly needed. But to truly deliver for Canadians, the government must go much further and overhaul the numerous policies, taxes and fees that limit competition and drive up costs.

Alex Whalen

Director, Atlantic Canada Prosperity, Fraser Institute

Jake Fuss

Director, Fiscal Studies, Fraser Institute

Landmark 2025 Study Says Near-Death Experiences Can’t Be Explained Away

STUDY: TikTok, Instagram, and YouTube Shorts Induce Measurable “Brain Rot”

Blacked-Out Democracy: The Stellantis Deal Ottawa Won’t Show Its Own MPs

Red Deer’s Jason Stephan calls for citizen-led referendum on late-term abortion ban in Alberta

-

Business1 day ago

Business1 day agoRecent price declines don’t solve Toronto’s housing affordability crisis

-

Daily Caller1 day ago

Daily Caller1 day agoTech Mogul Gives $6 Billion To 25 Million Kids To Boost Trump Investment Accounts

-

National1 day ago

National1 day agoCanada Needs an Alternative to Carney’s One Man Show

-

Alberta1 day ago

Alberta1 day agoAlberta will defend law-abiding gun owners who defend themselves

-

Artificial Intelligence2 days ago

Artificial Intelligence2 days agoThe Emptiness Inside: Why Large Language Models Can’t Think – and Never Will

-

Business1 day ago

Business1 day agoOttawa’s gun ‘buyback’ program will cost billions—and for no good reason

-

Business1 day ago

Business1 day agoCanada’s future prosperity runs through the northwest coast

-

Alberta18 hours ago

Alberta18 hours agoThis new Canada–Alberta pipeline agreement will cost you more than you think