Also Interesting

6 Netflix Original Movies filmed in Canada

Canada is widely recognized as one of the most beautiful countries in the world. With so many natural beauty backdrops, American film makers are shooting some of the most popular Netflix movies here. In fact it just might be that some of your favourite movies are filmed in Canada.

In this article, we will discuss original Netflix movies that are filmed in Canada. Also, we will tell you how you can access these US Netflix films wherever you are.

The Incredible Hulk

Directed by Louis Leterrier, The Incredible Hulk is an early and thoroughly enjoyable Marvel movie which features the amazing actor, Edward Norton as the titular force of nature, and Bruce Banner’s alter ego. Don’t let the mediocre reviews fool you, The Incredible Hulk is a much watch movie. The acting is spot on and this is something all members of the family would enjoy to watch.

October Faction

Based on reviews; October Faction, a series about people hunting monsters, lacks in almost all aspects from storytelling to plot. However, we see that this show has managed to garner a following who are still waiting for its season 2. The Story of October Faction has many rooms for improvement, from developing story lines for the main characters to adding some more action. If only more monster hunting was added to the film, it would be a great turning point for this film.

Chilling Adventures of Sabrina (Part 3)

Chilling Adventures of Sabrina Season 3 is directed by Rob Seidenglanz, Alex Pillai, Kevin Rodney Sullivan, Craig William Macneill, Viet Nguyen, Jeff Woolnough and was one of the most anticipated Netflix Series of 2020. The minds behind this film set out to ensure there are no boring moments. What makes the show interesting is both Sabrina’s power and her resistance to evil which comes from her goodness and her love for her friends and aunties. Despite being a witch, she remained a good and morally upright person. This might be the reason why everyone is excited for season 4.

Inception

Directed and written by Christopher Nolan, Inception has received numerous incredible reviews. Inception was filmed in Calgary where Leo De Carpio spent some time while filming this Netflix Film. Inception is known to be one of the best films of the century, receiving a rating of 87%. Nominated for eight Oscars, including Best Picture and Best Original Screenplay this film is superbly created and packed with action. Inception is unique in its complex portrayal of a hypnotizing vista of dreams within other dreams.

To All the Boys: P.S. I Still Love You

This Netflix original film directed by Michael Fimognari has received good reviews and ratings so far. It is the most highly anticipated Netflix film of this year for romance. This movie was filmed in Vancouver Aquarium, Queen Elizabeth Park and in surrounding areas..

Fractured

Directed by Brad Anderson, Fractured has received several good reviews from both critics and viewers. This thriller is very well created and executed, supported by amazing acting performances. The story revolves around the aftermath of a terrible accident. When Ray Monroe rushes his daughter and wife to a busy hospital, they seemingly dissappear. Tension builds throughout as Ray searches frantically in an effort to save his family.

Conclusion

The success of Netflix films isn’t only about great stories and plots, locations are carefully chosen because they are also critical. Of course choosing the right film depends on your taste and the genre you like to watch. But, we hope that we have given you a little bit of a push to try to spend some time with these Netflix original films.

Quick Steps to access US Netflix in Canada

We understand that if you are outside the US, you might not have access to US Netflix content. However, you can easily access the US Netflix by using any of the premium VPNs available. To access US Netflix in Canada, simply follow these steps:

1. Choose and look for any VPN provider on the internet that suits your needs. There are a lot of available VPN tools you can use to bypass geo-blocks. Just make sure to choose the one that offers fastest video streaming to avoid inconveniences.

2. Once you have secured a premium VPN account, log in and choose any US server from the location list.

3. Lastly, watch the best movies on Netflix Canada or the US. 6 Netflix Films That Are Filmed in Canada

If you’re looking for a provider that blends striking visuals, solid math models, and engaging themes, Endorphina slots are a must-try. Now featured at Zoome casino, Endorphina is quickly becoming a favourite among Canadian players who enjoy well-balanced volatility and great return potential.

From classic fruit machines to themed adventures with expanding wilds, Endorphina in casino environments offers reliable entertainment and serious payout opportunities. But what makes these games stand out? Let’s break down the key features, winning potential, and why you should play Endorphina games at Zoome.

Who Is Endorphina?

Endorphina is a leading game provider based in Prague, with over a decade of experience in developing online slots for regulated markets. The company is known for its well-polished video slots that balance engaging storylines with player-friendly mechanics. Their catalogue includes over 100 titles, with new releases launched regularly.

In Canada, Endorphina slots are now widely accessible through Zoome casino, one of the country’s fastest-growing platforms with a large game library and crypto-friendly payments.

Popular Endorphina Slots You Can Try at Zoome

Once you complete your zoome casino login, head over to the Endorphina slots section to discover a curated list of titles. Here are some fan favourites:

1. Hell Hot 100

● RTP (Return to Player): 96.07%

● Volatility: Medium

● Max Win: 1,000x

● Type: Classic fruit slot with a hot twist

● Why Play: Simple gameplay, blazing fast spins, and high hit frequency

2. Chance Machine 100

● RTP: 96.00%

● Volatility: Low to Medium

● Max Win: 5,000x

● Features: Expanding wilds, stacked symbols

● Why Play: Perfect for casual players who want frequent wins

3. Book of Santa

● RTP: 96.00%

● Volatility: High

● Max Win: 5,500x

● Features: Free spins with expanding symbols

● Why Play: A seasonal slot that pays like a timeless classic

4. Tribe

● RTP: 96.00%

● Volatility: Medium to High

● Max Win: 3,000x

● Special Feature: Free spins with progressive multipliers

● Why Play: Visually beautiful with strong payout structure

All endorphina games are built with HTML5, ensuring smooth play on desktop and mobile without requiring downloads.

Are There Endorphina Free Slots?

Yes! Endorphina free slots are available for demo play directly on Zoome. This means Canadian players can try out their favourites before making a real-money commitment. Free versions include all the same features, visuals, and mechanics — great for getting familiar with a game’s volatility and bonus structure.

To access, simply log in or click the “Demo” button on any title from the Endorphina section on Zoome.

Zoome Casino Bonuses and Endorphina Integration

Zoome casino offers several bonuses that can be used specifically on Endorphina slots, including:

● Welcome bonuses with free spins on selected Endorphina titles

● Reload bonuses for returning players

● Cashbacks and weekend tournaments featuring endorphina slot themes

● Seasonal campaigns with exclusive zoome casino promo codes

New players should check for a potential zoome no deposit bonus, as it occasionally applies to Endorphina’s most popular games like Book of Santa or Hell Hot 100.

RTP, Win Rate & Performance Metrics

Endorphina designs its games with a balance of fairness and entertainment. Here’s a general breakdown:

Metric Range/Typical Value

RTP 96.00% – 96.07%

Average Hit Frequency ~1 in 4 spins

Max Exposure (Base Game) 1,000x to 5,500x

Bonus Trigger Frequency 1 in 120–150 spins (approx.)

Average Session Duration 15–25 mins (based on volatility)

These stats make Endorphina in casino environments appealing to both casual players and slot grinders who understand variance and bankroll management.

Play Anywhere, Anytime

Zoome supports mobile-first gameplay. Every endorphina slot loads seamlessly on iOS and Android without needing an app. With fast servers, secure encryption, and a clean layout, spinning is quick, intuitive, and glitch-free.

Whether you’re chasing a bonus round or enjoying a few free spins on your lunch break, Zoome makes the experience smooth and hassle-free.

Final Thoughts

With its mix of quality graphics, strong RTP, and easy bonus access, Endorphina slots are a solid choice for Canadian players. Whether you’re trying endorphina free slots in demo mode or diving into real-money play via zoome casino login, there’s a title to suit your style.

From well-known hits like Hell Hot 100 to sleeper favourites like Tribe, this provider continues to prove why Endorphina in casino settings is a winning combination. And with regular zoome casino promo code campaigns and potential zoome no deposit bonus access, it’s the perfect time to start spinning.

Ready to explore the full lineup? Visit Zoome and see what Endorphina has to offer — your next big win could be one spin away.

Financial freedom means different things to different people. Some seek to clear debt or reduce working hours. Others aim to build an income stream separate from traditional employment. Betting is often seen as entertainment, but some treat it as a potential method for financial gain.

It is not a simple route. Success in betting depends on skill, patience, and clear risk control. Casual bets and chasing losses are not the same as long-term planning. Play slots and live casino online deals may attract interest, but true gains require a well-developed approach grounded in calculation,

not luck.

Some treat betting as a serious income project. Like investing, it involves monitoring markets, sticking to rules, and managing emotion. These habits shape outcomes more than any single win or loss.

The Role of Strategy and Market Choice

Building consistent returns from betting starts with discipline. Most success stories come from people who specialize in specific markets. They avoid randomness and focus on repeatable patterns. This reduces risk and allows room for structured decisions.

For some, sports betting offers the best value. Others prefer slots, roulette, or blackjack. Success in each area depends on the ability to control the betting environment. Choosing fixed budgets, setting limits, and logging results all contribute to a more sustainable system.

In Ireland and the UK, platforms now offer a wider range of services. These include analytics tools, stat-based bets, and account dashboards. Markets like Slots and table games in Ireland are especially popular among users who combine short sessions with targeted goals.

Key traits of long-term betting approaches include:

● Specialising in specific games or sports.

● Avoiding emotional or rushed bets.

● Logging every session and reviewing performance.

● Staking only a fixed portion of the bankroll per event.

Psychological Factors and Risk Limits

Financial growth through betting requires mental control. Most losses in gambling happen when people act without a plan. Emotional decisions, such as doubling stakes after a loss, often lead to poor outcomes.

Structured bettors approach the activity with neutral judgement. They view each bet as part of a larger system, not an isolated moment. This approach reduces stress and protects capital. Understanding the limits of control also helps. For example, not every market behaves the same

way each week.

Many betting platforms now offer tools that assist with self-monitoring. These include loss caps, spending summaries, and trend reports. These systems support the user but cannot replace careful thinking. Understanding the connection between strategy risk and decision making can lead to

better choices, both short and long-term.

Economic Context and the Role of Discipline

The idea of using betting as a route to financial freedom often attracts attention during economic stress. Some people look for faster income options when prices rise or wages stagnate. However, betting is not a guaranteed path. It only works when treated as a skill-based discipline, not a

shortcut.

Those who see results often treat betting like a second job. They put in regular hours for research, review performance metrics, and stick to a strict process. This removes guesswork and replaces it with control.

Having multiple sources of income is one part of building financial freedom. Betting can be one of those if it is paired with discipline, patience, and analysis. It is not passive income. It requires consistent effort and awareness.

Sensible Goals and Sustainable Progress

Success with betting should not be measured in jackpots or sudden windfalls. Small, repeatable profits are more stable. The aim is to grow a bankroll slowly, avoid major losses, and learn from every result. This mindset supports steady progress and avoids burnout.

Financial freedom through betting is possible for some. However, it depends on the user, not the platform. Planning, structure, and clear risk boundaries matter more than the type of bet. For those who view betting as a long-term activity rather than a quick fix, it can play a role in building

independence.

As always, betting should be treated with care and clear intent. When combined with focus and habit, it can support a wider plan toward financial freedom. However, without those foundations, it is more likely to create setbacks than solutions.

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

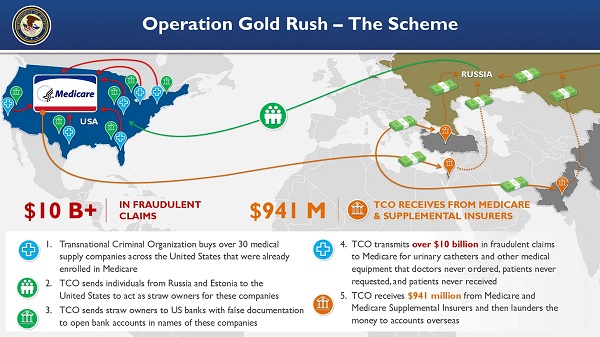

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Crime2 days ago

Crime2 days ago“This is a total fucking disaster”

-

Fraser Institute1 day ago

Fraser Institute1 day agoBefore Trudeau average annual immigration was 617,800. Under Trudeau number skyrocketted to 1.4 million annually

-

Daily Caller2 days ago

Daily Caller2 days ago‘I Know How These People Operate’: Fmr CIA Officer Calls BS On FBI’s New Epstein Intel

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is already killing the disabled. It’s about to get worse

-

Daily Caller2 days ago

Daily Caller2 days agoBlackouts Coming If America Continues With Biden-Era Green Frenzy, Trump Admin Warns

-

Red Deer2 days ago

Red Deer2 days agoJoin SPARC in spreading kindness by July 14th

-

Business1 day ago

Business1 day agoPrime minister can make good on campaign promise by reforming Canada Health Act

-

Frontier Centre for Public Policy1 day ago

Frontier Centre for Public Policy1 day agoNew Book Warns The Decline In Marriage Comes At A High Cost